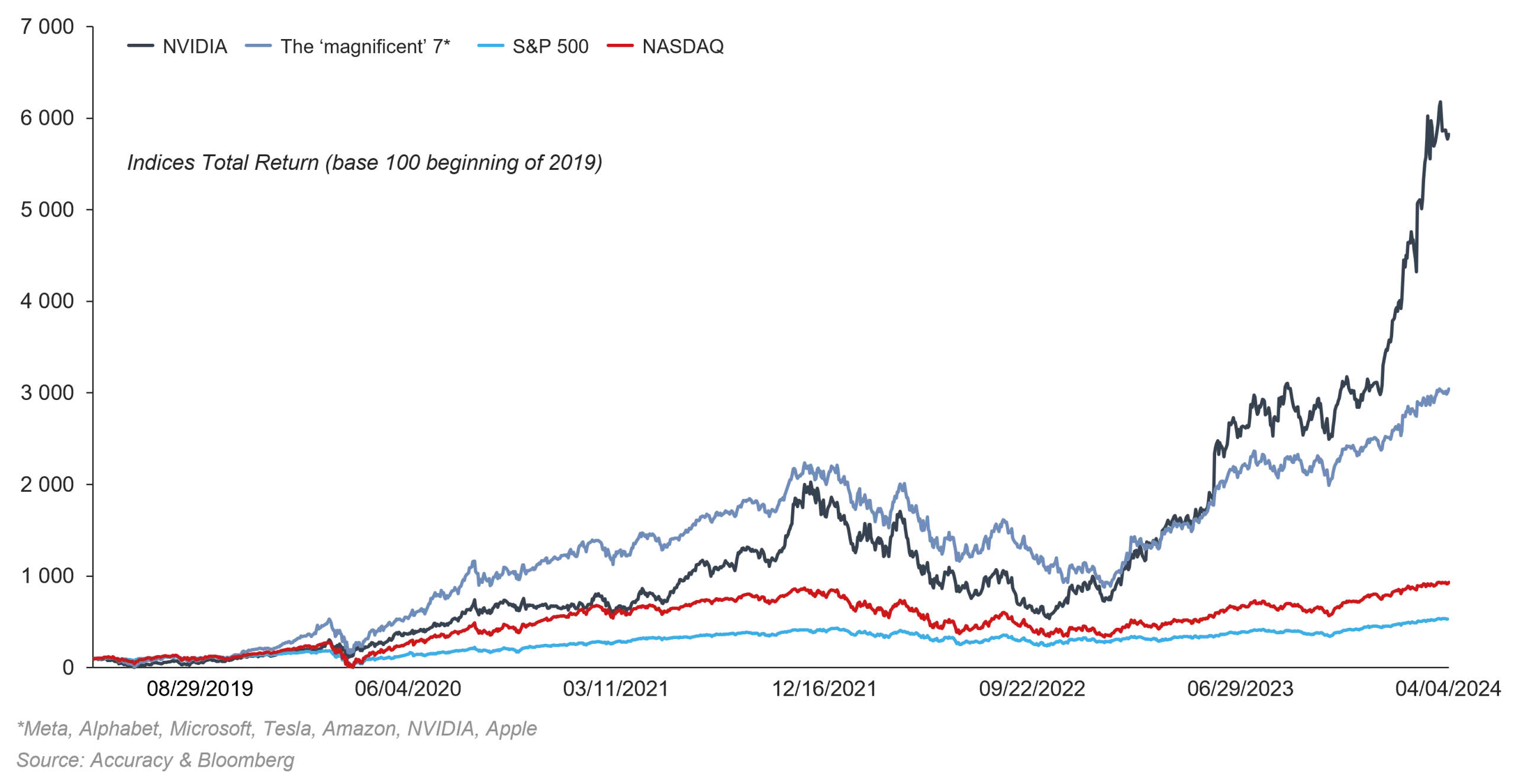

Generative artificial intelligence (GAI)[1] is attracting a lot of attention. There’s no shortage of evidence of this enthusiasm. According to a survey carried out by S&P Global Market Intelligence among a sample of 728 companies, 49% really intend to invest in GAI, 28% are looking closely at the issue and 23% are unsure. Factset, a financial data management company, tells us that 179 of the 500 companies that make up the S&P 500 stock market index (36%) mentioned artificial intelligence (AI) when presenting their results for the fourth quarter of 2023. This compares with a five-year average of 73. The percentage is even higher in the tech sector (over 80%). The (absolute) number of references to AI was around 70 for the ‘champions’ Meta, Microsoft and Alphabet and over 100 for NVIDIA, the star of the market. Individuals are not to be outdone in this matter. According to figures provided by the independent Canadian economic research company BCA, ChatGPT, one of the pioneers of GAI, passed the threshold of 100 million users in two months. By comparison, it took Facebook five years and TikTok one year to reach this level. Savers and investors are sensitive to the development of this technology. In the American case, the stock market performance of the relevant shares is all the more impressive as the chosen business model includes significant development in GAI.

Why this interest? For individuals, it is no doubt out of curiosity and also as an aid in content production. For companies, the ambition is obvious and it is twofold: to use a technology that is financially affordable and that will improve the efficiency of the value creation process. For investors, it is a question of betting now on a stock market story that should be a winner.

Let’s take a closer look at three aspects of GAI: the cost of the necessary investments, its macroeconomic impact and its valuation by the financial markets.

Let’s start with the costs. They can be grouped into three main categories: IT infrastructure, model training and the use of trained models. Two dynamics are emerging. First, costs look to be proportionate to the size of the models; second, a marked downward trend in costs is expected. According to BCA, infrastructure and training costs could fall by 75% by 2030. Use costs could fall even faster. Each company wishing to use GAI must then determine the best approach to do so: what size of model and how to obtain it (developing it in-house or sourcing it externally). It is worth noting that mastering the model will be a constraint for most of them. The dual solution of one or more smaller models produced from open-source code should be the dominant one, as it is more economical. All this points to the conclusion that many companies will embark on the GAI adventure, provided, of course, that this perspective on cost trends is borne out.

What will be the impact on the economy? A positive one, of course, and a considerable one at that, if we believe the opinion-makers that are the major investment banks and international strategy consultancies. Goldman Sachs is betting on an increase in world GDP of USD 7 trillion over the next 10 years (with a level of around USD 100 trillion in 2023), while McKinsey shows a little less optimism, with a range of between USD 2.6 trillion and USD 4.4 trillion.

