In this closing edition of the Economic Brief, we examine the IMF’s latest World Economic Outlook and the reasons for declining medium-term growth. We then head to Germany to cover its political turmoil before crossing the Rhine to understand the collapse of the French government. Let’s get stuck in.

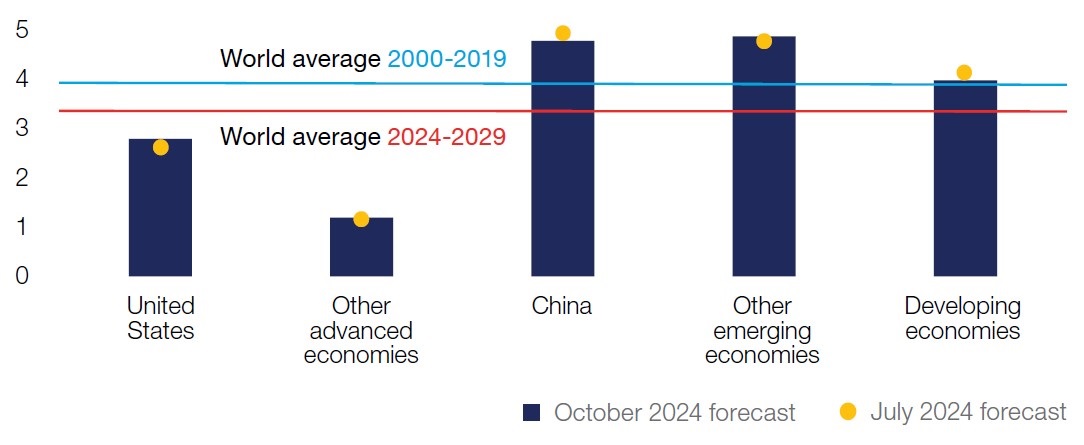

The IMF recently released its latest World Economic Outlook. One of its critical findings bears repeating here: whilst global economic growth appears stable in the short term, it is slowing down in the medium term. Indeed, compared with the period 2000–2019, where average global growth was c. 4%, forecast growth for the period 2024–2029 stands 0.5 points lower, a not inconsiderable amount at the global level.

Economic growth: stable in the short term, weaker in the medium term

Sources: Accuracy, IMF

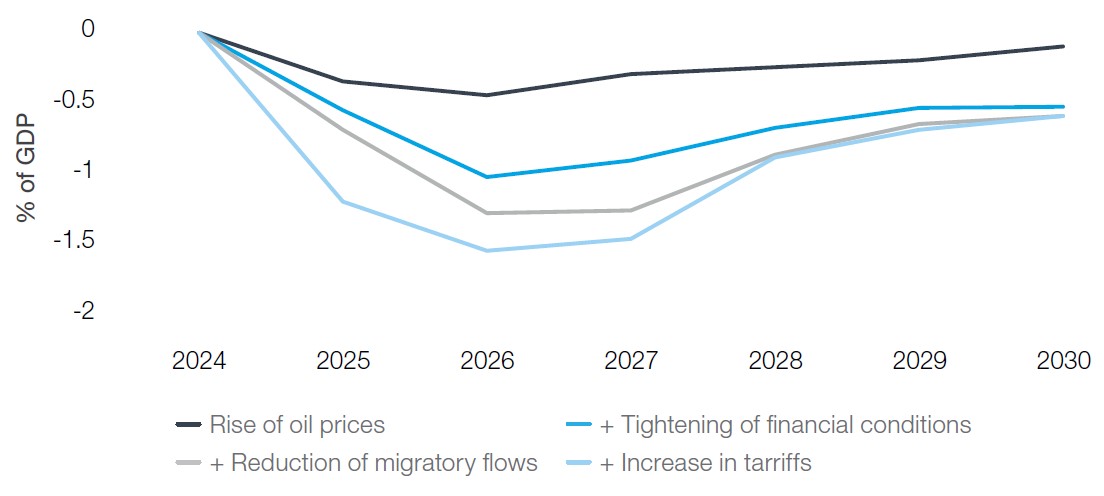

There are multiple reasons for this bleaker outlook, with a slowdown that may start soon, notably connected with various areas of uncertainty: possible rises in oil prices; potentially tighter financial conditions, whether in terms of credit availability or capital market dynamics; greater restrictions on migratory flows; increases in tariffs. Note, two of these points come directly from the Trump playbook. The IMF estimates that these factors taken together could have a 1.5-point impact on global economic growth in 2026.

Measuring mains risks to global growth

Sources: Accuracy, IMF

Let’s turn to Germany. The largest economy in Europe is undergoing a period of political turmoil as Olaf Scholz lost his majority in the Bundestag. Indeed, preparation of the 2025 budget highlighted certain unsustainable contradictions for his ruling coalition. Whilst policies in favour of Ukraine and rearmament appeared to be the subject of consensus, others were less so. The SPD sought to maintain a decent level of social protection. The Greens wanted to pursue their policies against climate change. And the FDP were looking to keep in place a certain degree of budgetary rigor. Unfortunately for Scholz, against the backdrop of the country’s stuttering economic growth, these objectives proved incompatible. The parties could find no compromise, the FDP withdrew from the coalition and Scholz lost a vote of no confidence. Germans will head to the polls on 23 February to elect a new Bundestag in a bid to resolve the deadlock.

