The Accuracy View

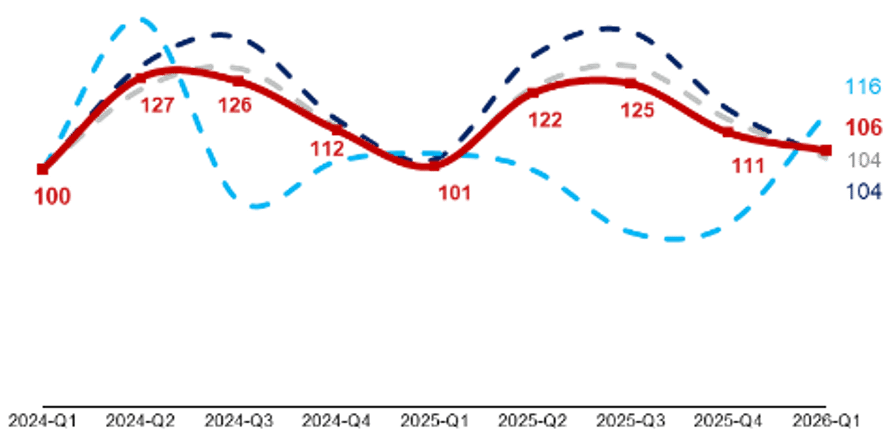

Q1 2026 confirms a structural shift in European hospitality: resilient but fragmented growth, luxury-led performance, and increasing pressure on midscale assets. With demand holding but margins tightening, value creation now hinges on asset positioning and operational resilience rather than pricing power alone.

Italy posted the strongest Q1 2026 performance (+21.4% RevPAR YoY), largely driven by the Milano-Cortina Winter Olympics. While Italy’s performance remained predominantly rate-driven due to event pricing, the broader European market was gradually shifting back to occupancy-led RevPAR growth.

Luxury outperformance was significant this quarter. Across Europe, Luxury & Upper Upscale assets continued to post positive RevPAR growth while Midscale & Economy performance remained weaker. The performance gap appears increasingly persistent, although further quarters will be needed to distinguish structural from cyclical effects.

Q2 2026 appears cautiously optimistic. Softer US travel budgets and weaker long-haul demand indicators may create a headwind for European luxury markets that rely heavily on high-spending American visitors. Additional pressure could also arise from higher energy prices and broader geopolitical volatility.

Regulatory risk emerged as a more material and still underpriced factor in Q1 2026. The CMA investigation into Hilton, IHG and Marriott, the increase in UK business rates from April 2026 and Amsterdam’s VAT increase on hotel accommodation in January 2026 all point to a tighter operating environment across Europe.

