Reinventing airport economics

The influence of airports reaches far beyond aviation. They are vital engines of employment, economic growth, regional development, and global connectivity.

The aviation sector contributes 3.9% of global GDP, and airports themselves significantly contribute to local and national economies. Worldwide, airports employ about 6.5 million people, with another 3.1 million working for airlines and many more in other supporting roles around the airport. The role of airports in tourism is equally significant: with nearly 58% of global tourists travelling by air, airports help sustain over 330 million jobs and contribute roughly 9% to global GDP.

Because of their importance in socio-economic development, airports are seen as safe and classically managed assets.

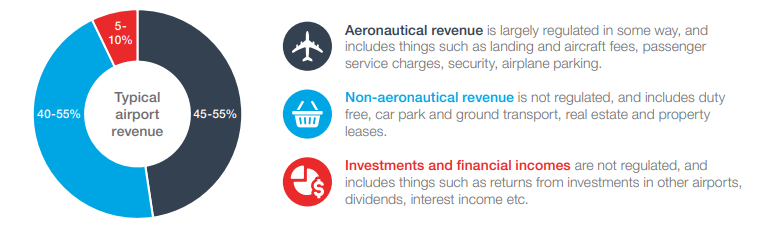

Airports generate revenue through three main streams: aeronautical, non-aeronautical, and investment income – together making up a highly volume-dependent model in which roughly 90 percent of revenues are tied to passenger traffic…

The three core revenue streams, each come with distinct strengths and constraints.

As aeronautical revenues are mostly regulated, they provide stable, predictable cash flows that underpin operations and financing, but offer limited pricing flexibility. Despite a 22% rebound since 2022, they remain 14% below 2019, reflecting their dependence on traffic recovery and regulatory timelines. This volume-linked model could be re-examined, as other sectors, like water distribution or waste collection, show how linking part of revenues to service quality rather than traffic alone may enable more sustainable growth and investment.

Non-aeronautical revenues deliver higher margins and greater commercial freedom, often making them the main profitability driver. Their performance depends on passenger volumes, dwell time, and spending, varying by region – representing 47% of total revenues in the Middle East versus 33% in North America. While consistently outperforming regulated fees, this segment is sensitive to consumer trends: per-passenger revenues have declined by –2.3% CAGR since 2016, highlighting the need for new retail formats and engagement strategies.

Investment income, though smaller, adds diversification and resilience, particularly for large operators with international stakes. Together, these streams combine regulatory stability with commercial opportunity but remain fundamentally volume-driven.

In 2023, total airport revenues were 12% below 2019, despite traffic being only 5% lower, mainly due to a 21% shortfall in non-aeronautical revenues and falling per-passenger profitability. This growing disconnect is pushing airports to rethink commercial models and focus on passenger engagement and high-margin activities.

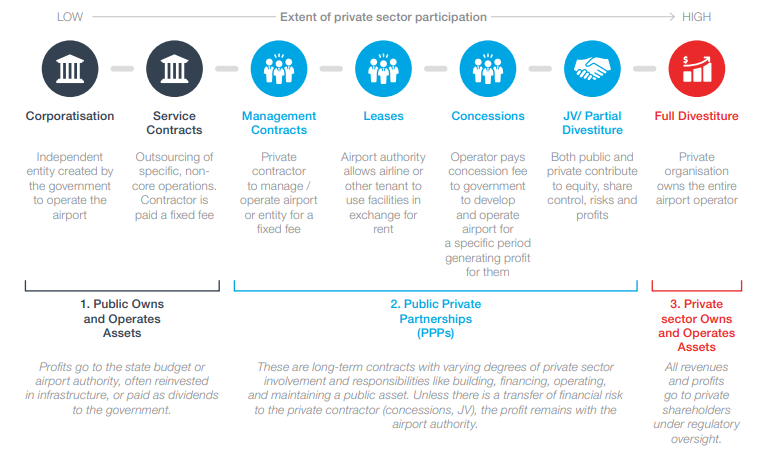

How effectively they do so depends heavily on ownership and operating structures, which shape the incentive for profit, pricing strategies, investment horizons, and the balance between public service and profit.

Ownership and operating models shape airport strategy, profitability, and public value – with multiple models proving successful.

Airports operate under a range of ownership and operating models – public, private, or hybrid – each shaping how revenues are managed, investments are funded, and the balance is struck between public service and profitability.

