Executive summary

Betting on India’s consumer‑goods arena is no longer an option; it is a strategic imperative. As developed markets plateau and global consumer confidence falters, India offers a rare combination of macro economic resilience, demographic tailwinds, and accelerating discretionary spending. Per capita GDP is projected to rise by 70% to $4,000 by 2030, pushing half of all households into middle or affluent tiers. Household consumption is expected to add $1.5 trillion in new spend.

Yet what makes India attractive also makes it complex. Rather than a linear expansion of traditional consumption, it is actually a bottom-up transformation driven by young, digitally native, experimental consumers, and powered by behavioural shifts: rising aspirations, convenience as a baseline expectation, and an appetite for new formats, brands, and channels. By 2030, 40% of consumer purchases will be digitally influenced; rural markets are already growing 1.5x faster than urban ones; and easier credit access is enabling a surge in first-time discretionary spenders.

Capturing this upside is now a question of precision, as opposed to a simple one of presence. Global brands face mounting pressure from agile Indian players who operate in compressed product cycles, build for fragmentation, and integrate digital channels for both fulfilment and feedback. Mamaearth’s short cycle and rapid SKU testing, Licious’s owned cold chain and boAt’s lean design cycles exemplify execution that keeps pace with consumers rather than calendars. Incumbents that rely on centralised structures, global product pipelines, and traditional retail formats risk being outpaced – not due to lack of insight but due to execution gaps.

What unites the outperformers is their ability to localise decisions, iterate rapidly, and meet the Indian consumer at their speed. Hindustan Unilever’s deep decentralisation, Celio’s tailored sizing, and Decathlon’s domestic sourcing model all demonstrate that structural adaptability is what builds long-term relevance, more so than just brand equity.

India is setting its own path in this, writing a new playbook as it goes. For international players, this market is not just a growth opportunity; it is a stress test for agility, proximity, and consumer fluency.

India’s consumer goods market: a growth curve too strategic to ignore

As developed markets plateau and consumer confidence falters, India stands out as a vibrant outlier. But entering this market requires more than optimism: it demands precision and a carefully calibrated strategy. India’s consumer landscape is fragmented across geographies, income levels, languages, and cultural preferences. Succeeding here calls for a deep understanding of local markets and robust go-to-market plans that reflect regional patterns and retail dynamics. An agile and dynamic approach is essential to continuously test, learn, and adapt. There is a significant upside for multinational corporations that enter India with full commitment, are willing to take some risks, and do their homework properly.

Section 1: How is India’s economic and demographic momentum reshaping the consumer landscape?

India’s consumer market is undergoing a structural transformation, one that combines strong demographic fundamentals with a unique blend of macroeconomic, political, and social drivers. While many emerging markets have experienced periods of fast growth, India’s trajectory is distinct in its scale, depth, and durability.

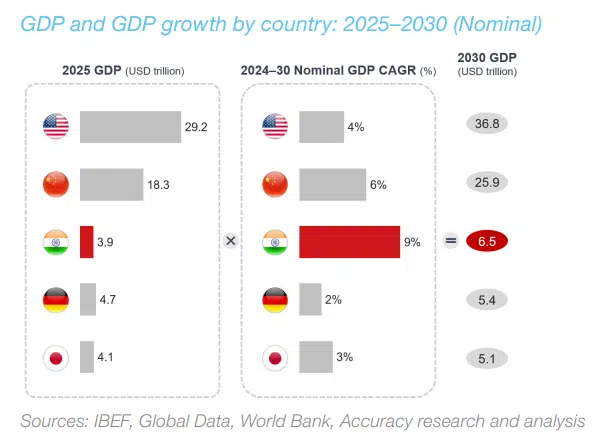

A fast-growing economy with staying power: India is the world’s fastest-growing large economy and will be the third largest by 2027. Between 2024 and 2029, GDP is set to grow from $4.0 trillion to $6.5 trillion reflecting a real growth rate of about 5–6%. This overarching economic rise is not only lifting GDP but is also fuelling widespread consumer optimism, creating fertile ground for consumption-led growth.

Strong supply-side fundamentals: What sets India apart is significant supply-side momentum due to strong policy support (e.g. production-linked incentives), shifting global supply chains, and a culture of entrepreneurship. Manufacturing, political stability, and infrastructure upgrades are creating jobs, boosting incomes, and expanding household participation in the consumption economy.