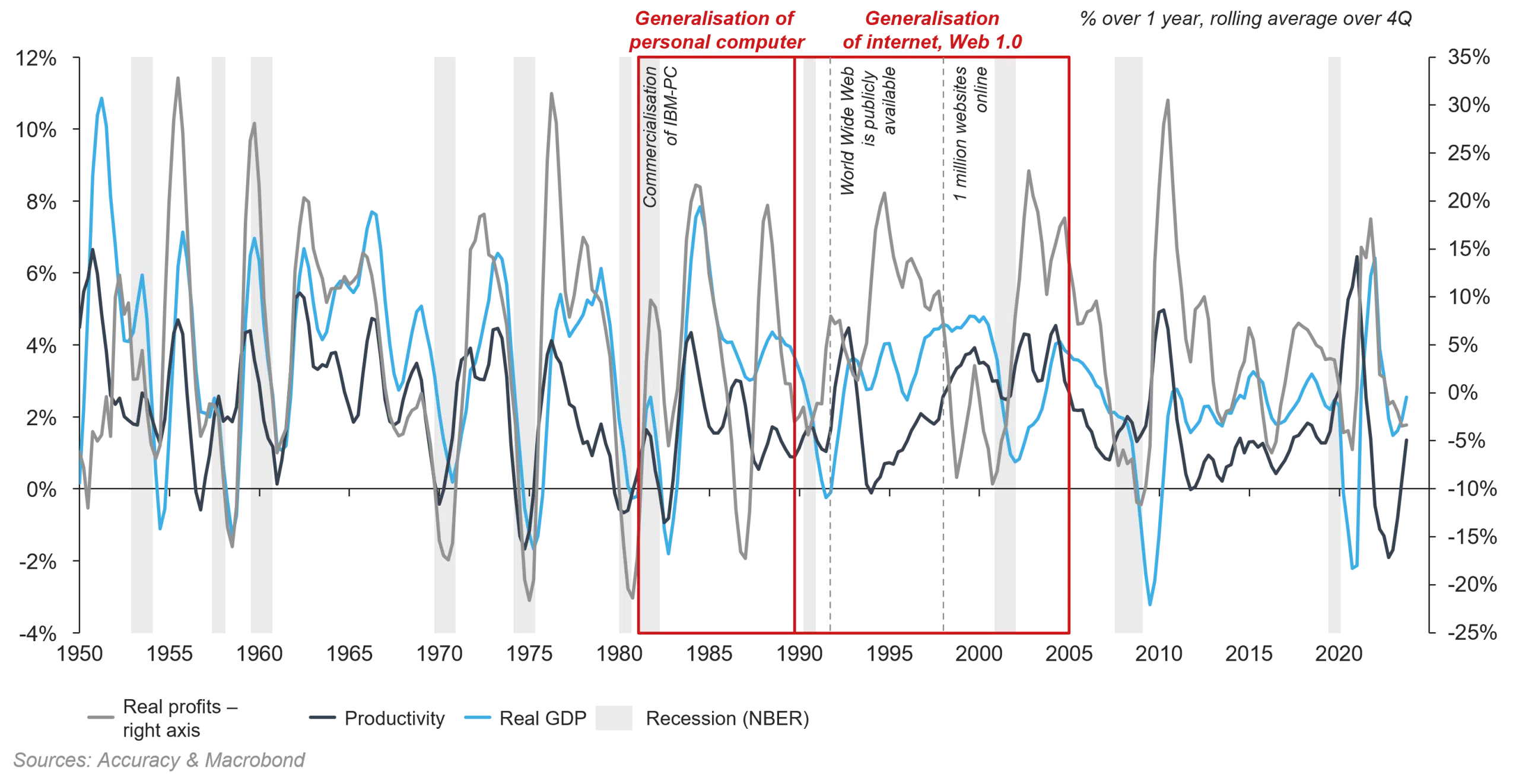

Two comments come to mind. First, academic literature concludes that the economic impact of the generalisation of GAI is uncertain, in terms of productivity, employment and therefore growth. There is a lack of data and also a lack of information on the economic policy support that should be put in place. Second, it is possible to look back in history and recall the productivity gains generated by the changes in tech. Let’s look at the American case and draw a picture of productivity trends in the United States since the end of the Second World War. The widespread introduction of personal computers (in the 1980s) and the internet (in the following decade) led to a surge in productivity. This growth was not particularly spectacular: if we exclude periods of recession, it stands at +1.8% per year between 1975 and 1979; +2.1% between 1981 and 1988 (spread of the personal computer); +2.4% between 1989 and 2005 (spread of the internet); +1.5% thereafter (between 2006 and 2023). Given this hindsight, we are inclined to envisage a rather modest increase in productivity, and not over a very long period. Without commenting on the impact of GAI on employment, might we be inclined to find that the Goldman Sachs and McKinsey assumptions are perhaps over-optimistic?

This two-pronged approach, even if only provisional, prompts us to reconsider the attitude of the capital markets towards GAI. If implementation and operating costs fall as envisaged, and if productivity and growth results are truly high, the translation of such expectations into share performance can be understood. But what if this optimism is dashed? The reasons for such disappointment are easy to imagine: as well as a failure to confirm the assumptions, we might imagine soaring energy costs, onerous copyrights or a destabilisation of the labour market that economic policy initiatives struggle to correct. All of this is to say that the capital markets appear to have adopted a rose-tinted scenario. Is this to the point of exaggeration?

And then there is the question of the organisation of the GAI market. It is now dominated by some of the biggest players in the tech industry. Is this situation sustainable? If not (due to action by the regulator or the emergence of new competitors), what impact will this have on earning prospects and capitalisation multiples?

[1] According to BPIfrance, GAI is an artificial intelligence capable of generating images, videos and even music. This category of AI is based on the use of machine learning models. Let’s look at the definition of AI, as proposed by France Stratégie: a set of technologies designed to use computers to perform cognitive tasks traditionally carried out by humans. The availability and quality of data, as well as the training of the system, are the necessary conditions for the smooth operation of GAI.

Hervé Goulletquer – Senior economic adviser, Accuracy

Accuracy Talks Straight #10 – Economic point of view