Flying into turbulence: airports in the context of climate change

The aviation sector accounted for roughly 2.5% of global CO2 emissions in 2024, a share that could rise to around 4% when considering non-CO2 effects such as contrails (condensed water vapour left behind by aircraft engines at high altitudes), and other greenhouse gases. For context, emissions from the aviation sector are three times higher than France’s total annual emissions.

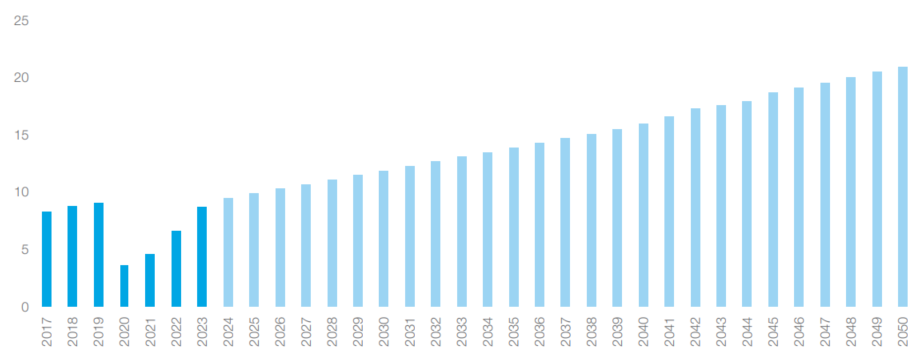

At the same time, around 80% of the world’s population has never taken a flight. As global population and living standards continue to rise, demand for air travel is expected to grow substantially—making it all the more urgent to identify sustainable pathways to decarbonise the sector. According to the Airport Council International (ACI), in 2024, global passenger traffic reached 9.5 billion. The ACI projects that passenger traffic could reach more than 16 billion by 2040 and more than 20 billion by 2050.

Passenger traffic forecast (bn passengers)

Source: Airport Council International

This article explores physical, financial and transition risks challenging the current airport model while also imagining potential solutions for building a sustainable airport model, capable of aligning environmental imperatives with the long- term resilience of the aviation industry.

I. Mounting pressures on the airport business model

Airports’ business models face physical, financial and transition risks that put the model under pressure.

Increasing exposure to climate hazards: the physical impact of climate change on the aviation sector

Beyond transition risks, airports also face growing physical risks. Many airports are located in low-lying coastal areas, making them highly vulnerable to sea-level rise and flooding. A 2021 study focusing on 1,200 airports concluded that 269 are currently at risk, a number projected to increase by 30% by 2100 even under a 2°C warming scenario. Extreme weather events—such as storms, heatwaves, and flooding—are expected to disrupt operations more frequently. For instance, during the 2017 heatwave in Arizona, temperatures grounded more than 50 planes, highlighting the sensitivity of airport operations to climate extremes. According to a Eurocontrol study, a one-day closure of an airport due to severe or partial flooding could potentially affect around 0.5% of daily air traffic movements at medium-sized airports and 2–3% at large airports in Europe.

At the same time, climate change is intensifying atmospheric turbulence by increasing the temperature contrast between warm and cold air masses that form the jet stream. This leads to greater wear and tear on aircraft and longer flight times as pilots adjust routes to avoid unstable conditions, rising operational costs, and decreasing demand due to passengers’ turbulence fear.

These growing physical threats are compounded by the vulnerability of aging airport infrastructure and the tightening of insurance conditions, as rising premiums and reduced coverage in high-risk zones increasingly pressure operators to invest in resilience upgrades.

Evolving financial exposure and opportunities: climate risk is reshaping aviation finance

Climate change is fundamentally reshaping access to capital in the aviation sector.

Investors and financial institutions are increasingly redirecting funds toward assets aligned with environmental, social, and governance (ESG) standards, leaving carbon- intensive infrastructure exposed to reduced financing options.

