Growth Amidst Uncertainty

As the global community accelerates efforts to mitigate climate change – albeit with a recent major exception in the form of the U.S. under President Trump – the shift from internal combustion engine (ICE) vehicles to electric vehicles (EVs) has emerged as a linchpin of decarbonisation strategies. Yet, the transition is contingent on one critical element: charging infrastructure. Without widespread, reliable and easily accessible charging options, the full potential of EV adoption risks stalling, limiting its role in reducing emissions.

The surge in EV ownership across Europe has prompted governments and industries to respond with unprecedented levels of investment in charging networks. The Netherlands, Germany and France lead the way, setting the pace for infrastructure development. However, this rapid growth belies a paradox: the market is scaling quickly, but profitability remains elusive.

Despite billions of euros in public subsidies and private investment, the financial viability of EV charging infrastructure is far from assured. In this article, we dissect the intricacies of the EV charging ecosystem, exploring the forces driving expansion, the emerging business models, the competitive landscape, and the persistent barriers to profitability. Can sheer scale unlock lasting success, or does the market require a fundamentally different approach?

The rapid pace of EV adoption also brings a host of logistical, technical and economic challenges. From ensuring grid capacity to navigating fragmented regulatory frameworks across borders, the road to a mature and profitable EV charging ecosystem is fraught with complexity. As public policy, private investment and consumer behaviour intersect, the stakes are higher than ever. Can the industry resolve these issues in time to support the global push for decarbonisation, or will the infrastructure gap frustrate the EV revolution?

Fundamental Concepts of EV Charging Infrastructure

EV charging infrastructure can be broadly categorised into three levels, distinguished primarily by their charging speed and power output:

- Level 1: This level uses standard household outlets (120 V) to provide about 6–8 km of range per hour of charging. Best suited for overnight home use, these chargers are easy to set up and widely accessible. However, their slow charging rate may limit practicality for users needing faster charging options.

- Level 2: Offering 3.4–22 kW of power output, this level enables about 40–120 km of range per hour of charging. These stations are faster and can be installed at residential locations but require professional installation and involve higher upfront costs. Level 2 chargers are commonly found at residential, public parking, company parking and commercial locations, and they constitute the majority of public EV chargers.

- DC fast chargers: Providing anywhere from 50 kW to over 350 kW of power output, these chargers are capable of charging certain EVs to 80% capacity in just 15 to 30 minutes, making them ideal for when time is critical. Their high costs and low availability, however, mean they are less accessible for daily use.

The differences between public and private EV charging infrastructures highlight the current imbalance between accessibility and efficiency:

- Public charging stations: Public stations are accessible to all, often located in high-traffic areas such as motorways and urban centres. However, they regularly come with higher use fees and may involve issues like long wait times and charger congestion due to high demand.

- Private charging solutions: Typically installed at homes or businesses, these charging stations are unavailable to the broader public as their access is restricted. They offer the convenience of charging at private premises and benefit from lower electricity rates. Nonetheless, they face challenges such as regulatory hurdles, including zoning and electrical capacity limits, and the significant cost of installation, especially in older buildings or areas without existing infrastructure.

