The Accuracy View

We are proud to present a new edition of the European hospitality index covering operations in France, Italy, Germany, Spain, and the UK.

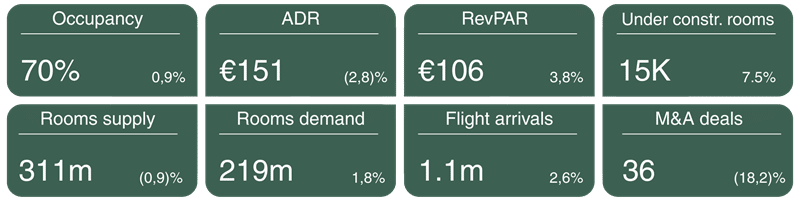

We are particularly impressed by Germany’s hotel market, which delivered an excellent Q4 2025 with RevPAR up +6.1%, supported almost across all segments and boosted notably by Oktoberfest in Munich or fairs in Dusseldorf.

Luxury & Upper Upscale continue to capture the majority of European RevPAR growth, confirming sustained pricing power and supporting premium asset valuations in gateway cities.

Midscale & Economy assets are increasingly exposed to margin compression, as demand softens while cost inflation remains elevated — a structural concern for secondary locations and leveraged operators. Revo difficulties in Germany / Austria exemplify this trend.

Transaction volumes remain selective, with capital concentrating on single-asset prime deals. Portfolio transactions remain limited, reflecting pricing gaps and continued underwriting discipline. Valuations finish the year higher, signaling strong confidence and anticipated growth in the hotel sector, notably with large groups benefitting from upscaling strategies (Mariott, IHG) as well as AI deployment (Accor).

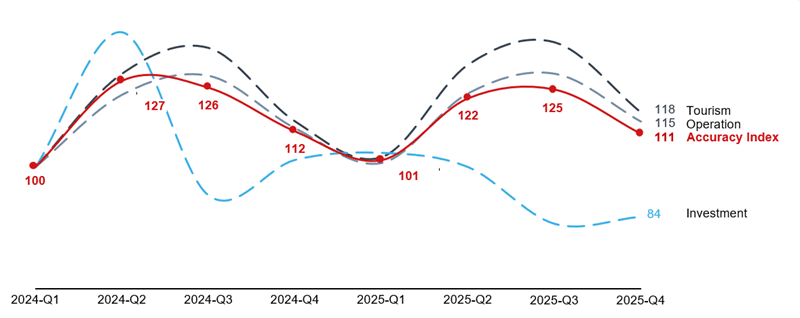

Accuracy Index – Q4 2025

Sources: Mergermarket, CoStar, EuroStar and Accuracy analysis

OPERATIONAL PERFORMANCE

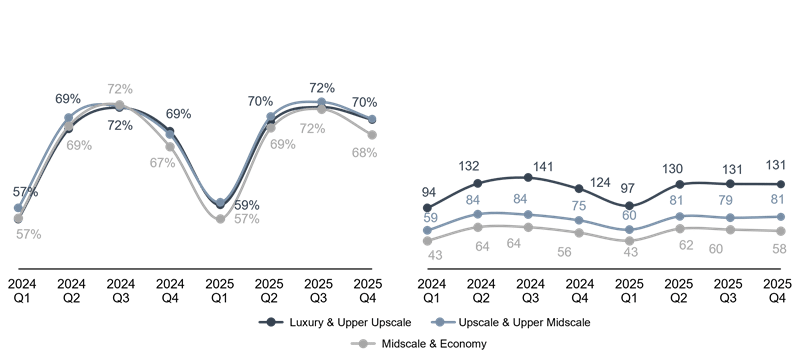

France: Luxury outperforms as other classes stall

Evolution of occupancy (in %)

Evolution of RevPAR (in €)

Sources: CoStar and Accuracy data analysis

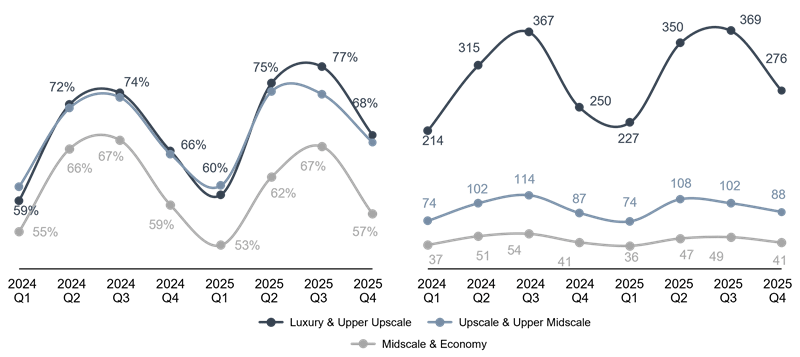

Luxury & upper-upscale hotels saw RevPAR skyrocket, posting a +10.8% YoY increase (reaching €276) with +2 points in OR (reaching 68%). Paris was the primary driver of this growth, with strong end of year period, fueled by a surge in high-spending international tourists, particularly from the U.S. and the Middle East.

By contrast, Midscale & Economy segment saw stable RevPAR at €41, reflecting weaker occupancy and price challenges, looming challenging margins for operators.

The divergence between luxury and midscale segments implies widening valuation spreads, with prime Paris assets likely to maintain pricing support, while secondary assets may face increased refinancing pressure in 2026, explaining the slowdown on several portfolio transactions (notably in midscale, eco and super eco) .

