India’s auto-component industry has reached a structural inflection point. What began as a cost-efficient manufacturing base has evolved into a globally relevant industrial ecosystem, employing ~1.5 million people and supported by USD 15 billion in planned capital expenditure through 2030. With a deep supplier base and steadily improving engineering capabilities, Indian manufacturers now operate at a level that allows them to engage meaningfully in global automotive value chains.

While the domestic market continues to grow, it remains structurally smaller and less value-intensive than international markets. Outside India, the opportunity set is 7–8 times larger, with higher component content per vehicle, stronger pricing dynamics (typically +10–20%), and faster adoption of advanced technologies. As a result, companies that remain primarily focused on the domestic market are likely to face limitations over time in terms of scale and margin expansion, as well as in exposure to technological developments.

Among the available markets, L'Europe offers a particularly relevant entry point. Its auto-component market is estimated at USD ~200 billion, and its high concentration of OEMs and significant R&D intensity (~30% of automotive spend) mean the region provides both scale and technological depth. At the same time, it is undergoing a period of adjustment. Supplier profitability has declined by around 250 basis points, supply chains are being restructured toward greater localization, and a growing number of assets are becoming available at 30–50% of replacement cost. These dynamics are creating conditions that can facilitate market entry for well-positioned players.

Indian suppliers bring a combination of cost efficiency and operational flexibility. Those factors, together with their increasing technical capability, align well with Europe’s evolving requirements. Capturing this opportunity, however, depends on how companies choose to enter and operate in these markets. Approaches centered solely on exports are often insufficient to secure long-term positions. In a supply chain that is being actively reshaped, positioning early and with discipline is likely to determine which companies secure a lasting role in global automotive ecosystems.

India’s Auto-Component Industry is positioned for global growth

India’s auto-component sector has moved beyond its historical role as a cost-efficient supplier to domestic OEMs. It now combines scale, industrial depth, and operational discipline in a way that makes international expansion inevitable.

This shift is underpinned by three structural strengths.

1. A multi-layered and robust ecosystem

While the industry remains highly fragmented with ~80% of players being SMEs, a growing group of export-oriented firms already generating ~15–20% of industry revenues internationally, has developed the scale, technical capabilities, and operational maturity to compete globally. India offers a deep supplier base spanning traditional processes such as casting and forging to more advanced systems including electrical and emission components. This diversity allows suppliers to operate across multiple tiers of the value chain, combining cost efficiency and manufacturing breadth. Companies such as Bharat Forge (forging and powertrain systems) and Samvardhana Motherson (global Tier-1 supplier) illustrate this shift, combining cost advantages with increasing global integration.

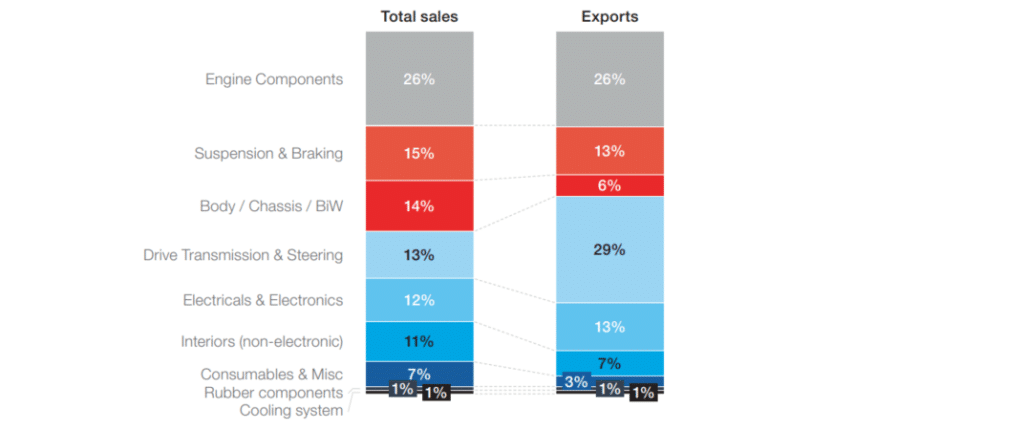

Figure 1: Auto component (by category FY25)

2. Rising and targeted technology upgrades

India is moving up the value chain, strengthening its capabilities in precision engineering and selected electrification components, including driveline and powertrain modules. While frontier areas like ADAS and SDV are nascent and dominated by global players, Indian firms are positioning themselves in adjacent segments where engineering complexity and cost competitiveness intersect. This pragmatic positioning allows them to remain competitive while progressively upgrading capabilities.