Public ownership: stable but capital constrained

Most airports remain publicly owned, especially in the US, where nearly all are government-run. Funding is limited with several hundred US airports sharing just $3 billion, forcing many to self-finance and leaving infrastructure outdated. Profitability matters because profitable airports fund upgrades, ease fiscal pressure, and support economies: UK air transport added £14 billion to GDP in 2023, and US airports generated $1.8 trillion in activity and 12.8 million jobs.

Private ownership: commercial focus and efficiency

Private owners focus on maximising profitability, often prioritising long-haul routes with higher fees and per-passenger spend. Since 1987, privatisation has grown, with 437 airports (18% globally) privatised by 2020, including 102 PE-owned.

Private investors typically deliver greater efficiency, better service, and more routes, without significantly higher fees, though commercial priorities can clash with broader stakeholder needs.

A shifting balance – With rising investment needs and limited public funds, more airports are turning to privatisation and PPPs. Ownership models shape how airports balance economic impact, investment, and commercial ambition, a role that will grow as the sector evolves.

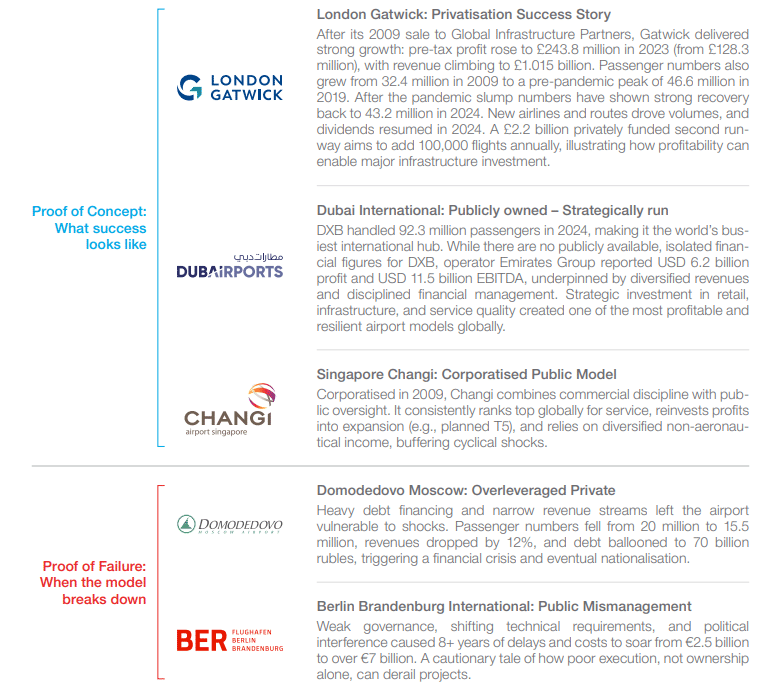

Proof of Concept vs. Proof of Failure: Ownership and Execution in Practice.

Real-world evidence shows there is no single ownership model guaranteeing success, outcomes depend on regulation, governance, investment strategy, and execution quality.

Successful airports pair their ownership model with strong governance, strategic investment, and diversified revenue.

Global studies find no automatic efficiency advantage of private over public, but PE-backed privatisations often deliver higher productivity. Critically, efficiency outcomes depend on regulation, structure, and execution – not ownership alone.

Corporatised public models, well-structured PPPs, and disciplined private operators can all thrive – while poor governance, over-reliance on debt, or misaligned incentives can undermine even the best-funded projects.

Proof of Concept: Dubai International Airport, A Global Success Story

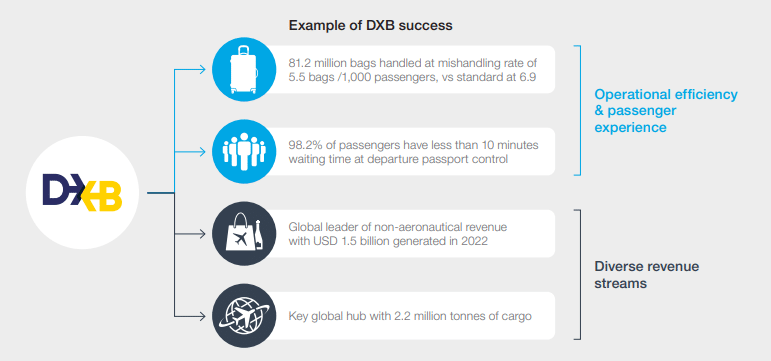

Dubai International Airport (DXB) exemplifies how strategic planning, operational excellence, and long-term investment can drive exceptional profitability and global leadership in aviation. In 2024, DXB handled a record-breaking 92.3 million passengers, cementing its position as one of the world’s busiest international airports. DXB is not just successful by passenger numbers, but also recognised as a top leader in customer experience, consistently ranking among the top airports and winning multiple service excellence awards.