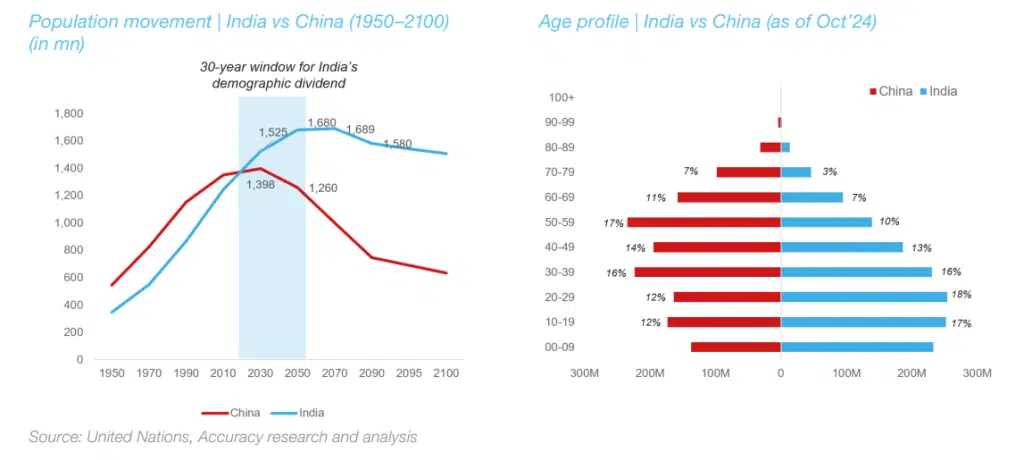

- A demographic dividend that goes beyond size: India’s population – currently at 1.4 billion and projected to stabilise at 1.6 billion – is not only large but structurally young. With a median age of around 29 years, India is over a decade younger than China. More than 40% of the population is under 25, creating an enormous base of first-time earners and aspirational consumers. But this demographic dividend is no longer just about scale; it’s about changing consumer profiles. Today’s young Indians are digitally native, brand-conscious, and value-driven. Their consumption habits are shaped by social media, global exposure, and a strong desire for self-expression.

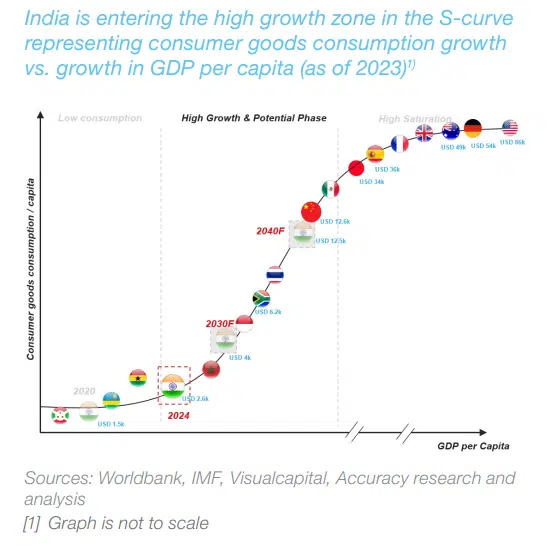

Rising incomes, rising expectations: This youth-driven momentum is amplified by rapid gains in per capita income. With GDP rising and population growth stabilising, India’s per capita income is forecast to jump from $2,450 in 2023 to $4,000 by 2030 (i.e. a 70% increase). This shift is reshaping the income pyramid. By 2030, half of all households will belong to middle income and higher segments, compared with just a quarter today. The number of high-income households (those with household income of more than ~ $35,000) is projected to soar from 1 million in 2005 to 50 million by 2030, considerably expanding the pool of premium consumers.

Section 2: Where is consumption growth most concentrated today?

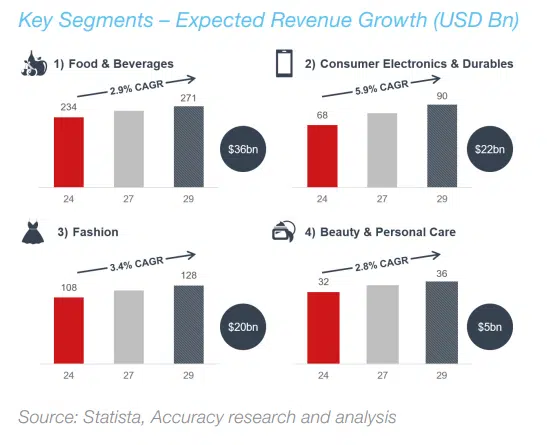

India’s consumption boom spans multiple sectors and is projected to grow from $525 billion in 2025 to $625 billion in 2030. However, this market is also becoming more complex, segmented, and dynamic. Growth is broad yet uneven, with the biggest shifts occurring where rising aspirations, digital access, and changing price-value perceptions meet.