3. A demanding domestic market as a testing ground

With steady consumer-driven demand (~6% CAGR) and increasing component content per vehicle, India provides a live laboratory in which suppliers refine execution. Capabilities developed domestically, such as lean manufacturing cycles, localized production flexibility, and rapid response to changing OEM requirements, can be directly translated into international operations, where execution and responsiveness increasingly determine supplier selection.

Taken together, these factors suggest a clear shift: for leading Indian auto-component manufacturers, the constraint is no longer capability, but the limits of a single market.

Internationalization: The Natural Next Step

Domestic success has created a strong foundation for Indian auto-component manufacturers, but future growth is increasingly constrained by the limits of a single market, making international expansion the natural next phase of development.

Opportunity pools outside India are materially larger. Developed markets offer both greater scale and structurally better economics, with 10–20% higher pricing and greater component value per vehicle, translating into superior margins. Just as critically, proximity to OEMs plays a decisive role in sourcing decisions: suppliers that operate close to customers benefit from stronger qualification pipelines, better visibility on programs, and higher win rates.

Internationalization also acts as a strategic hedge. An India-only footprint exposes companies to domestic cyclicality, in addition to policy shifts and supply chain vulnerabilities; a diversified geographic base, by contrast, improves resilience. At the same time, participation in more technologically advanced ecosystems accelerates learning, enabling firms to absorb and replicate capabilities more quickly.

This combination—larger markets, better economics, risk diversification, and faster capability-building—creates a powerful flywheel. Leading Indian players are already moving in this direction, with many deriving 15% or more of their revenues internationally and aspiring to reach ~50% over time.