Financially, the Emirates Group, which operates DXB (publicly owned), reported a profit before tax of USD 6.2 billion for the 2024–25 fiscal year, an 18% increase from the previous year, alongside a record EBITDA of USD 11.5 billion and cash assets totaling USD 14.6 billion, reflecting strong profitability and liquidity.¹

DXB’s success stems from a combination of high passenger throughput, operational efficiency, and diversified revenue streams. Much of this operational efficiency reflects the close alignment between airport operators and government authorities in the Middle East, where swift decision-making and fewer data-privacy constraints enable smoother passenger flows and faster infrastructure development. On the other hand strategic investments in infrastructure, technology, and customer service have enhanced both service quality and non-aeronautical revenues, such as retail, dining, and premium services. Looking ahead, Dubai Airports plans a USD 35 billion expansion at Al Maktoum International Airport, which will become the world’s largest terminal with capacity for up to 260 million passengers, reinforcing Dubai’s position as a global aviation hub.

Despite the scale of its operations, Dubai has maintained prudent debt management, with total outstanding debt at AED 112.4 billion and a debt-to-GDP ratio of 22%, ensuring financial stability while pursuing ambitious growth.

Key Takeaway: DXB demonstrates high traffic volumes, operational efficiency, strategic infrastructure investment, and effective financial management, creating one of the most profitable and resilient airports globally.

The Future of Airport Profitability: Digital Transformation, Real Estate Expansion, and Smarter Regulation.

As airports emerge from the turbulence of recent years, they face a fundamentally different operating environment.

Passenger volumes are returning, but revenues per traveller remain below pre-pandemic levels, and inflation, capacity constraints, and sustainability pressures are reshaping how airports must think about profitability. The old model, relying largely on traffic growth to lift revenues, will no longer be sufficient. Instead, airports are pivoting towards new commercial strategies, digital transformation, real estate development, and regulatory innovation to build more resilient business models.

Digitalisation is transforming passenger engagement and unlocking new commercial value, enabling airports to grow non-aeronautical revenues without raising prices.

Airports are rapidly adopting seamless payments, pre-order platforms, personalised marketing, and AI-driven pricing to deepen engagement and unlock new revenue streams. These tools boost conversion rates and basket sizes, while generating data to refine marketing and operations. By embedding digital touchpoints throughout the journey, airports create richer, more profitable interactions without raising prices.

London Heathrow has rolled out a comprehensive digital commerce platform, including Heathrow Boutique, which allows passengers to pre-order retail and duty-free items online for collection at the airport. It also uses personalised marketing and dynamic pricing in parking, leveraging AI and CRM data to optimise yield.

Munich Airport has implemented AI-driven dynamic pricing for parking and a suite of mobile commerce tools to support pre-ordering and targeted promotions. The airport’s digital marketplace strategy is often cited as a best-practice example in European airport commercial operations.

Airports are turning real estate into a strategic profit engine, expanding beyond terminals to unlock new, diversified revenue streams.

Airports are increasingly developing logistics hubs, hotels, offices, and vertiports (landing hubs for vertical take-off and landing), making real estate a core growth driver. Research shows that scale and smart use of commercial space – especially F&B and retail – boost efficiency and profitability.

Projects like Jewel Changi, with its extensive retail, leisure, and hospitality offer, show how airports can become multi-use destinations that attract travellers and locals, creating more stable, diversified revenues. Attractive, engaging environments also encourage longer dwell times, driving higher retail and F&B spend.

Amsterdam Schiphol has developed a large-scale AirportCity model, including Schiphol Real Estate, which manages offices, hotels, logistics hubs, and retail areas. The airport’s real estate arm is a key contributor to profitability, accounting for a significant share of non-aeronautical revenues and positioning Schiphol as both a transport hub and a business district.

Another major trend is broadening commercial activity through on-arrival duty-free and landside retail for non-travellers, expanding revenue pools and smoothing peak-time dependency without major airside investment. Efficient public transport and fast city connections are essential to enable these strategies.

Delhi Airport is directly linked to the city centre via the Delhi Airport Metro Express, offering a 20-minute high-speed connection that has boosted both passenger convenience and landside footfall. This connectivity has been a key enabler of Delhi’s successful airport city development, supporting retail, hospitality, and commercial growth around the airport.

Regulation and financing are key enablers of investment, shaping the pace of airport transformation.