In 2022, for instance, the European Investment Bank halted the payment of a €200 million loan to expand Budapest Airport due to the absence of an environmental impact assessment covering air and noise pollution as well as greenhouse gas emissions.

This shift reflects a broader trend: airports lacking credible decarbonization strategies face reduced access to capital, higher financing costs, and potentially lower credit ratings as lenders and investors price in transition and physical climate risks.

At the same time, climate finance is a real opportunity for actors in the industry to shift towards sustainability.

How climate finance is reshaping how airports raise capital

Sustainability is reshaping airport investor models and capital allocation.

Regulatory pressure and transition challenges: Carbon pricing and emissions trading schemes increase operating costs for airlines and airports

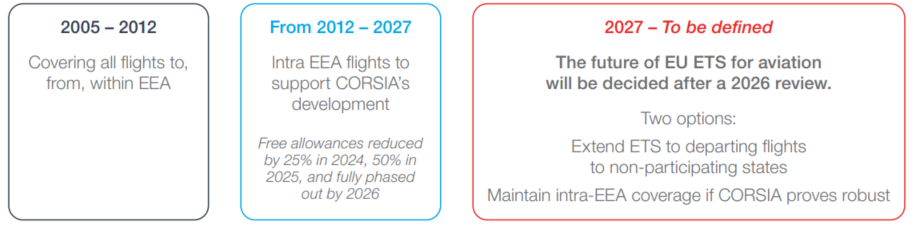

Under the EU Emissions Trading System (EU ETS), all airlines operating in Europe are required to monitor, report and surrender allowances against their CO2 emissions.

- As of now, the impact is limited as allowances are freely distributed by the European Commission, but the scope of this regulation is limited to flights within the EU as the regulator aims at enabling the development of the global Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) system.

- As free EU ETS allowances are phased out, airlines must buy carbon credits, driving up operating costs. This squeezes margins, reduces cash flow, and cascades to airports through lower traffic and revenues. For investors, this means lower IRR, longer payback periods, and higher cash flow volatility.

EU ETS

Source: Aviation benefits beyond borders

CORSIA implementation

Source: Aviation benefits beyond borders

II. The decarbonization challenge

Where do airports’ emissions really come from?

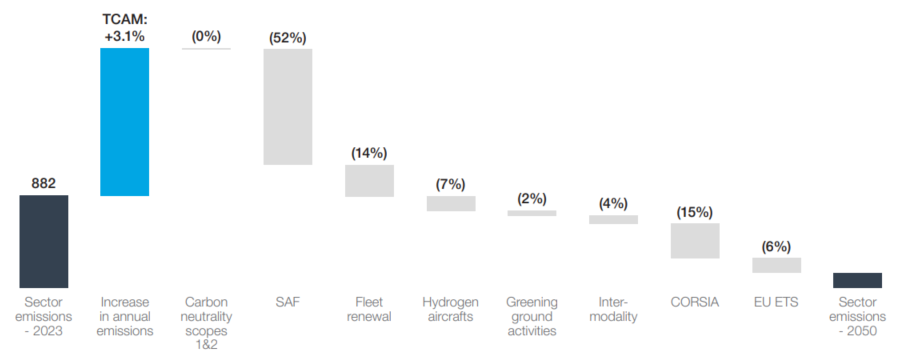

Although the industry has committed to achieving carbon neutrality by 2050, there is still no global consensus on a carbon budget specifically allocated to international aviation. The International Energy Agency has warned that the aviation sector is “not on track” to meet the Net Zero Emissions by 2050 scenario. The Climate Action Tracker has rated the sector’s efforts to meet decarbonization targets as “critically insufficient.”

While technological innovation, particularly through the development and adoption of sustainable aviation fuels (SAF), will play a pivotal role, the level of technological maturity of such technological innovation makes it impossible to achieve net zero by 2050 without a reduction in flight demand.