Accuracy Index – Q1 2026

Sources: Mergermarket, CoStar, EuroStar and Accuracy analysis

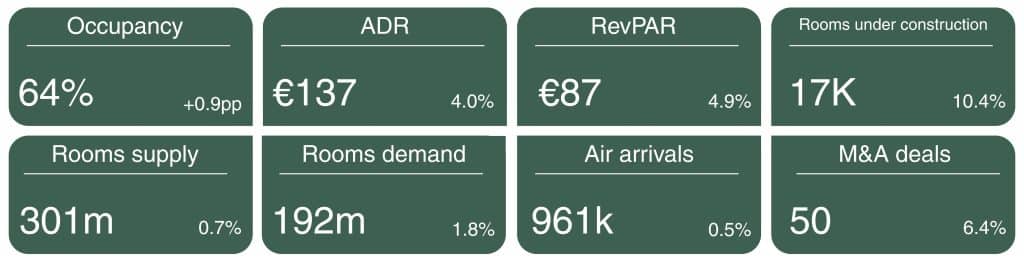

OPERATIONAL PERFORMANCE

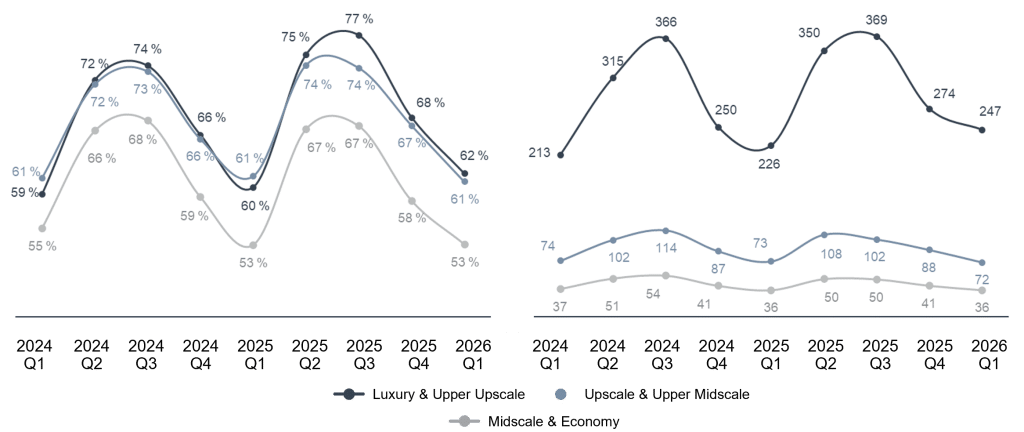

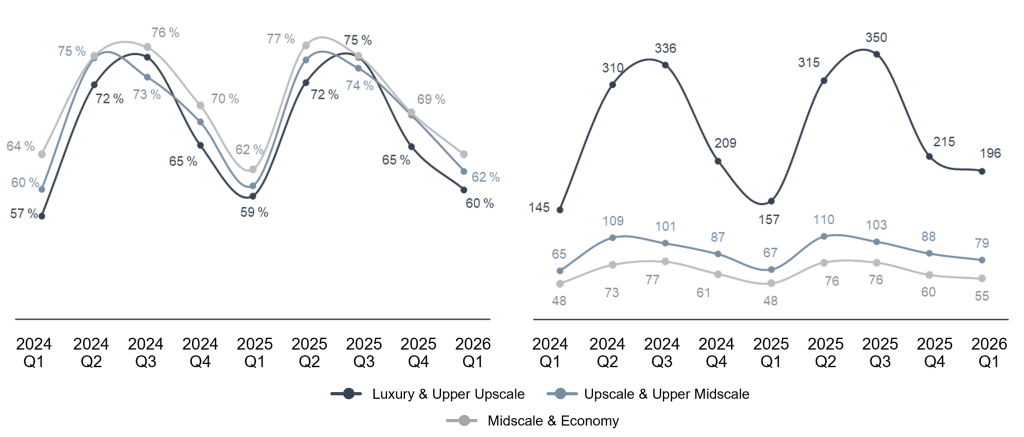

France: Paris luxury surges while budget segment softens

Evolution of occupancy (in %)

Evolution of RevPAR (in €)

Sources: CoStar and Accuracy data analysis

Paris drove another quarter of outperformance for the Luxury & Upper Upscale segment, with RevPAR reaching €247 (+9.0% YoY) on occupancy of 62%. A dense events calendar sustained elevated demand throughout the quarter, from Men’s Fashion Week and Haute Couture Week in January to Six Nations home fixtures at Stade de France.

Midscale & Economy hotels saw RevPAR remain broadly flat at €36 (-0.1% YoY), reflecting weaker business-travel budgets and increasing downside risk for smaller, cost-sensitive operators.

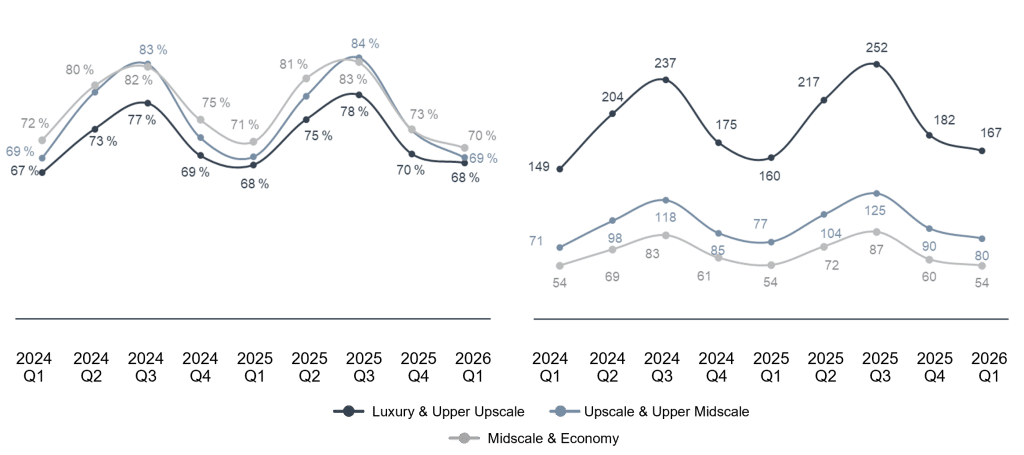

Germany: Trade fair calendar sustains modest broad growth

Evolution of occupancy (in %)

Evolution of RevPAR (in €)

Sources: CoStar and Accuracy data analysis

Germany delivered broad but modest RevPAR growth in Q1 2026, with all three segments recording positive YoY gains. Cologne led the pack in January, with hotel RevPAR up +23.2% YoY, driven by the IMM Cologne furniture fair.

