With numerous recent crises of global scale, governments have had to act decisively to protect their own economies and populations. This has inevitably meant turning to debt to find the cash necessary to implement protective measures. But what are the consequences? And should there be a limit? As for global trade, it grew strongly in 2022; however, this belies the structural changes that have been taking place. In this edition of the Economic Brief, we will delve into these topics, notably focussing on public debt levels for the major eurozone economies and recent developments in global trade, in particular with regard to China.

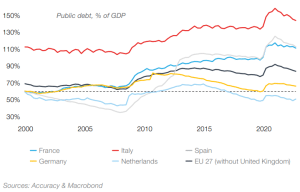

Eurozone: debt has still not returned to pre-pandemic levels despite a recent decrease

The level of public debt in Europe has risen significantly over the past few years. The graph opposite shows the level of public debt as a percentage of GDP for the major economies of the eurozone. We can observe that this metric rose in 2008–2009 systematically as each country came to grips with the Great Recession. It rose again across the board in 2020, with the onset of the Covid-19 pandemic. Indeed, many governments were doubly hit at this time: they took on debt to finance their public health services and their protective measures (e.g. furlough schemes and lockdowns), the very same measures that were partially responsible for shrinking their GDPs.

The subsequent fall in debt as a percentage of GDP was fostered by strong economic growth thanks to the post-pandemic recovery in 2021 and by inflation in 2022; however, levels remain high. Now, many governments are looking to reduce their debts, an issue becoming all the more pressing with the substantial rise in interest rates soon to be felt as governments renew their bonds.

Achieving this reduction will be no easy feat. Many priority areas for governments require increased public investment: the Russo-Ukrainian war has highlighted the need for European countries to increase their defence budgets to reach 2% of GDP, the target set by NATO, something managed by only three countries at present; the European Commission’s objective of a 55% reduction in greenhouse gas emissions by 2030 requires investment totalling a further 2% of GDP annually; and the digital revolution requires approximately 0.9% of GDP in annual investment. In light of all this and the EU’s Stability and Growth Pact (the rules that essentially prevent countries in the EU from overspending) coming into force again in 2024 after a pause during the pandemic, the Union finds itself in the midst of vital discussions to change the mechanism.

When it comes to global trade, activity was robust in 2022, having grown by 5% over the year despite the war in Ukraine, geopolitical tensions, inflation on raw materials and the appreciation of the dollar. This growth was driven largely by the lubrication of supply chains, linked to the end of Covid-19 restrictions notably in Asia. Notwithstanding, it is worth mentioning that the end of 2022 was affected considerably by the tightening of monetary policy, which weakened industrial production.

USA: the materialisation of “de-risking” with China?

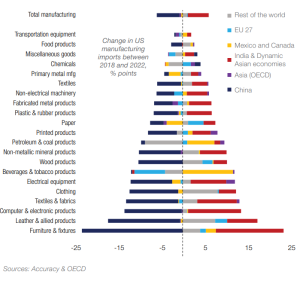

It is interesting to note that the structure of global trade has changed significantly in recent years, particularly in relation to China. For example, US manufacturing imports from China fell 25% in 2018, the year in which it applied customs barriers. This fall was compensated by increases in imports from other Asian countries, as shown in the graph opposite. We can also observe that the US is still far from nearshoring; the share of imports from Mexico and Canada remains relatively stable.

China does not come out of the situation so badly, however, with the EU compensating its fall in activity with the US. Indeed, manufacturing imports from China represented 33% of the total for the EU in 2022, compared with 26% in 2018. This rise appears to come to the detriment of imports from 25 other European countries (outside the EU) and from North America.

But where does this leave global trade tomorrow and the day after? For the US, at least, two options prevail: the first is a new cold war with China, with each party trying to contain the other rather than working together as competitors or even partners; the second is the renewal of a spirit of cooperation à la Bretton Woods. Might there be room to consider a comfortable middle ground between these polar opposites?