Why is the remaining portion of inflation proving so difficult to overcome? Adapting monetary policy has worked well to rein in the alarming inflationary trends experienced over the past couple of years, but it is struggling to finish the task of slowing economic activity and bringing consumer price growth down to target levels. In this edition of the Economic Brief, we will examine the situation in the US in a bid to explain this resilience.

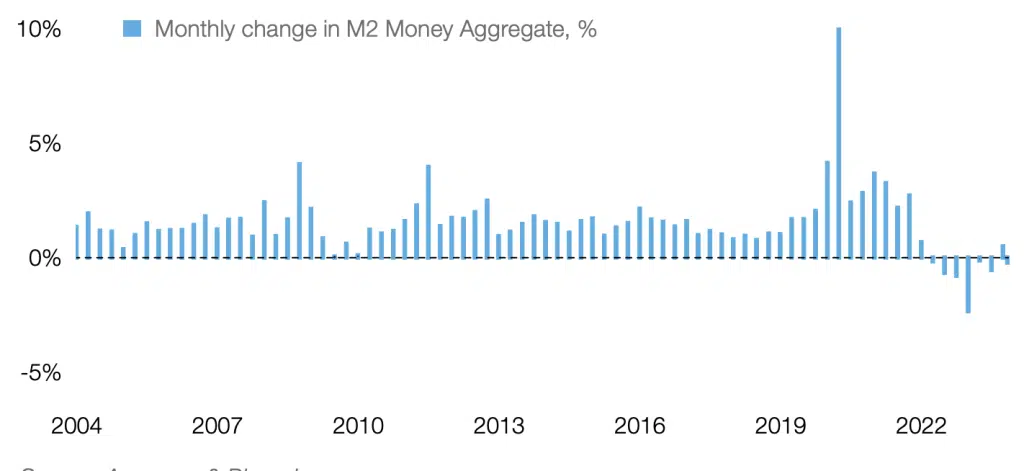

United States: money supply increased considerably during the pandemic

Our first angle is to view the current situation in its wider context and note that it is highly original – not just in the US but in the West generally. Coming on the back of the Covid-19 crisis, this extended period of inflation has some unusual characteristics. First, money supply is considerable. During the pandemic, money supply increased vastly, as part of governments’ efforts to support their economies during periods of lockdown. The graph opposite shows the development of money supply over the period. As we can see, although it started to decrease in 2023, a significant amount of liquidity remains in the system, much of which held in savings. This spare liquidity counters the Fed’s efforts of raising interest rates, as many consumers dip into their savings to maintain their lifestyles.

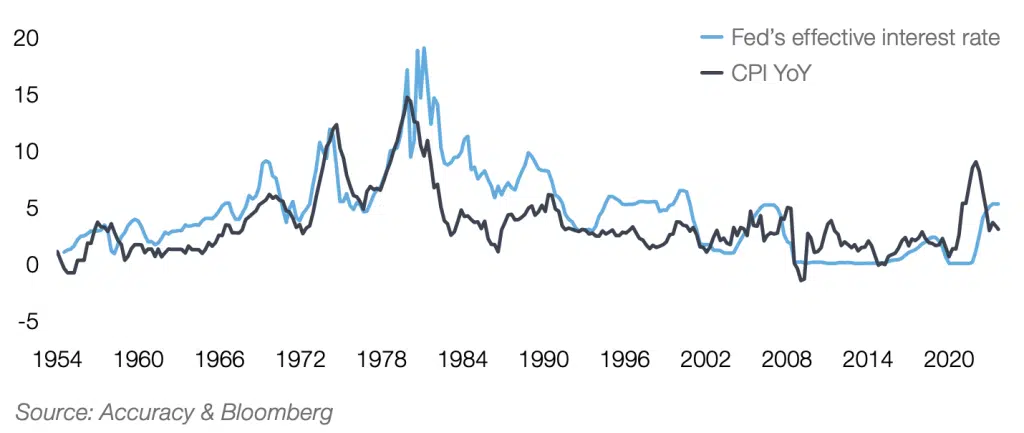

United States: the rise in interest rates only started after the inflation peak

The singularity of the current situation also becomes apparent when we review the timing of the actions taken. In a typical scenario of rising consumer prices, the central bank raises interest rates as soon as possible to cool down demand. However, as we can see in the graph opposite, the Fed did not begin taking these countermeasures until the inflation peak had been reached, several months later. The reason for this delayed reaction is simple: the Covid-19 crisis had already dealt a considerable blow to the economy in the preceding few years. The fall in economic activity during the pandemic was such that the Fed did not wish to risk hamstringing the economy’s recovery by raising rates too quickly.