The State of the EV Charging Market: A Snapshot

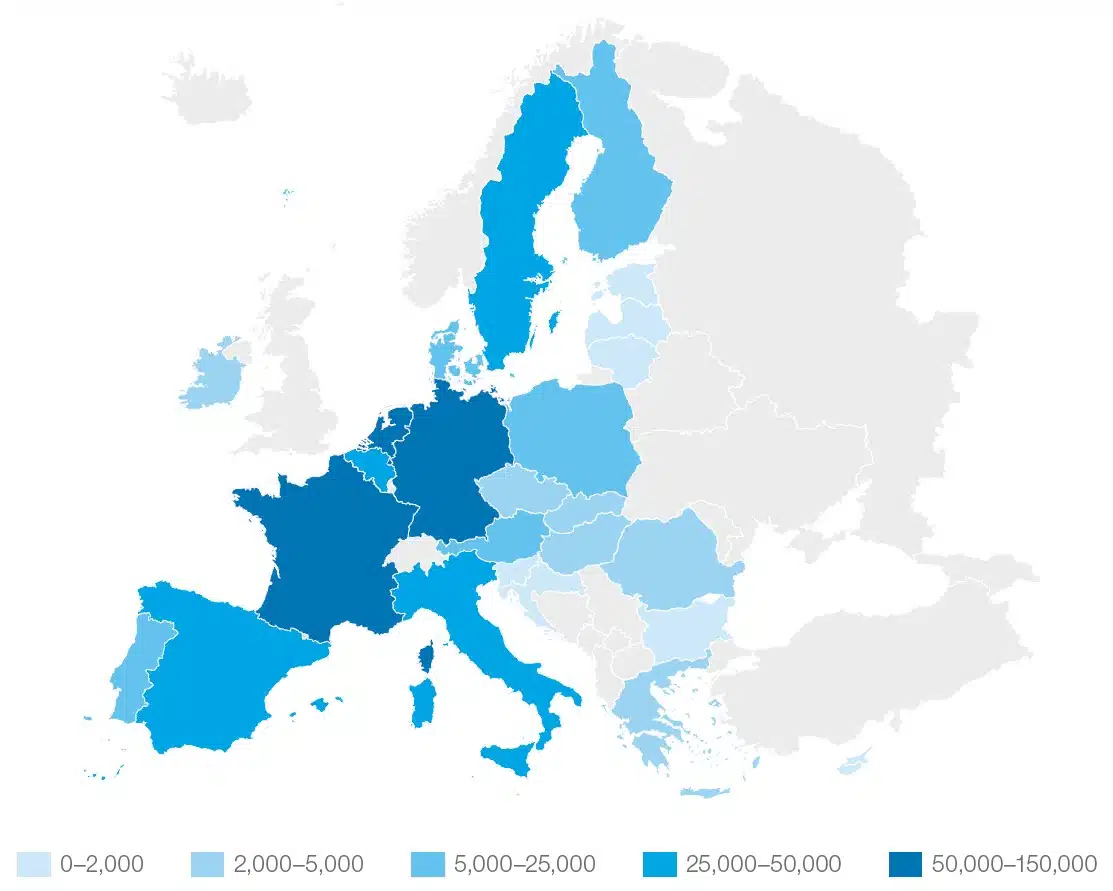

The EV charging market is growing rapidly across Europe, driven by ambitious climate policies, shifting consumer preferences, and technological advances. However, this growth is not without its challenges. In countries like the Netherlands, Germany and France, dense networks of charging stations are emerging, with a mix of urban fast-charging hubs and residential slow chargers. The countries’ efforts reflect the complexity of building a truly inclusive and accessible charging network that caters to all types of users (see case studies below).

However, beneath the surface of the market’s rapid expansion lies a more complicated reality. Charging point utilisation rates vary significantly from region to region, and for many operators, becoming profitable remains a distant goal. This discrepancy underscores a fundamental challenge: while demand for electric vehicles continues to surge, the economics of charging infrastructure often fail to keep pace. This creates a fragmented market where rapid growth is frequently contrasted with financial instability and slow returns on investment.

Figure 1 – Distribution of EV charging points across the EU

Source: ACEA

The Market Evolution: From Niche to Necessity

The EV charging market has undergone significant transformation in recent years. What was once a niche offering is now a critical component of national energy and transport strategies. In the early 2010s, charging networks were sparse, primarily confined to urban areas. Today, they span cities, motorways and even rural regions, reflecting the widespread adoption of electric mobility.

This shift has been driven by regulatory changes, technological advances and the increasing willingness of industries to collaborate. The introduction of ultra-fast-charging technology has dramatically reduced charging times, addressing one of the key barriers to EV adoption. Moreover, the push for interoperability across different charging networks has made it easier for consumers to access a broader range of charging points, further encouraging EV adoption. However, growth has not always been linear. Regulatory pushes have often outpaced market readiness, leaving charging networks with underutilised stations and prolonged payback periods.

While the infrastructure is expanding at pace, profitability issues have become evident. The recent surge in charging stations has unfortunately not been accompanied by proportional demand or utilisation, and the same regulatory pressure and technological innovations that have spurred growth also highlight the need for smarter, more strategic investment. As the market grows, the question of whether expansion alone can support profitability becomes central. How can operators scale effectively while ensuring a return on investment in such a fragmented market?