Munich, Berlin, Hamburg and Cologne were the only German cities to reach European average occupancy levels, underscoring the concentration of demand in key metropolitan markets. For full-year 2026, ADR and RevPAR are expected to grow by 1% to 3% across Germany. However, rising operating costs are likely to keep margins under pressure, particularly in the Economy segment.

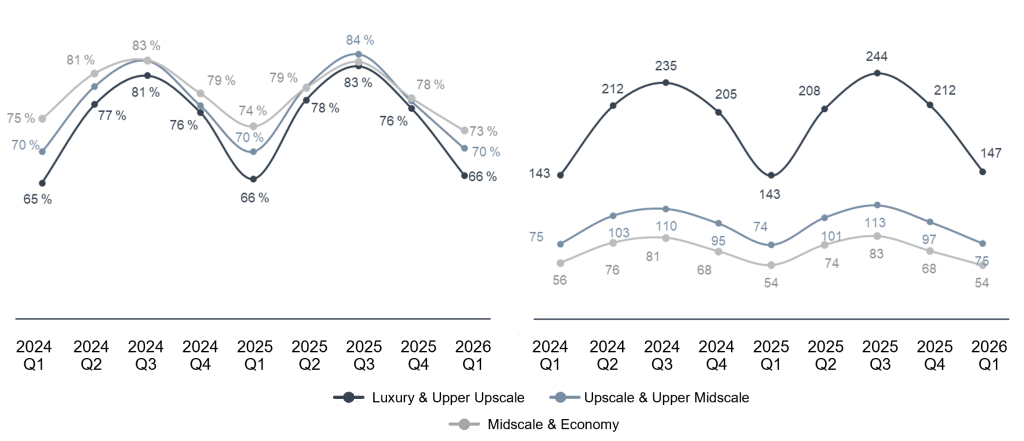

Italy: Milano-Cortina Olympics propel record Q1 performance

Evolution of occupancy (in %)

Evolution of RevPAR (in €)

Sources: CoStar and Accuracy data analysis

Italy delivered the strongest Q1 performance in the dataset, with average RevPAR up +21.4% YoY to €110, driven primarily by the Milano-Cortina Winter Olympics. The Luxury & Upper Upscale segment posted RevPAR of €196 (+25.1% YoY), while occupancy remained broadly stable at 60%, confirming that the rate was the main growth driver. During the Games, Milan’s hotel market reached record occupancy of 83.4%. The Olympics effect also lifted other segments, with Midscale & Economy RevPAR rising to €55 (+12.9% YoY) on occupancy of 64%.

Spain: Mobile World Congress powers luxury gains

Evolution of occupancy (in %)

Evolution of RevPAR (in €)

Sources: CoStar and Accuracy data analysis

Spain’s hotel market maintained positive momentum in Q1 2026, with Luxury & Upper Upscale reaching RevPAR of €167 (+4.2% YoY), while occupancy remained near flat at 68%. Barcelona was the standout demand driver in March, with the Mobile World Congress (2–5 March) drawing over 105,000 attendees from 207 countries, pushing hotel bookings to 93% in March. Midscale & Economy performance continued to soften, with occupancy declining to 70%, prolonging the weakness initially observed in Q4 2025. Spain’s growth trajectory increasingly reflects a two-speed market, with pricing power concentrated in luxury urban and resort assets while Midscale & Economy segments face structural strain, as domestic travellers remain highly price-sensitive.