The combination of these elements, high money supply and delayed countermeasures, has led to a slower reaction and thus greater difficulty in bringing the situation under control.

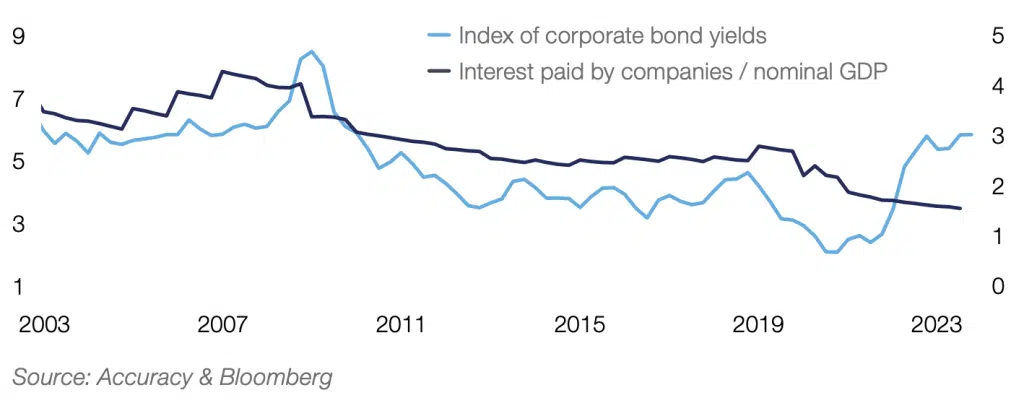

US companies: a debt-to-GDP ratio that is currently unaffected by rising interest rates

Another factor that is contributing to the stickiness of inflation is the financial situation facing US companies. At present, the cost of corporate debt remains low. Indeed, despite the rapid rise in interest rates in the past few years, the level of interest payments on corporate debt continues to fall when shown in relation to GDP, as illustrated in the graph opposite.

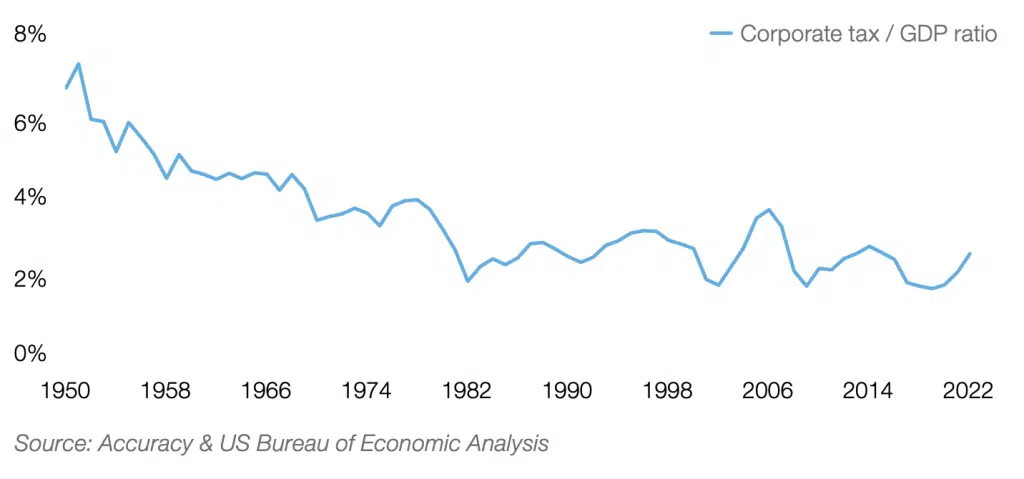

United States: the corporate tax burden remains low

What is more, the same can be said of tax. When we review the corporate tax charge in relation to GDP, we see a figure that has been trending downwards for the past half century. All of this contributes to a high level of inertia for corporates, giving them much leeway to act in spite of the effects of the monetary policy in force.

The interplay of all of these forces goes a long way to explain why the last portion of inflation is proving so troublesome and tricky to master.

One last area of interest remains in our case study of the US: how companies are financing themselves on the capital markets. For the past two decades before their recent rise, interest rates were low. This meant that it was simple for companies to issue debt to finance their development, something that had a corresponding impact on the number of public listings: 20 years ago, the US counted 7,500 listed companies; today, that number is just 4,000. But with the rise of interest rates and share indices reaching record highs, the appeal for companies to finance themselves via shares may be growing. In fact, this shift may already be bearing fruit: the number of IPOs grew by 8% in 2023.