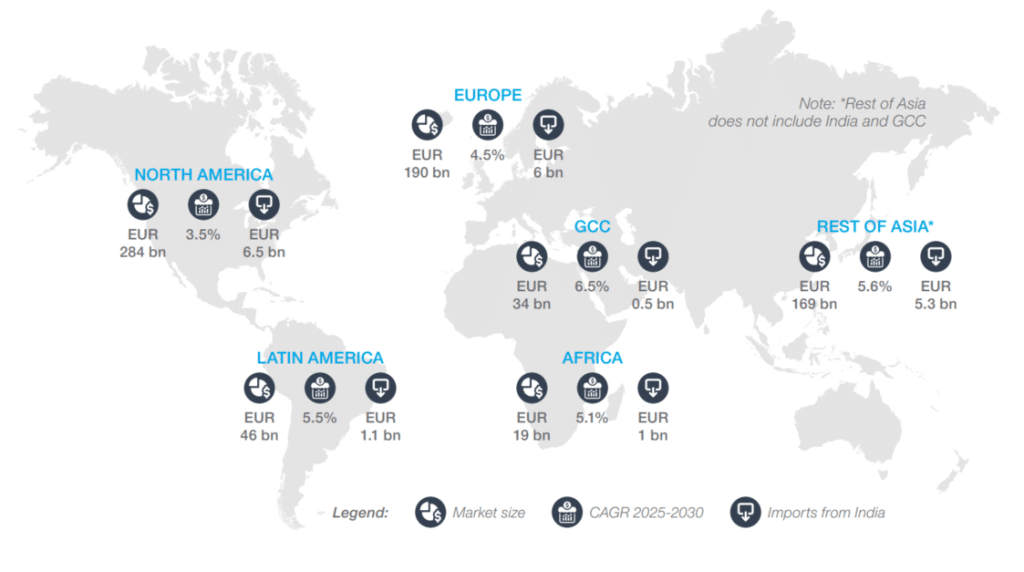

Figure 2: Regional domestic markets and imports from India in 2025

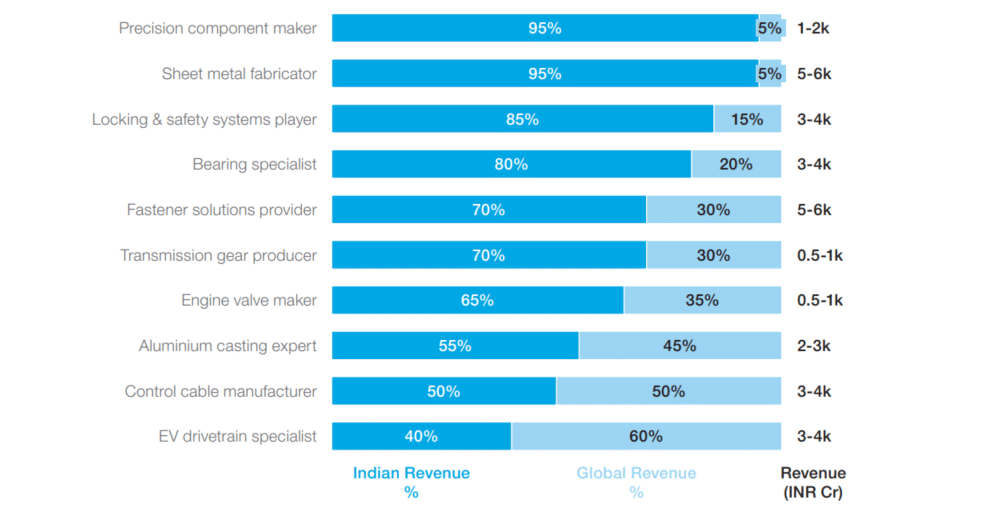

Figure 3: Share of global revenue in total revenue of Indian auto-components players (Illustrative list)

In this context, the question is no longer one of whether to internationalize, but one of where to start.

Europe: Where Opportunity Meets Timing

With an estimated EUR 190 billion domestic auto-component market growing at a ~4.5% CAGR, Europe stands out for its scale and for the current imbalance shaping its supplier landscape. While the region remains one of the most technologically advanced automotive ecosystems, it is also undergoing a period of adjustment that is creating entry points for new players.

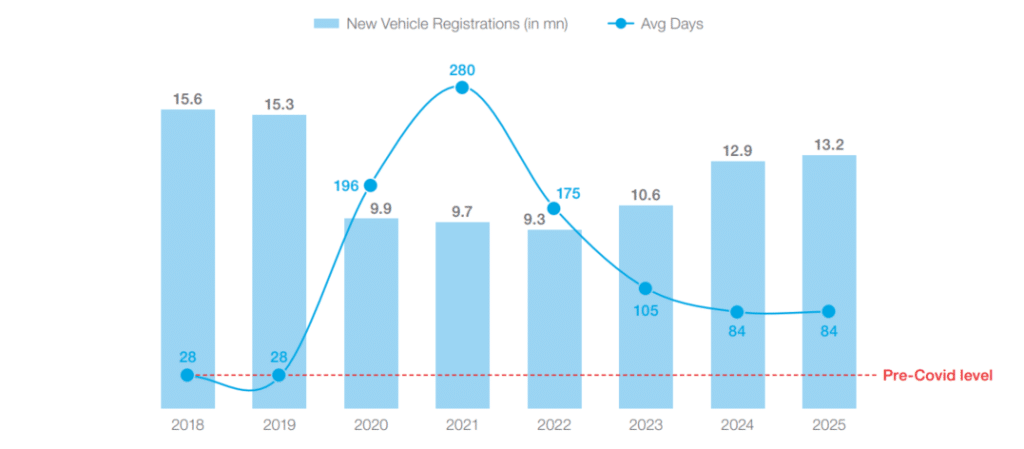

Demand remains below pre-pandemic levels (~15% lower), while the transition to electrification has become more uncertain. Hybrid powertrains are regaining traction, while BEV adoption forecasts have been revised downward from 27% to ~15%. In addition, the average vehicle age has risen from ~11 to ~13 years, moderating replacement demand but expanding opportunities in the aftermarket.

Figure 4: European vehicle backorders [in EUR billions]

Note: Avg. days computed as the median of range in market research

In parallel, suppliers are facing margin compression, with profitability declining by ~250 basis points to ~3.5%, alongside regulatory shifts, energy inflation, and high capital expenditure requirements.

Together, these dynamics are increasing uncertainty around long-term demand and investment cycles.

Slower demand, combined with rising complexity and margin pressure, is forcing incumbents to restructure, consolidate, or exit certain segments while OEMs are re-evaluating their supply chains. European OEMs are reducing exposure to concentrated sourcing risks and, in particular, are actively derisking their supply chains from over-reliance on China, creating openings for suppliers who can localize production. Near-shoring is now a clear preference: ~55% of buyers favor locally assembled vehicles, with ~$50 billion pledged for new regional plants.