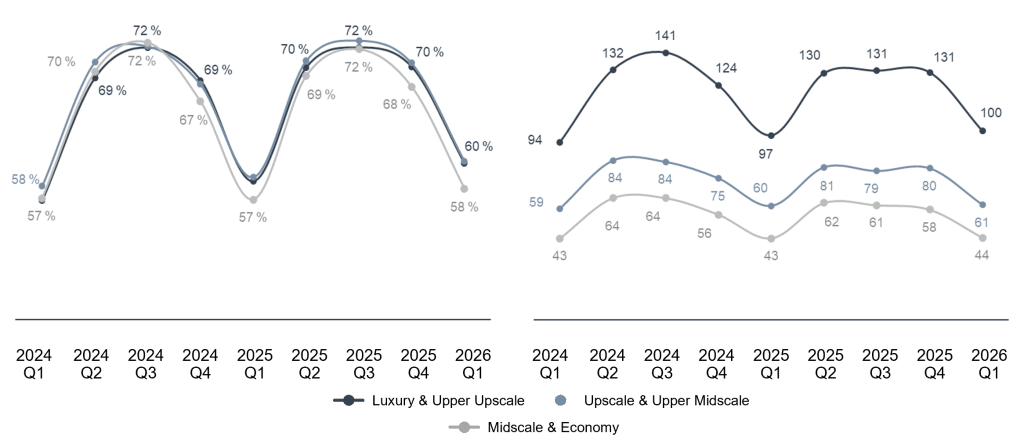

UK: Rising costs and policy shifts cloud Q1 performance

Evolution of occupancy (in %)

Evolution of RevPAR (in €)

Sources: CoStar and Accuracy data analysis

UK posted the most subdued Q1 2026 performance of the five markets, with average RevPAR growing just +1.7% YoY to €92 across the three segments, as overall occupancy remained relatively flat at 70%. The operating landscape has become increasingly challenging, shaped by the cumulative effect of recent policy shifts. It includes higher business rates, rising employment costs, and new regulatory obligations. These regulatory measures are increasingly constraining margin expansion and limiting near-term upside in the UK market. The strong rise in business rates from April 2026 is expected to erode margins across all segments, with Central London hotels already posting a 0.9% RevPAR decline while maintaining a 46.8% GOP margin through disciplined cost control.