Scaling up: Bridging Ambition and Reality

The market’s trajectory is also being shaped by the dynamic business outlook in the EV sector. With EV sales in Europe on an upward trend, demand for EV charging infrastructure is also expected to rise. By 2030, the anticipated addition of 11 million battery electric vehicles in corporate fleets is projected to create an annual demand of 100 billion kWh, signalling the need for substantial growth in the EV charging infrastructure market.

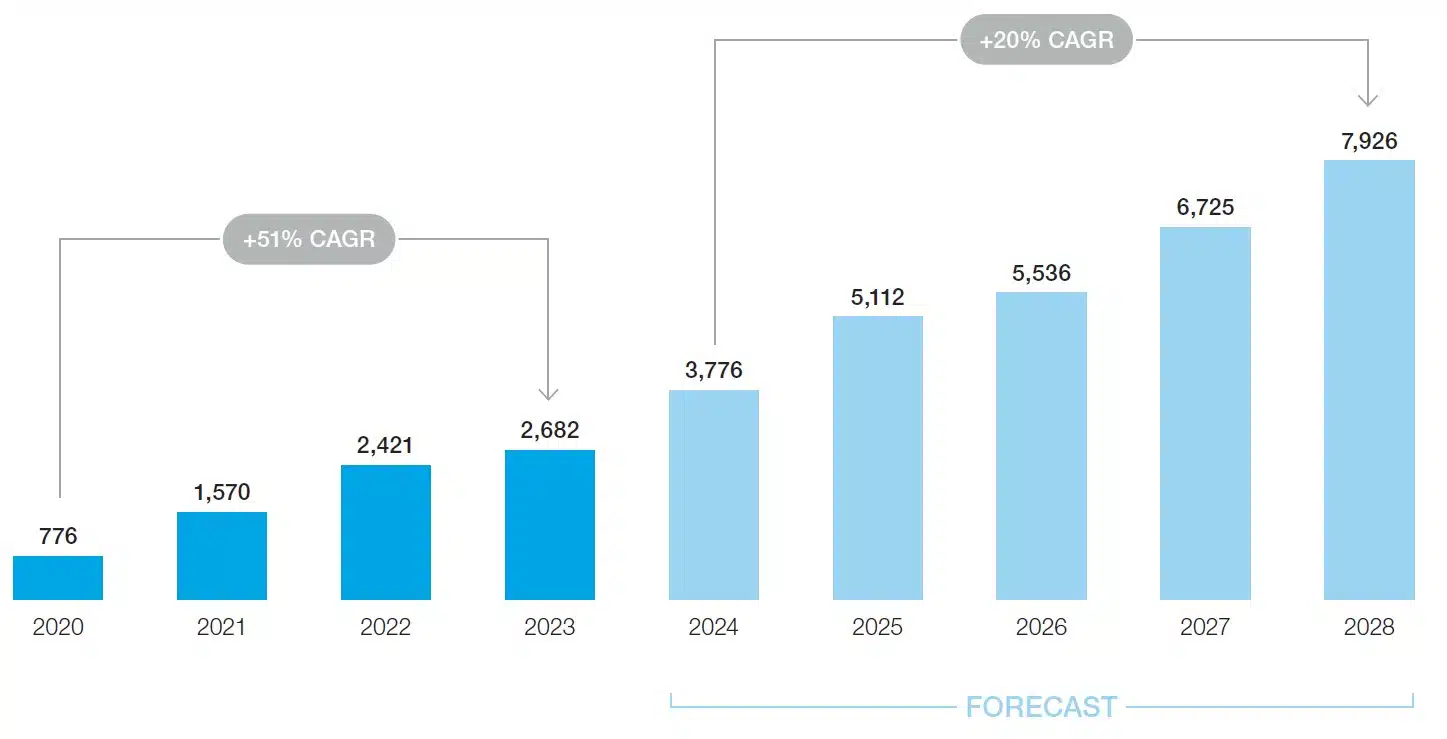

Figure 2 – European EV charging infrastructure market size and outlook (€ million)

Source: GlobalData

Between 2020 and 2023, the market expanded significantly from €776 million to €2,682 million, representing a compound annual growth rate (CAGR) of 51%. Looking ahead, it is expected to continue its robust expansion, albeit at a slightly slower pace: from 2024 to 2028, it is forecast to grow at a CAGR of 20% to reach €7,926 million.