Light-handed, stable regulation and dual or hybrid till models align incentives and lower the cost of capital, encouraging airports to invest in commercial development. At the same time, PPPs and long-term infrastructure funds are providing essential financing for modernisation, capacity expansion, and digital upgrades. Together, these frameworks increasingly determine how quickly airports can unlock new revenue streams and improve services.

Santiago International Airport is a PPP concession success story, benefiting from clear, stable concession agreements and predictable regulatory terms. This framework has attracted long- term infrastructure fund investment, enabling the construction of a new international terminal and significant commercial development, accelerating its transformation into a modern regional gateway.

Sustainability is now a core financial and strategic driver for airports.

Hundreds of airports, especially in Europe, have set net-zero roadmaps tied to green finance mechanisms. From eco- retail and energy-efficient hotels to carbon offset programmes and electrified ground operations, sustainability measures are no longer optional. They shape investor appetite, brand reputation, and regulatory compliance, making them central to long-term competitiveness.

Swedavia, which operates 10 Swedish airports including Stockholm Arlanda, became carbon neutral across its operations in 2020, one of the first national airport groups to do so. It uses green energy, biofuels for ground operations, and sustainable construction standards, and funds its initiatives through green bonds and climate-linked financing. Swedavia’s sustainability leadership has enhanced its reputation and access to favourable capital markets, reinforcing its competitive positioning.

Together, these developments point to a future in which profitability is less about the sheer number of passengers and more about how effectively airports use their assets, data, and partnerships. Airports that embrace digital transformation, expand into real estate and hospitality, adopt enabling regulatory frameworks, and integrate sustainability into their commercial strategies will be best positioned to thrive in the next era of aviation.

Conclusion/Summary

Airports at a Defining Crossroads

Airports stand at a pivotal inflection point. Having rebuilt resilience after the industry’s greatest crisis, they now face long-term shifts that will redefine their purpose and profitability. Evolving passenger expectations, climate pressures, and a changing revenue model are reshaping what airports must be: not only transport infrastructures, but adaptive

businesses that create value beyond passenger volumes.

Passenger behaviour is shifting as business travel declines and leisure, visiting friends and relatives, and price-sensitive travellers dominate. Mature markets face capacity, regulatory, and modal-shift constraints, while emerging economies expand connectivity and infrastructure. In this environment, airports must move beyond throughput to deliver seamless, meaningful experiences that increase dwell time, justify premium services, and integrate airports into wider mobility ecosystems.

Climate change adds structural pressure, from rising physical risks to tighter carbon regulation and investor scrutiny. With most emissions tied to in-flight activity, airports must play an active role in the energy transition – enabling SAF, electrification, resilient infrastructure, and green financing. Sustainability is becoming a fundamental driver of competitiveness and access to capital.

Financially, the predominantly volume-linked model is no longer sufficient. Non-aeronautical revenues remain critical yet volatile, and airports must diversify through digitalisation, real estate development, multimodal integration, and new commercial ecosystems. Governance, investment discipline, and a shift towards long-term value creation will define future success.

A New Airport Paradigm: Balancing People, Planet, and Profit

The airports that lead the next era will be those that:

- Put passengers – their expectations, wellbeing, and time – at the centre of strategy.

- Treat sustainability as a competitive advantage and financing lever.

- Diversify revenue through digital, real estate, and multimodal platforms.

- Invest with long-term discipline, supported by strong governance.

People will always need airports – but they increasingly need airports that deliver more than connectivity. Those that strengthen communities, reduce environmental impact, and create genuine value will remain relevant, resilient, and profitable. In a world shaped by climate urgency and changing mobility, airports that align people, planet, and profit as mutually reinforcing pillars will define the future of global aviation.

As the sector evolves, a critical question emerges: if airports are no longer defined by traffic alone, how should they be remunerated? Around the world, infrastructure sectors are moving away from purely volume-based models toward frameworks that reward service quality, resilience, sustainability, and passenger experience. Airports may soon

follow – shifting from asking “How many passengers did we process?” to “How well did we serve them, how sustainably did we operate, and how resilient is the system we manage?” One needs to consider what a future-ready airport business model could look like – one where value is created not just by moving people, but by serving them better, cleaner, and

more efficiently than ever before.

Nicolas Bourdon – Partner, Accuracy

Zaheer Minhas – Partner, Accuracy

Christy Howard – Partner, Accuracy

Joris Timmers – Partner, Accuracy

Julie Malzac – Director, Accuracy

Thierry de Séverac – Advisor, Accuracy

What does the future hold for airports? Riding high on tailwinds or bracing for turbulence?

Note:

¹Financials are for entire Emirates Group, not just those related to the operation of DXB