INVESTMENT PERFORMANCE

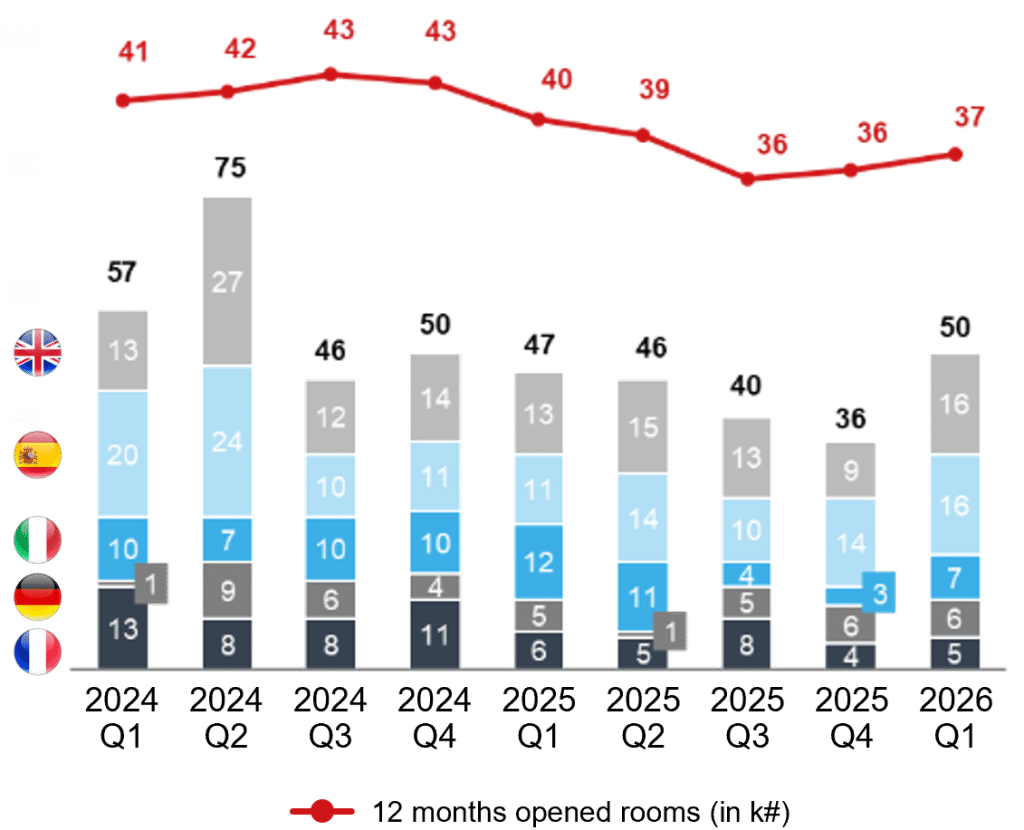

Number of hotel transactions vs. 12-month room openings

Sources: Mergermarket and CoStar

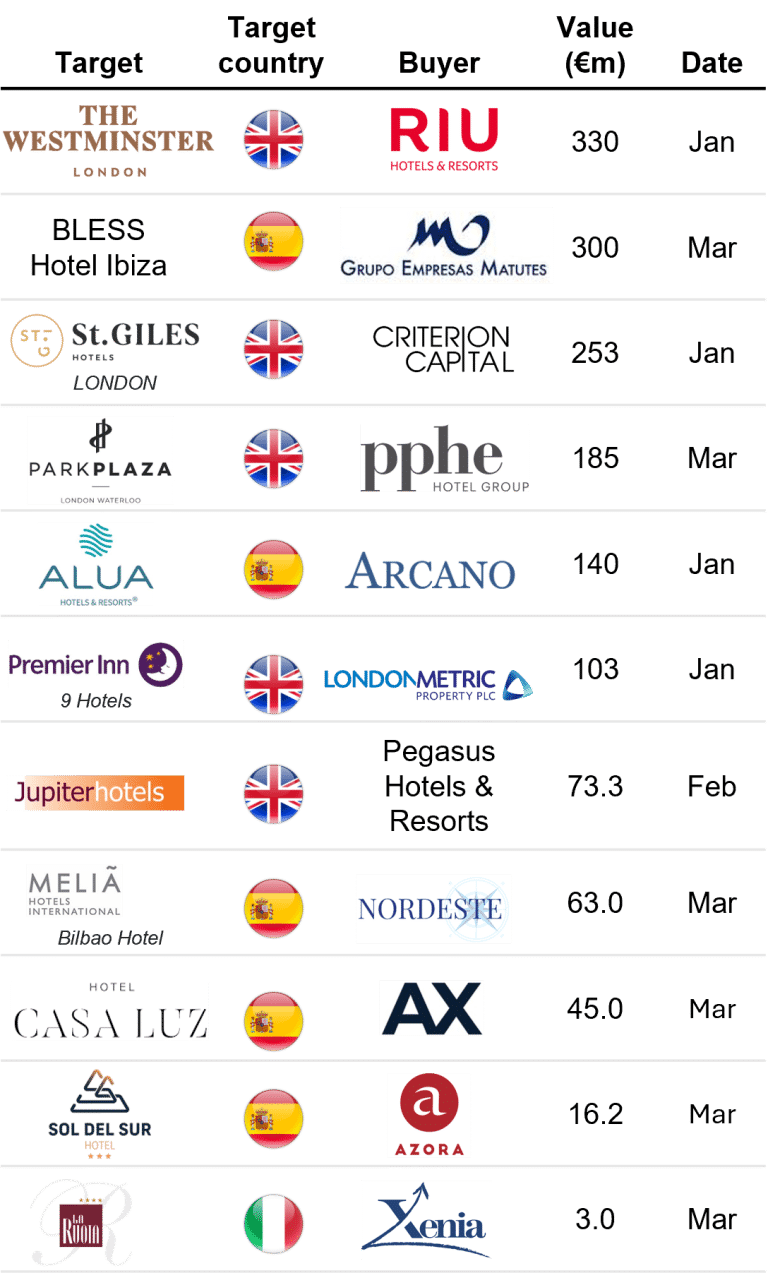

Deal flow rebounded to 50 transactions in Q1 2026, up +6.4% YoY from 47 in Q1 2025 and the highest quarterly count since Q4 2024, confirming a recovery after four consecutive quarters of declining activity. The UK and Spain concentrated the largest individual deals, confirming sustained global appetite for prime UK trophy assets and strong investor conviction in resort leisure assets.

Large-scale transactions above €250m are forecast to increase significantly in 2026. Large deals have also been announced in France (Belambra/Antin and Essendi/Blackstone).