This environment is translating directly into tangible entry opportunities. Financial stress among incumbent suppliers has made distressed assets available at 30–50% of replacement cost. In H1 2025 alone, there were 163 distressed deals valued at €2.5 billion, compared to 183 deals (€1.6 billion) in H1 2024. These assets offer Indian manufacturers a fast and cost-effective route to market entry.

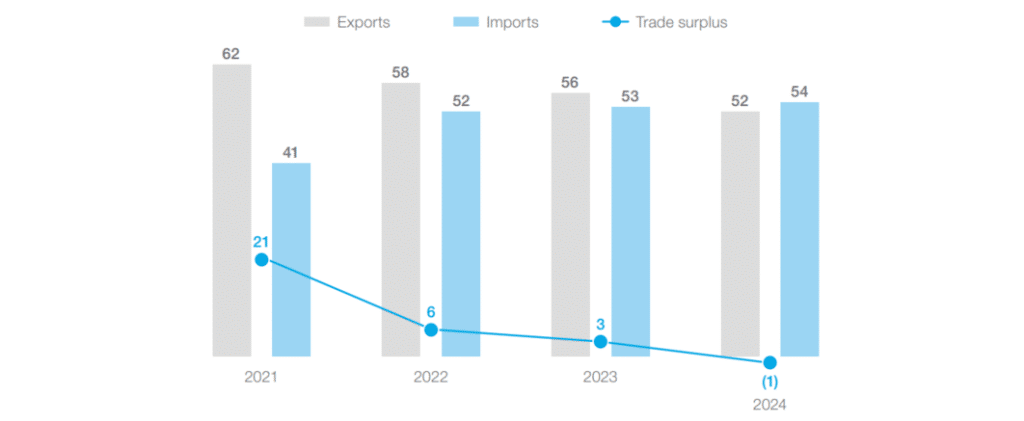

The market’s trade dynamics further enhance the opportunity. Europe’s auto-component trade balance has swung from a €20.9 billion surplus in 2021 to a €1.4 billion deficit in 2024, creating room for competitive international players. Combined with preferential access via the recently signed EU–India FTA and relatively lower tariff exposure versus the US, the region is particularly attractive for Indian firms seeking both growth and predictability.

Figure 5: European auto-components trade balance

Note: Includes conventional auto components plus batteries & semiconductors for automotive use

For Indian auto-component companies, Europe offers a perfect alignment of timing and capability. Their cost efficiency can navigate margin pressures; their operational depth supports localization; and their emerging technical capability enables selective participation in high-value components, from ADAS to EV modules. In short, Europe is a strategic proving ground. It allows Indian firms to convert domestic operational excellence into global competitiveness, while gaining exposure to advanced technologies, localization practices, and structural growth opportunities.

Pathways to Global Expansion: Turning Capability into Opportunity

Indian auto-component companies have built strong engineering capabilities, as well as cost discipline and operational agility. The challenge now lies in how these strengths are translated into sustainable positions in international markets.

Export-led approaches leveraging existing client relationships or working through commercial agents can provide fast, low-risk access to new markets. However, they typically offer limited visibility on OEM programs and reduce direct customer engagement. In a market where sourcing decisions are highly proximity-driven, these models often constrain long-term positioning.

Partnerships and joint ventures offer deeper integration, combining Indian cost and engineering advantages with local market access. They can accelerate credibility but require moving beyond a transactional role to avoid remaining confined to an “India-only” position within global supply chains.

Local presence or acquisitions offer the most direct route to embedding within European value chains. Building a European facility, acquiring a distressed supplier, or merging with a regional player offers immediate access to customers, programs, and advanced technology. Yet these routes require patience and cultural sensitivity, along with disciplined execution. Ultimately, value creation depends on how well the strategy is executed—particularly in choosing the right assets and maintaining local management—while integrating operations without disrupting existing customer programs. Missteps, whether in product-market alignment, integration approach, or understanding of local regulations, can quickly turn opportunity into costly setbacks.

Some Indian players are experimenting with hybrid or dual-shore strategies, producing labor- or energy-intensive components in India while completing final assembly in Europe. This approach blends India’s cost advantage with local credibility, delivering both efficiency and proximity to key OEMs.