The consumer electronics and durables sector is forecast to grow from $68 billion to $90 billion by 2029, driven by first-time buyers and upgrades across incomes. Affordability and financing are boosting demand for smartphones and smart TVs in semi-urban and rural areas. Domestic manufacturing, aided by government support, is making the segment more competitive. Consumers prefer durable, affordable products with smart features, building loyalty before upgrading. Brands balancing aspiration, practicality, and physical and digital reach will best capture this growth.

Food and beverages, already the largest segment at $234 billion in 2024, is set to reach $271 billion by 2029. While staples remain core, rising incomes and digital access are fuelling demand for artisanal, organic, and health-focused choices. Younger households are drawn to global flavours, clean labels, and premium packaging, helped by modern trade and quick commerce. Yet trust, value, and local relevance still anchor decisions. Success here requires brands to balance price sensitivity with quality and to scale with India’s layered food culture.

Fashion is projected to grow from $108 billion to $128 billion by 2029, driven by young, fashion-aware consumers engaging with global and local brands. Interest in athleisure and Western styles is rising, but fashion remains rooted in function, affordability, and culture. Tier 2 and tier 3 city consumers value durability and fit, alongside trends. Global brands have adapted sizing and pricing to compete. Success hinges on balancing aspiration with pragmatism, styling with accessibility, and scale with local nuance.

The beauty and personal care segment, growing from $32 billion to $36 billion by 2029, is driven by young urban consumers favouring digital-first, natural, and Ayurveda-inspired brands, prioritising transparency over legacy. Many consumers are still exploring routines and price points, with seasoned buyers preferring minimalist, heritage products, while newcomers seek bold packaging and influencer trends. Success requires brands to go beyond visibility –educating, contextualising, and growing with consumers by balancing confidence with curiosity.

Together, these trends point to a distinctive pattern: while consumer growth in India is strong across categories, the underlying drivers vary significantly due to diverse consumer motivations and behaviors. Each category is evolving in its own way – shaped by a mix of cultural, geographic, income-based, and urban–rural dynamics. This complexity means that new entrants risk oversimplifying the market at their own peril, while established brands relying on legacy strategies may be outpaced by those more attuned to India’s dynamic and highly segmented landscape.

Section 3: What makes the Indian consumer market uniquely challenging – and uniquely rewarding?

India’s consumer evolution doesn’t follow the linear playbook seen in past emerging markets. What is unfolding is structurally distinct, driven by young, digital-first consumers and accelerated by local innovation, not just macro expansion. What makes this market stand out is the scale of the opportunity and, perhaps even more so, the complexity of capturing it.

A new set of growth engines

- Premiumisation across price points: Consumers across income levels are moving from basic utility to aspirational quality. Even price-sensitive categories see rising demand for value-added features, natural ingredients, and better design. As upper-middle and high-income segments grow, so does premium interest among the middle class, with “affordable luxury” becoming a key focus.

- Convenience as a consumption driver: Quick commerce is redefining value to include speed, accessibility, and instant gratification. For young urban consumers, convenience is now a baseline expectation. Digital-native brands capitalise on this but face rising cost and inventory challenges to sustain the “10-minute delivery” promise.

- High digital literacy and influence: With over 600 million smartphone users and a leading digital payment ecosystem, Indian consumers are among the most digitally influenced globally. By 2030, nearly 40% of all purchases will be digitally shaped, either through discovery, comparison, or purchase — meaning brands must be present and relevant across multiple touchpoints.

- A rural engine gaining momentum: Rural and semi-urban markets are now growing 5x faster than urban ones, fuelled by post-COVID economic recovery, digital access, and improved infrastructure. Rural growth is expanding to include packaged foods, beauty products, and even electronics, often driven by mobile-first engagement.

- Consumer confidence and willingness to experiment: Compared to Asia-Pacific peers, Indian consumers are more optimistic, open to try new brands, and receptive to marketing innovation. This enables faster testing and less resistance to new formats, demands higher standards for relevance, brand storytelling, and trust-building.

- Easy access to credit: Digital lending, buy-now-pay-later (BNPL) platforms, and improved financial inclusion are driving wider consumption participation. Household credit demand in India has grown at a 6% CAGR over 10 years, with consumer financing becoming key for spending — especially for first-time premium buyers.