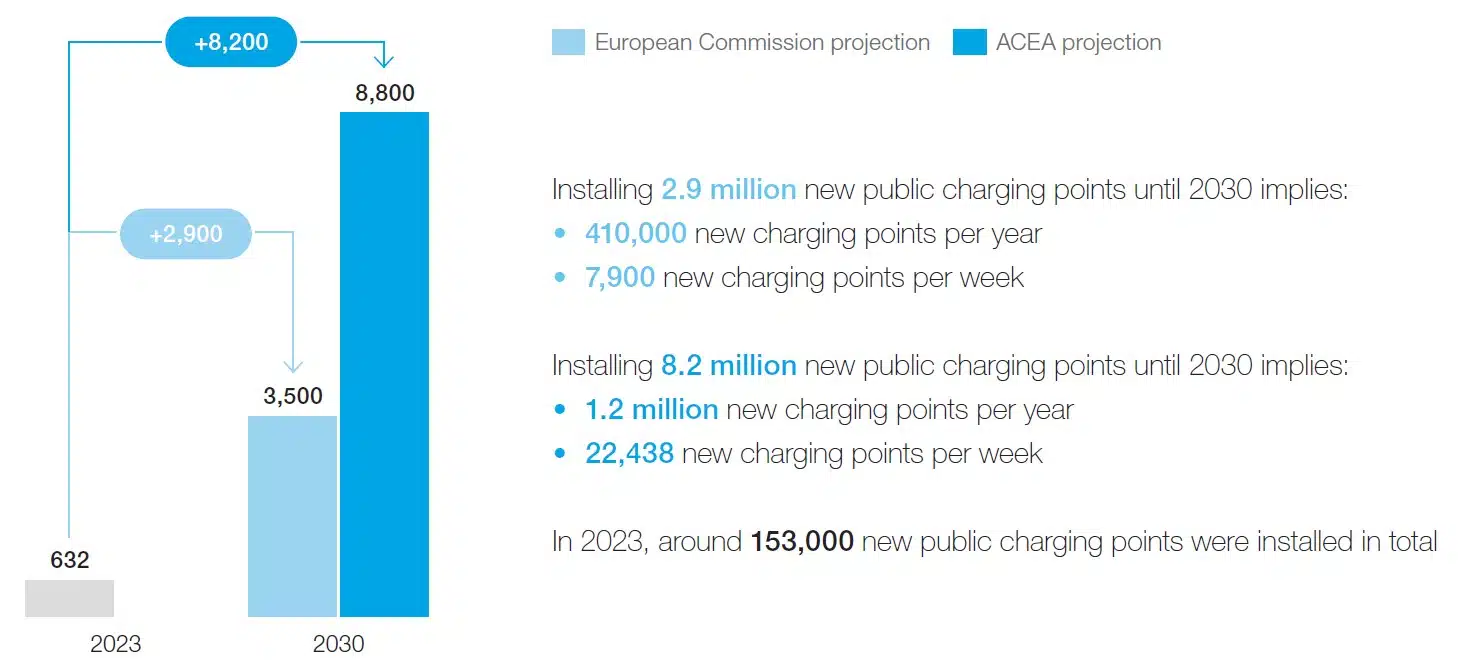

However, there is a significant disparity between growth projections from different stakeholders. The European Commission’s forecasts, aligned with its objective of a 55% reduction in CO2 emissions from passenger cars by 2030, estimate that around 2.9 million public charging stations will be required within that timeframe. In contrast, the European Automobile Manufacturers Association (ACEA) projects a far higher demand, estimating the need for 8.2 million charging points by the same year. This suggests a considerable misalignment between regulatory targets and industry expectations, with the ACEA forecast requiring 1.2 million chargers to be installed per year, compared with just 410,000 installations per year to meet the European Commission’s target. For context, 153,000 new public charging points were installed in 2023.

