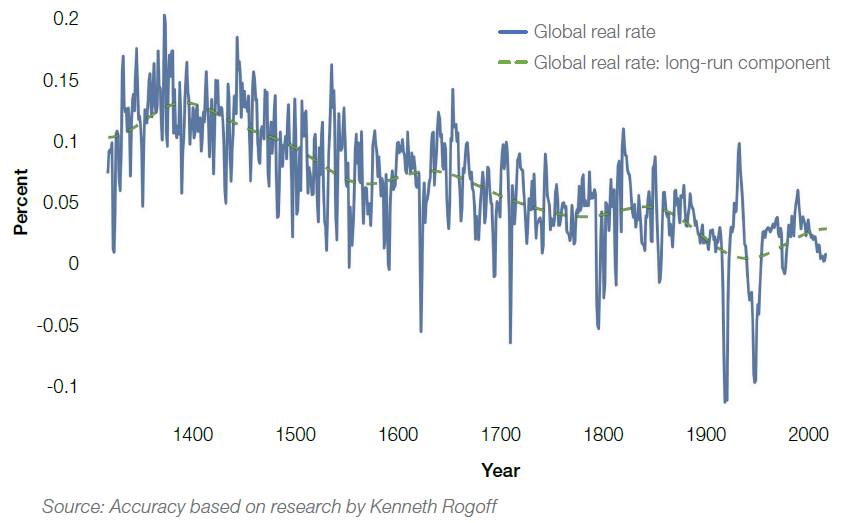

A new study on long-term interest rates has identified what appears to be a downward structural trend – one lasting centuries! This runs counter to received wisdom on the matter, challenging our preconceived notions. But it is not just the past that is of interest here. In recent years, the global economy has faced a number of obstacles that have complicated the work of economists in forecasting its future trajectory. Brexit, Covid-19, the war in Ukraine – the list goes on. And it includes Biden’s new protectionist policies against China. Let’s look into each of these matters in turn to see what we find.

Headline global real rates

A study performed by Kenneth Rogoff, a leading US economist, came to an interesting conclusion. His paper, titled ‘Long-Run Trends in Long-Maturity Real Rates’, found that long-term interest rates had been on a general downward trend since the Renaissance, demonstrating that this trend is no recent phenomenon but, in fact, has been a feature of the global economy for centuries! This observation calls into question traditional explanations attributing the downward trend to recent economic dynamics, such as stagnation or demographic change. On the contrary, the study found that these elements appeared to have little bearing on the overall movement; what is more, any periods of upward movement were relatively short, returning to the downward trend within more or less one to three years. So, what is causing this pattern? The study suggests that other factors, such as bond market liquidity and global time preferences, may be playing a much more significant role.

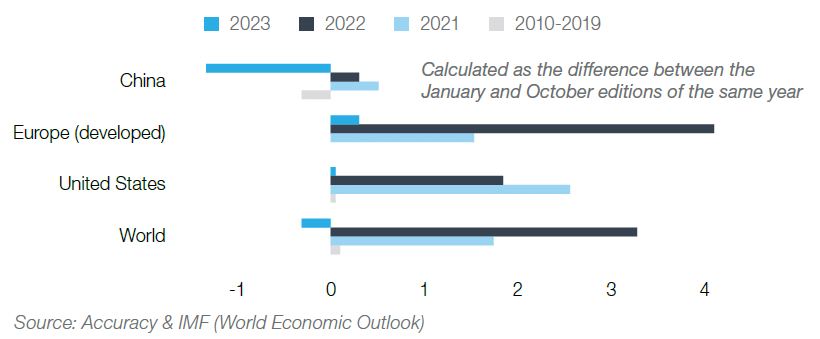

Inflation forecasting errors of the IMF in past years

Enough of the past, let’s move on to the future and forecasting, in particular. This art has come under greater scrutiny in recent years, as events like the Covid pandemic and the Russian invasion of Ukraine, with the subsequent spike in energy prices and general rise in inflation, wreak havoc on economists’ forecasting models. Indeed, for short-term forecasts, economists tend to rely heavily on cyclical dynamics; however, the recent events mentioned above, among others, have had a considerable disruptive impact on the economic cycle, culminating in far less accurate forecasts overall (see chart). Are such cataclysmic events behind us? What about their lingering consequences? That remains up for debate. What is important to remember is not to think as if we have a deterministic future or one already determined and laid out ahead; the situation is undoubtedly more complex than that.

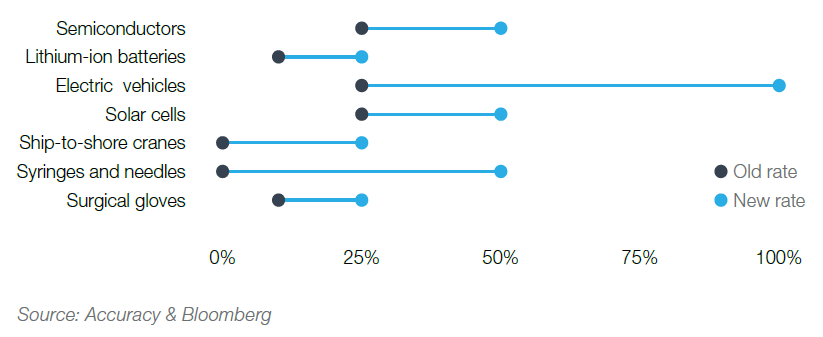

Increase in duties on Chinese imports by President Biden

Finally, let’s touch on international trade, and on President Biden’s new protectionist policies vis-à-vis China. These policies, taken from the playbook of former President Trump, albeit in a much smaller package (only $18bn of Chinese imports concerned vs $350bn), come in support of the president’s plan to reindustrialise the country, particularly in certain swing states (those that switch between Democrat and Republican). Three points are worth mentioning here. First, the approach goes against traditional economic doctrine by reducing competitive forces and thus, in the long run, harming the USA’s competitive edge. Second, by increasing duties on certain goods, it undermines some of the fundamentals of Bidenomics, namely the fight against inflation and the transition to greener energy (in light of the goods targeted). Third, it places Europe in a sticky situation: the USA will more than likely put pressure on Europe to apply similar measures on China, but Europe is loath to hobble itself economically, particularly at this time of anaemic growth for the region. Biden is clearly prioritising US consumers over the traditional operations of the market; it is almost as if there is an election around the corner…