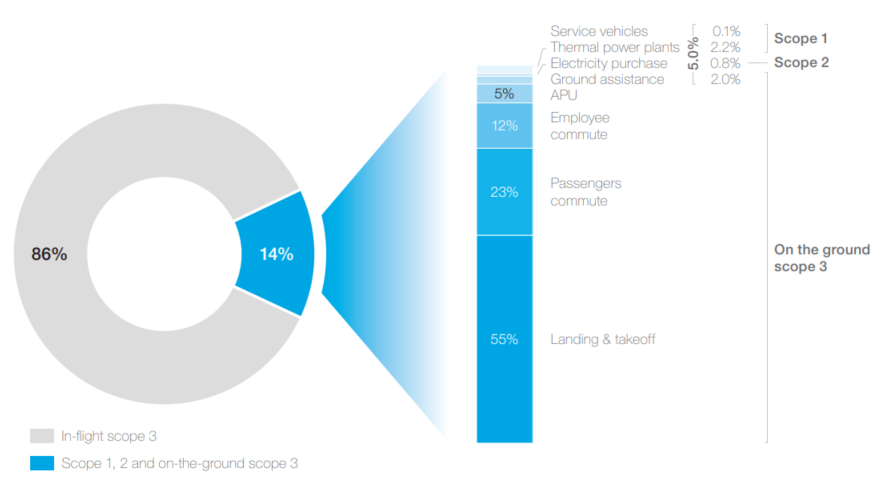

The vast majority of the 900 million tons of CO2 emitted each year from the aviation sector stem from in-flight activities (scope 3).

For an airport, 86% of total emissions are attributed to in-flight operations (scope 3), while the remaining 14% are associated with ground operations — both from the airport itself (scopes 1 and 2) and from airlines’ on-the-ground activities (scope 3). Within ground emissions:

- The largest contributor is the LTO (Landing and Take-Off) aircraft cycle, accounting for 55%

- Passenger access to the airport accounts for 23%

- Employee access to the airport accounts for 12%

- Smaller contributors include the Auxiliary Power Unit (5%), power plants (2.2%), ground assistance (2%), and minor sources such as electricity (<1%) and the airport vehicle fleet (0.1%)

This breakdown underscores the dominance of in-flight emissions while also revealing key areas for ground-side decarbonization efforts.

Airports’ carbon footprint by scope of emissions

Decarbonising airports: from runways to renewable pathways

To decarbonise the industry, innovative paths exist, yet technological limits and uncertainties cloud the way.

Airports’ decarbonization strategies must address both operational emissions (Scope 1 & 2) and value chain emissions (Scope 3). While reducing operational emissions is crucial, tackling Scope 3 is the real battleground, as it accounts for 95% of an airport’s total carbon footprint.

Scope 1, 2, and on-the-ground-scope 3 decarbonisation

For airports’ operations emissions (scope 1&2) and on-the-ground emissions (scope 3), main decarbonisation levers reside into operational innovation.

Enhanced energy efficiency within airports, such as more energy-efficient buildings and eco-friendly vehicle fleets, are a necessary step, but will only decarbonise a small portion of industry emissions.

- Switching to renewable energy sources for airport operations can reduce scope 1 and 2 emissions by up to 50%, but this is only a fraction of the total emissions attributed to aviation.

- Reducing emissions during the taxiing phase by using only one engine or replacing the Auxiliary Power Unit (APU) with ground-based green electricity can cut emissions. Such measures could reduce fuel consumption during taxiing by up to 20% (World Economic Forum).

In flight-scope 3 decarbonisation

Key decarbonisation levers for in-flight scope 3 emissions are technological innovations and in-flight operational improvements. Technologically speaking, main efforts are concentrated into Sustainable Aviation Fuels (SAFs and hydrogen).