Figure 3 – Public charging points available in the EU (units, thousand)

Source: ACEA

This gap identifies potential market growth but also highlights significant concerns about the sector’s ability to meet these ambitious targets while maintaining profitability – and, by extension, securing adequate financing. To address this shortfall, collaboration between manufacturers, charge point operators and policymakers will be crucial. Ensuring the rapid expansion of infrastructure to keep pace with EV demand will require either a profitable market outlook or continued government intervention to facilitate growth.

Current energy infrastructure often lacks the capacity to support the widespread deployment of high-demand fast-charging stations, necessitating significant upgrades and integration with advanced energy management systems. Standardisation and compatibility issues across different networks, long investment payback periods and the looming risk of technological obsolescence further complicate the market landscape. Utilisation rates remain low for much of the year, spiking only during peak travel seasons, often limited to weekends or holidays. This sporadic use undermines profitability and raises concerns about whether the current business models can sustain large-scale expansion.

Growth Drivers: Government Policies and Consumer Demand

The EV charging market has been propelled by three key drivers: government regulations, rising consumer demand and technological innovation.

The European Union’s Alternative Fuels Infrastructure Regulation (AFIR) has played a pivotal role by setting ambitious targets for the deployment of charging stations across key transport corridors. This regulation, combined with national and local government incentives, has created powerful momentum for growth. In the Netherlands, municipal grants and favourable zoning laws have spurred the installation of public chargers, while in Germany, government funding for high-speed charging infrastructure has accelerated the deployment of fast chargers along its autobahns.

On the consumer side, the rapid adoption of electric vehicles has been driven by a combination of environmental awareness, rising fuel costs and the decreasing affordability gap between EVs and traditional vehicles. As more consumers make the switch to electric vehicles, demand for reliable, widespread charging infrastructure becomes increasingly pressing. Corporate fleet electrification, particularly in logistics and service sectors, is also adding to the pressure for faster, more reliable charging networks. However, consumer expectations have placed considerable strain on infrastructure providers. Drivers now expect a fast-charging experience that mirrors the convenience and speed of traditional petrol stations, presenting significant capital and logistical challenges for operators.

Despite surging demand, consumer preferences are far from uniform. Urban users prioritise convenience and accessibility, while rural drivers focus more on the availability of charging stations along longer routes. This divergence adds another layer of complexity to deployment strategies, making it clear that a one-size-fits-all approach will not work for all markets.

Consumer Preferences and Market Demands

One of the most significant shifts in the EV charging market is the changing nature of consumer preferences. While home chargers remain the preferred option for many, there is growing demand for fast- or ultra-fast-charging stations, particularly along motorways and in urban centres. Fast-charging stations are crucial to address range anxiety and alleviate concerns about long journeys. However, building a network of high-speed chargers at scale is an expensive undertaking, one that requires careful planning and substantial investment.

A notable trend emerging within the consumer space is the increasing use of fast chargers, even though most drivers still charge their vehicles overnight at home. This preference for rapid recharging highlights the growing demand for infrastructure that can deliver on the promise of convenience and speed. Yet, as these charging stations are capital intensive, their roll-out is hampered by long payback periods and limited utilisation during off-peak times, raising questions about the sustainability of current business models.

Furthermore, the divergence between urban and rural consumer needs is a critical factor in determining the deployment of charging stations. Urban drivers are seeking high-density networks that provide quick and easy access to chargers in busy areas. In contrast, rural drivers need charging infrastructure that ensures long journeys are possible without the fear of running out of charge in underserved regions. The challenge for operators is balancing these different preferences while ensuring the profitability and viability of their investments.

Current energy infrastructure is often not equipped to support the widespread deployment of fast-charging stations, which will require substantial upgrades to the grid, as well as the integration of advanced energy management systems to handle increased demand and greater fluctuations. Furthermore, issues such as the lack of standardisation across different charging networks and the high upfront costs associated with deploying fast chargers are additional hurdles to profitability. Operators also face the challenge of low utilisation rates, which are exacerbated by the fact that charging stations are often only used at peak times, such as weekends or holidays. This fluctuating demand undermines the potential for sustained profitability and raises doubts about the viability of certain business models in the long term

Business Models: Fragmented and Complex

Business models in the EV charging market are diverse and continue to evolve. At one end of the spectrum are vertically integrated operators, like Tesla, which build proprietary charging networks for their own vehicles. At the other end are open-access providers, who focus on enabling interoperability across multiple networks, allowing consumers to charge their vehicles at a wide range of locations.