Main European hospitality transactions – Q1 2026

Sources: Mergermarket and news

TOURISM PERFORMANCE

Air arrivals and hotel demand

Sources: Eurostat and Accuracy data analysis

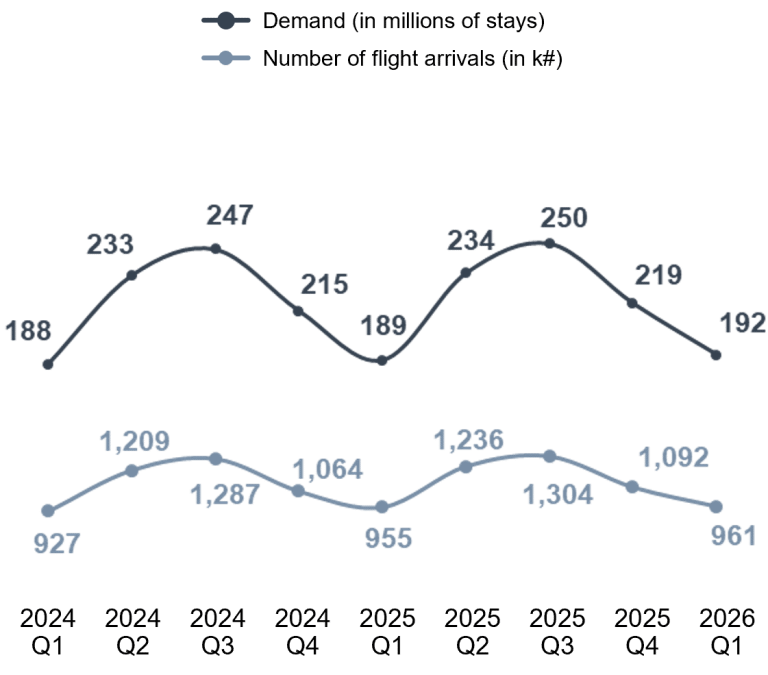

Q1 2026 air traffic growth decelerated sharply to +0.5% YoY (961k total arrivals), well below the +3.1% recorded in Q1 2025. First, Europe-Middle East routes were severely disrupted by regional airspace closures, with weekly traffic down -51% YoY by late March. Second, jet fuel prices ended the quarter at $4.73 per gallon, twice as high as at the beginning of the year, constraining airline capacity additions.

Against this backdrop, hotel demand proved more resilient, reaching 192 million stays (+1.8% YoY), outpacing arrivals growth and pointing to stronger conversion rates among arriving passengers.