- Sustainable Aviation Fuels (SAFs), produced from non-petroleum sources such as biomass or synthetic processes, can cut aircraft CO2 emissions by up to 80% and are currently the most viable path to net-zero aviation. Yet, their deployment remains constrained by high costs and limited supply — global production reached 2.5 billion litres in 2025 (less than 0.7% of aviation fuel use), while 450 billion litres will be needed annually by 2050. Meeting this demand would require 3,000–6,500 new renewable fuel plants and around $128 billion in yearly investments. SAFs are particularly critical as they remain the only scalable decarbonization solution for long-haul flights, which account for just 6% of flights but over half of aviation’s total emissions.

SAF deployment

- Low-carbon hydrogen is another promising aviation fuel, mainly suited for short-haul flights due to storage and weight constraints. Its potential to cut aviation emissions—around 6% by 2050—depends on the use of green or blue hydrogen, yet 99% of current production still relies on unabated fossil fuels. Green hydrogen remains costly and scarce, competing with other sectors for supply. To meet projected aviation demand of up to 100 million tons annually by 2050, significant advances in storage, propulsion technologies (e.g., Airbus ZEROe), and large-scale low-carbon hydrogen production will be essential.

Hydrogen aircraft deployment

Developing these technologies demands significant investments, with benefits that will only be felt in the long term, while immediate actions are necessary. The global investment required to achieve net-zero emissions in aviation by 2050 is estimated to be around $5 trillion (ICCT). While assessing decarbonization options for the industry, one must keep in mind that the production of biofuels can also negatively impact agriculture and biodiversity. For instance, large-scale biofuel production could lead to deforestation and loss of biodiversity if not managed sustainably. The extraction of resources needed for electric aircraft batteries also poses environmental problems, such as the mining of lithium and cobalt, which can have significant ecological and social impacts. Decisions will therefore need to strike a balance, ensuring that the decarbonization of the aviation sector does not occur at the expense of other environmental or social priorities.

How regional dynamics shape the airport transition

EUROPE

Airports lead the transition under strict EU rules and investor pressure, with SAF and green financing gaining traction. Oslo Airport (Norway) for instance offers commercial-scale SAF refueling and renewable energy operations. Yet, smaller airports struggle with costs, and hydrogen infrastructure remains limited. Physical risks are significant: coastal hubs like Schiphol face growing threats from sea-level rise and storm surges.

NORTH AMERICA

Green bonds and electrification dominate, as seen in Los Angeles and Orlando (United States), supported by state-level mandates. However, SAF supply chains remain fragmented, and the absence of federal mandates slows progress. Heatwaves in the Southwest increasingly disrupt operations, grounding flights and raising cooling costs.

ASIA PACIFIC

Energy hubs and multimodal links are emerging, with Cochin Airport (India) fully solar-powered and Incheon (South Korea) investing in logistics and technology parks. Still, SAF infrastructure is scarce and regulation less ambitious than in Europe, limiting progress. Typhoons and flooding pose severe risks for coastal megahubs like Bangkok and Manila.

MIDDLE EAST

Dubai (UAE) and Doha (Qatar) push hydrogen and SAF projects tied to national energy strategies, aiming to position the region as a green aviation leader. Yet, reliance on fossil fuels and extreme heat complicate progress, especially for hydrogen storage. Heat stress is the main physical risk, increasing cooling costs and operational challenges.

LATIN AMERICA & AFRICA

Progress is slower due to financing gaps and outdated infrastructure, despite some renewable energy pilots. Regulatory pressure is limited, and SAF adoption remains marginal. Coastal airports such as Lagos and Rio face growing flood and storm surge risks, threatening long-term resilience.

Nicolas Bourdon – Partner, Accuracy

Zaheer Minhas – Partner, Accuracy

Christy Howard – Partner, Accuracy

Joris Timmers – Partner, Accuracy

Julie Malzac – Director, Accuracy

Thierry de Séverac – Advisor, Accuracy

What does the future hold for airports? Riding high on tailwinds or bracing for turbulence?