In practice, international expansion is less about choosing a single model than about acting decisively in a shifting landscape. For Indian auto-component firms, global markets represent a way to strengthen their positioning within increasingly competitive and technologically advanced automotive value chains.

Learning from Experience: How Players Win in Europe

Europe has long been both a challenge and an opportunity for Indian auto-component companies.

Bharat Forge illustrates how targeted acquisition can accelerate entry into European value chains when combined with strong local integration. Its acquisition of CDP enabled access to BMW, Volkswagen and DaimlerChrysler programs worth millions. It leveraged India’s engineering talent while investing in building local management teams and integrating them into the existing supply chain. This combination of industrial capability and on-the-ground integration was critical in converting an acquisition into sustained business.

De même, Motherson has shown how distressed or underperforming assets can become engines of growth. The company systematically targets businesses with strong strategic fit, even if they are operationally challenged, and applies its own playbook to restore profitability. Critical to this approach is local autonomy coupled with tight central financial control, ensuring speed and responsiveness while maintaining strategic oversight.

Not all attempts succeed. BYD’s €4bn investment in Hungary illustrates the risks of misreading the market. Treating Europe as a homogenous block, focusing too heavily on BEVs where demand was slower than expected, and importing labor without local integration led to regulatory scrutiny and costly delays. Structural understanding and execution discipline tend to outweigh scale or capital alone.

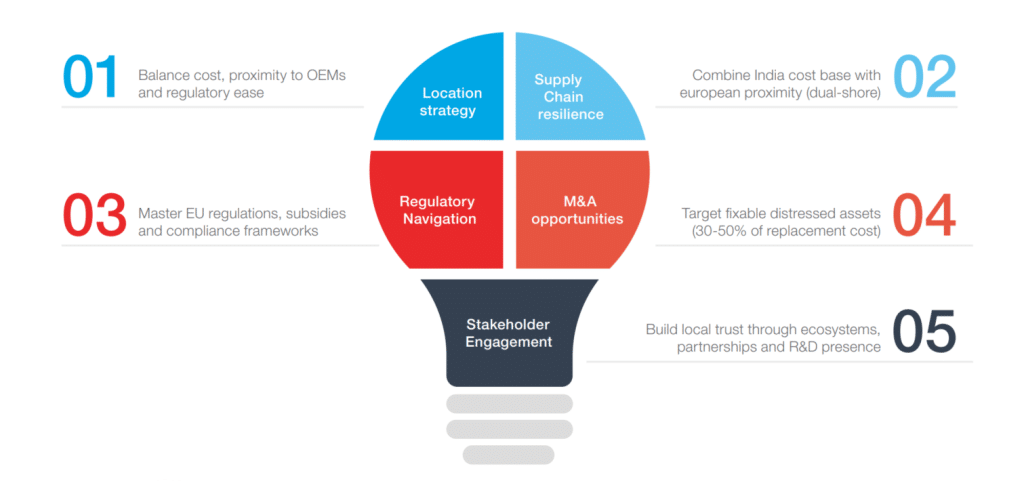

From these examples, five pillars emerge for Indian players seeking success in Europe:

Conclusion: The Path Forward, Shaping Global Success

The trajectory of India’s auto-component industry is increasingly shaped by how companies extend their capabilities beyond the domestic market. Many players have built strong foundations in scale, cost efficiency, and operational depth; the next phase will depend on how effectively these strengths are deployed in more demanding international environments.

Expanding internationally introduces a different set of requirements. For many firms, this represents a structural evolution in how the business is run. Each strategy will in its own manner shape access to programs, resilience of revenue, and long-term relevance in the value chain.

Europe currently offers a rare combination of scale, technological depth, and market dislocation.

Ongoing supplier restructuring and shifts in supply chains, combined with the availability of underperforming assets, have opened a window for new entrants. This creates opportunities to establish a foothold in ways that would be far harder in a more stable environment.

Those that move later or underestimate the complexity of this transition may face a more competitive and less accessible environment as conditions stabilize.

For Indian auto-component companies, the question is therefore not only where to expand, but how to do so in a way that strengthens their position over time. The ability to translate domestic strengths into global operating models is likely to define which players emerge as long-term partners in the evolving automotive ecosystem.

Anuj Rikhye – Partner, Accuracy

Jean-François Partiot – Partner, Accuracy

Frédéric Recordon – Partner, Accuracy

Shifting Gears – The Case for Indian Auto-Component Companies to Expand Internationally