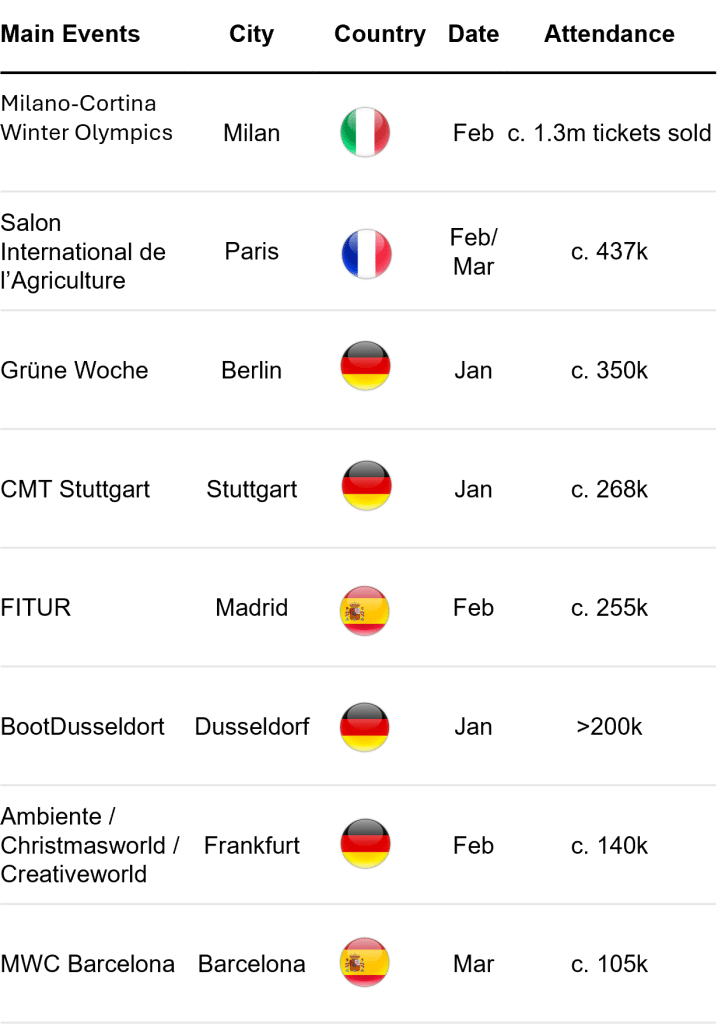

Key European festivals and attendance

Sources: News

ÉVALUATION

Hotel sector’s EV/EBITDA multiple1

Sources: S&P Capital IQ

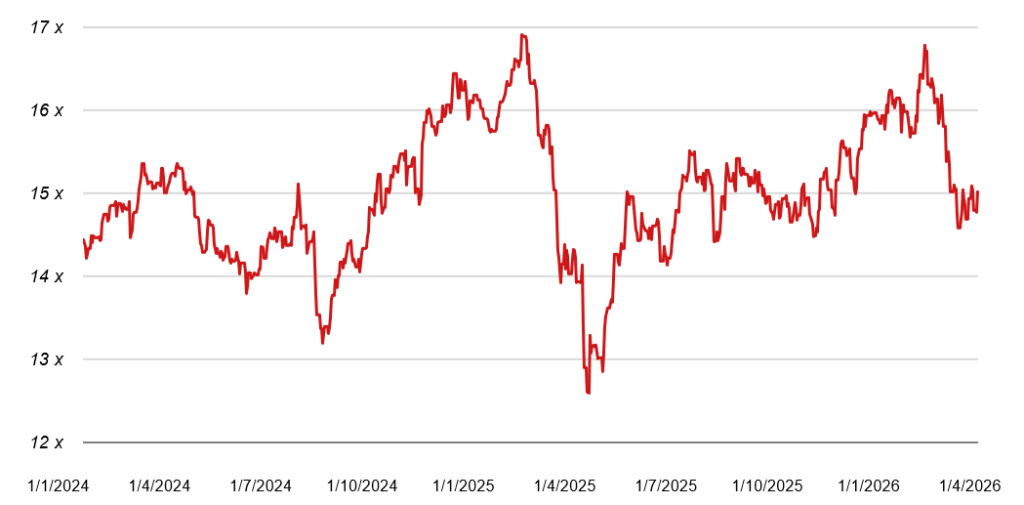

The hotel sector’s EV/EBITDA multiple rose from 15.8x to a peak of 16.8x in early February, supported by a strong Q4 earnings season and sustained investor confidence in asset-light business models. A subsequent correction brought the multiple back to 15.0x by the end of March – in line with its two-year average – due to broader market volatility, further amplified by regulatory developments (CMA investigation into pricing practices) and geopolitical tensions affecting travel flows. Importantly, valuation resilience despite these shocks highlights continued investor conviction in the sector’s long-term fundamentals, particularly for high-quality, asset-light platforms.

However, the growing disconnect between capital markets performance and underlying operating conditions, especially rising costs and pressure on Midscale segments, suggests that valuation upside will increasingly depend on asset quality, pricing power and operational efficiency rather than market-wide growth.

OUTLOOK

European RevPAR growth is expected to remain positive but moderate in 2026, in the range of 1–3% at European level.

However, the market is becoming structurally more complex. While geopolitical tensions and air traffic disruptions are weighing on long-haul demand – particularly from the US – these effects are partly offset by demand reallocation toward Southern European leisure markets, supporting occupancy in Spain and Portugal.

At the same time, rising travel costs and weakening consumer confidence are starting to constrain discretionary spending, creating increasing pressure on midscale and price-sensitive segments, while high-end assets remain more resilient.

In terms of capital, investment volumes are expected to recover, supported by strong liquidity and continued investor focus on prime, luxury and value-add opportunities, with limited appetite for secondary assets. European hotel investment volumes are projected to reach €27bn in 2026, with 86% of investors expecting to deploy capital equal to or greater than 2025 levels. Overall, the key shift for 2026 is a move from broad-based growth to selective performance: asset quality, location and customer mix will increasingly determine outcomes, as margin pressure intensifies and pricing power remains uneven across segments.

Jérémie Israël – Partner, Accuracy

Simon Perez – Partner, Accuracy

Nicolas Paillot de Montabert – Partner, Accuracy

Hospitality in Europe at a glance – Q1 2026