A market that doesn’t scale linearly

The very factors that make India attractive also create operational and strategic hurdles:

- Youthful, fast-moving consumer base: Brand loyalty is volatile. Trends can shift quickly, and companies must stay close to consumers and continuously test and iterate — especially in categories like fashion, beauty, and food.

- No single India: India is a mosaic of micro-markets with varied tastes and price sensitivities. Success of a product in one city rarely predicts the same in another, requiring localisation across product, pricing, and go-to-market strategies.

- Intense competition from all sides: Local startups move fast and undercut, regional players hold strong loyalty, and Korean and Chinese brands gain traction with aspirational, affordable design—especially in electronics, cosmetics, and fashion.

- Supply chain fragmentation: India’s vast geography challenges logistics and fulfilment. Quick commerce amplifies this, needing hyperlocal inventory, last-mile innovation, and seamless channel orchestration. Traditional retail also remains fragmented.

What truly sets this growth apart is its structure. Unlike past industrialising economies with centralised, manufacturing-led growth, India’s surge is fragmented and digitally driven — powered by a rising semi-urban middle class, digitally native youth, and growing rural buying power alongside rapid smartphone adoption. India’s growth is also bottom-up, driven not just by macroeconomic expansion but by shifting behaviours — demand for convenience, aspirational buying, quick commerce adoption, and openness to experimentation. Unlike past markets led by global brands, India faces pressure from agile local startups and consumers seeking both value and variety. Consumption here evolves in real time, shaped by technology, financial inclusion, and cultural fluidity.

Section 4: India is not repeating a previous playbook — it is writing a new one.

While the fundamentals may be familiar, the patterns of consumption in India unfolding today suggest a different type of opportunity, and a different set of strategic requirements.

Meeting expectations in India’s fragmented, margin-sensitive, and logistically complex market—especially in perishables—is challenging. Rural markets are growing faster and differently, yet many foreign brands rely on metro-centric distribution, raising costs in high-growth areas. Local players succeed by building operational elasticity — shorter lead times, tighter inventory, and adaptable last-mile delivery. Decisions are made closer to customers, free from global hierarchies. For Western incumbents, the barrier isn’t insight but execution. In a market where speed, availability, and channel fluency matter, this execution gap quickly becomes a competitive risk.

How are local and new-age players outpacing established brands?

The companies best positioned for India’s shifting market are not the biggest ones, but the most structurally responsive. New Indian brands are built for fragmentation, speed, and consumer proximity. They launch and refine products fast, using digital channels for both sales and feedback, and tightly link supply chains with marketing to match demand in real time. Mamaearth hit $230 million in revenues with a five-year CAGR of 154% through rapid SKU testing, influencer marketing, and a D2C-first strategy; Licious scaled to $82 million (93% CAGR) by owning its cold chain and delivery; and boAt reached $374 million thanks to its lean, high-turnover cycles and localised design, pricing, and bundling.

These brands show an ability to operate in short loops: listening, testing, fulfilling, and relaunching at the pace of the consumer, rather than the calendar. With over half of India now digitally active, behaviours shift in real time. Global incumbents, slowed by rigid pipelines, struggle to match this speed. And in a fluid market, adaptability beats legacy.

Entry gets you in. Execution keeps you there.

As India’s consumer market matures, the gap between presence and true effectiveness widens. India rewards precision, aligning operations with fast-changing, local expectations for product, value, and access. This often shows up in details that global structures overlook. Celio resized clothes for Indian body types; cheese and wine brands reworked packaging and portion sizes; toothpaste manufacturers added salt to follow Ayurvedic recommendations. These represent structural shifts.

But the product alone doesn’t set winners apart; decision-making does. Hindustan Unilever thrives not because of its size but because of its deep local autonomy built through decades of decentralised execution and frontline trust. How companies enter a market also matters less than how adaptable they stay: Starbucks’s JV with Tata and Decathlon’s pivot to local sourcing are clear examples. By contrast, rigid, global playbooks often fail. Take, for example, Nike stumbling in the implementation of its standardised model, where Adidas adapted with local pricing and targeted sponsorships.

In a market where loyalty is fluid and value chains are still forming, slow or shallow adaptation carries steep costs. Those who do not build true relevance risk being present in name only, as faster local players lead India’s next growth wave.

By Anuj Rikhye, Xavier Chevreux and Jean-François Partiot, Partners, Accuracy.

With contributions from Felicitas von Anhalt, Dhruv Bhardwaj and Subhanshi Srivastava, Managers, Accuracy.