In addition to these models, many operators have pursued partnerships with retail outlets, hotels and real estate developers, aiming to install charging stations in high-traffic locations and generate additional revenue streams. Other business models focus on providing fleet-specific charging solutions for logistics companies or ride-hailing services. Subscription models, pay-per-use schemes and public–private partnerships are also common, adding to the market’s complexity.

However, despite the wide array of business models, profitability remains elusive for a large number of operators, with, again, high capital expenditure, unpredictable utilisation rates and long payback periods being to blame. Even large, well-established players are struggling to achieve consistent margins. A case in point is the Dutch market, where several EV charging companies have struggled financially or even gone bankrupt. These companies faced a combination of operational challenges, such as high upfront costs for infrastructure, fluctuating energy prices and competition-driven price wars. Additionally, reliance on public–private partnerships and government subsidies has left many companies vulnerable to shifts in policy and funding. For smaller operators, underutilised assets and slow market growth have further complicated efforts to become profitable.

Achieving profitability thus remains a major hurdle for many operators. The question is whether their current business models can evolve to meet their long-term profitability needs, or if the market will ultimately consolidate around a few vertically integrated players capable of absorbing the high costs and competition.

Key Players in the Market: Competition and Collaboration

The EV charging ecosystem is highly competitive, with a range of stakeholders vying for increasing market share. Dedicated charging companies like Fastned and Allego are rapidly expanding their networks across Europe, while automotive giants such as Volkswagen are heavily investing in charging infrastructure through ventures like IONITY. Energy companies like Shell and BP are also entering the space, leveraging their existing petrol station networks to deploy EV chargers.

But governments and public–private partnerships are also playing a crucial role in deploying charging infrastructure, particularly in underserved areas. While competition is fierce, collaboration is increasingly necessary to fill infrastructure gaps and address profitability concerns. Shared infrastructure agreements and roaming partnerships are helping to build network density, reduce duplication and improve consumer confidence. The question remains whether these collaborations can support long-term growth or whether the market will eventually consolidate around a few dominant players.

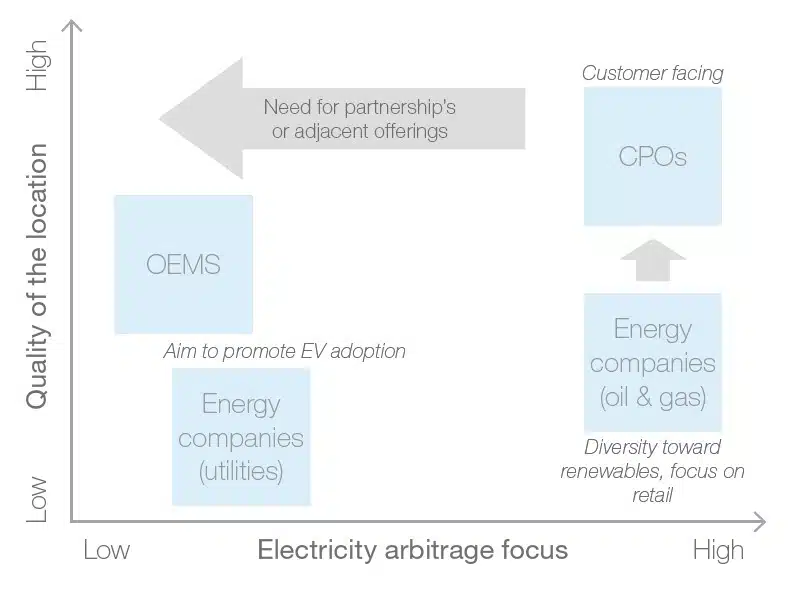

Figure 4 – Current pure-play CPO positioning against new market entrants

Source: McKinsey