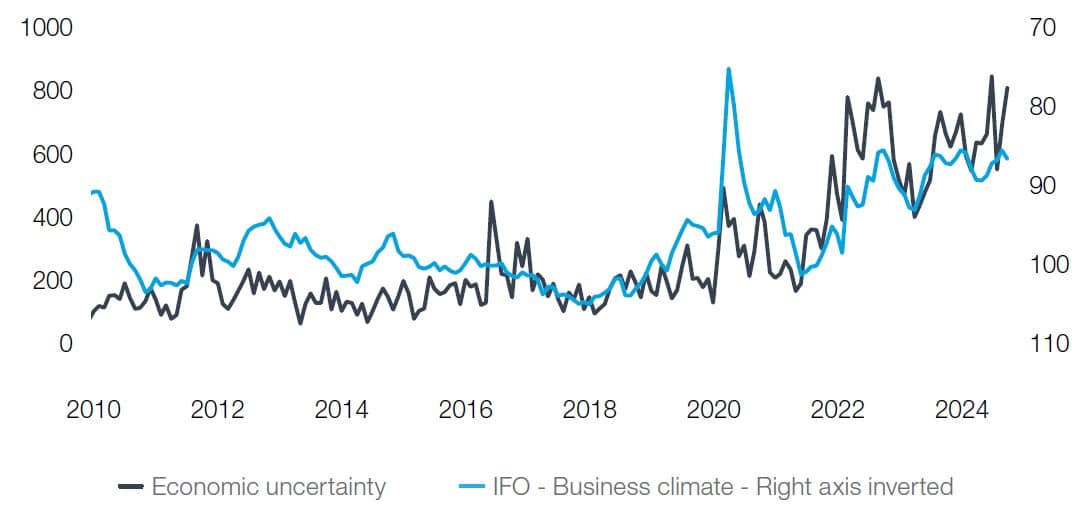

Germany: rising economic uncertainty and falling business confidence

Sources: Accuracy, Macrobond

This quagmire is reflected in the country’s growing economic uncertainty and diminishing business confidence. Four economic ills plague the country: the rise of economic nationalism in parallel with the fragmentation of the global economy; the change in the status of China, from customer to competitor to indispensable supplier; the increase in the cost of energy, a major consideration for a country with such a significant manufacturing base; and cumulative gaps in domestic investment and structural reforms. A turning point must come if the country is to dig itself out of its hole.

Crossing the border to France, we find a country also in something of a predicament. Like its neighbour, it is struggling to get its budget approved for 2025. The executive and the legislative are at loggerheads over the budgets for the State and social protection, to such an extent that the previous government under Barnier has collapsed. The National Assembly is fractured, with no clear majority, and coming to a compromise appears beyond the capabilities of all involved. It would not be unreasonable to question whether France will get a 2025 budget sorted at all! In the meantime, the 2024 budget will roll over on a monthly basis until a new one is voted…

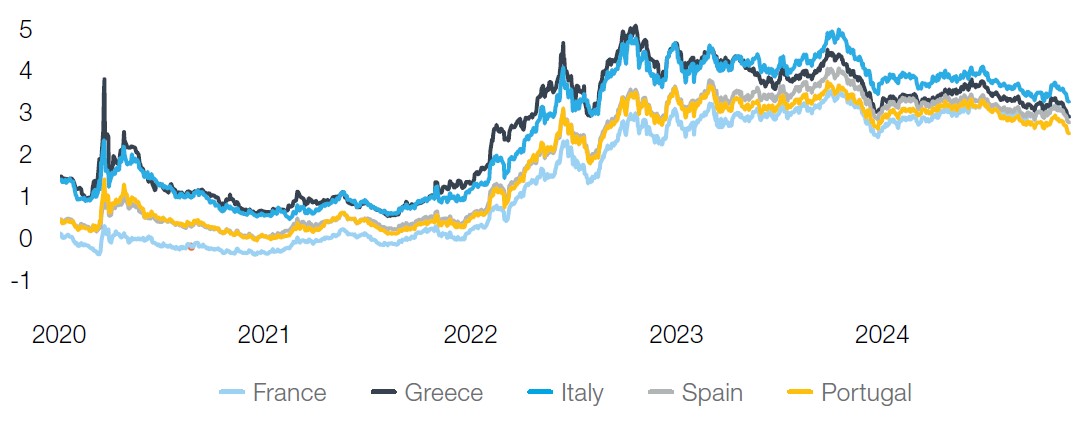

The financial markets are watching this situation closely. France’s long-term government bonds have lost some of their lustre, and yields are now equivalent to those of the former problem children (at least in economic terms) of the European Union: Greece, Italy, Spain and Portugal. But the French are far from alone in this; many countries need to be wary of finding the right balance between public deficits and long-term interest rates…

French long yields now lost in the Mediterranean melting pot

Sources: Accuracy, Macrobond