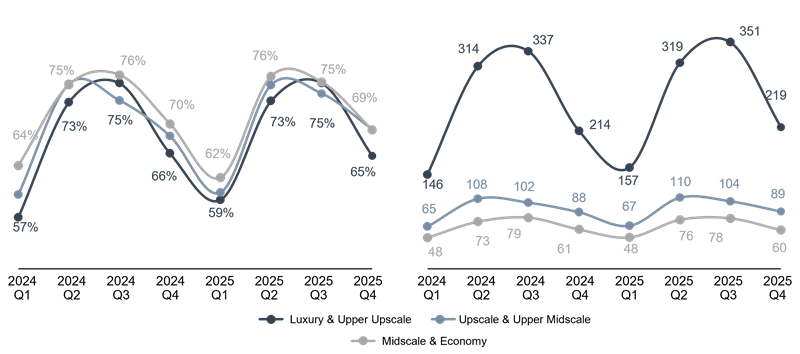

Germany: Excellent performance driven by Oktoberfest

Evolution of occupancy (in %)

Evolution of RevPAR (in €)

Sources: CoStar and Accuracy data analysis

Q4 2025 was positive across the entire German hotel sector, with RevPAR rising +6.1% YoY. Performance was broadly uniform across segments, supported equally by volume and price effects, each contributing roughly 50% to growth. Germany benefitted from strong tourism demand, driven by fairs, notably in Munich (Oktoberfest) or Dusseldorf.

The insolvency of Revo highlights growing vulnerability among cost-sensitive operators in the economy segment, particularly in highly competitive regional markets.

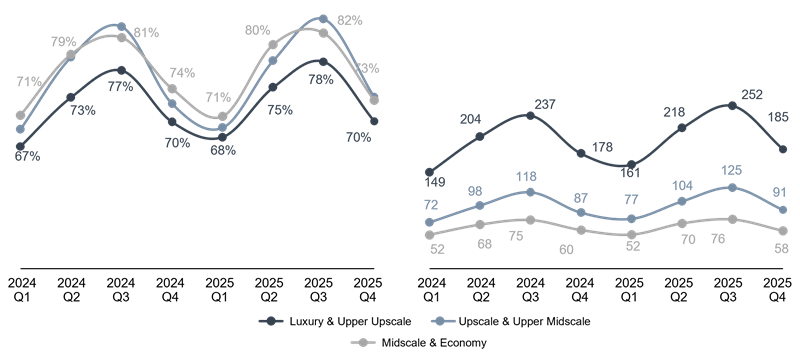

Italy: Stable occupancy for Luxury

Evolution of occupancy (in %)

Evolution of RevPAR (in €)

Sources: CoStar and Accuracy data analysis

Stable occupancy despite increased supply indicates sustained demand depth; however, the slight decline in luxury occupancy suggests that pricing discipline will be key to preserving margins in 2026. Tourist arrivals continue to grow during the low season, particularly in key destinations such as Rome, Venice, and Florence, as travelers seek lower prices and smaller crowds. Hoteliers have adapted by increasingly choosing to remain open, expanding room availability during this period. As a result, overall occupancy has remained stable compared to last year. However, contrary to the broader European trend, luxury and upper-upscale hotels experienced a slight decline in occupancy (-0.5% YoY).

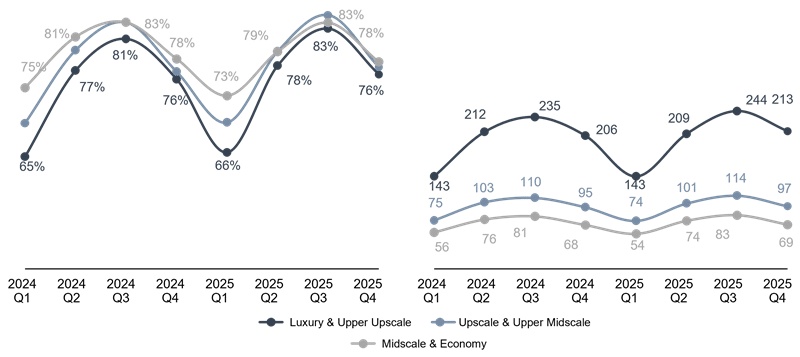

Spain: Historic decline in the midscale & economy class

Evolution of occupancy (in %)

Evolution of RevPAR (in €)

Sources: CoStar and Accuracy data analysis

The first RevPAR contraction in several years may mark a turning point in the Spanish cycle, particularly for price-sensitive segments. Investors should reassess short-term growth assumptions in secondary coastal markets. Q4 2025 saw muted demand growth in the Spanish hotel market, reflecting an already high base. Price increases supported comfortable RevPAR growth for luxury & upper-midscale and upscale & upper-midscale segments, which rose +3.8% and +4.9% YoY, respectively. In contrast, midscale & economy hotels, targeting price-sensitive travelers, largely held rates flat. Coupled with declining occupancy, RevPAR in this segment fell -2% YoY.

UK: Weak demand growth and price increase to offset inflation

Evolution of occupancy (in %)

Evolution of RevPAR (in €)

Sources: CoStar and Accuracy data analysis

All hotel segments in the UK increased their rates, with ADR up +4% YoY. The catch-up in ADR reflects delayed inflation pass-through, but increasing business rates and new supply in London may limit further pricing upside in 2026.

The price increase is exerting some downward pressure on demand. Overall occupancy in Q4 remained stable compared to last year, supported by an already high base. However, strong demand in London was offset by a record number of hotel openings in 2025, particularly in the luxury segment, resulting in a slight decline in citywide occupancy (-1% YoY).

INVESTMENT PERFORMANCE

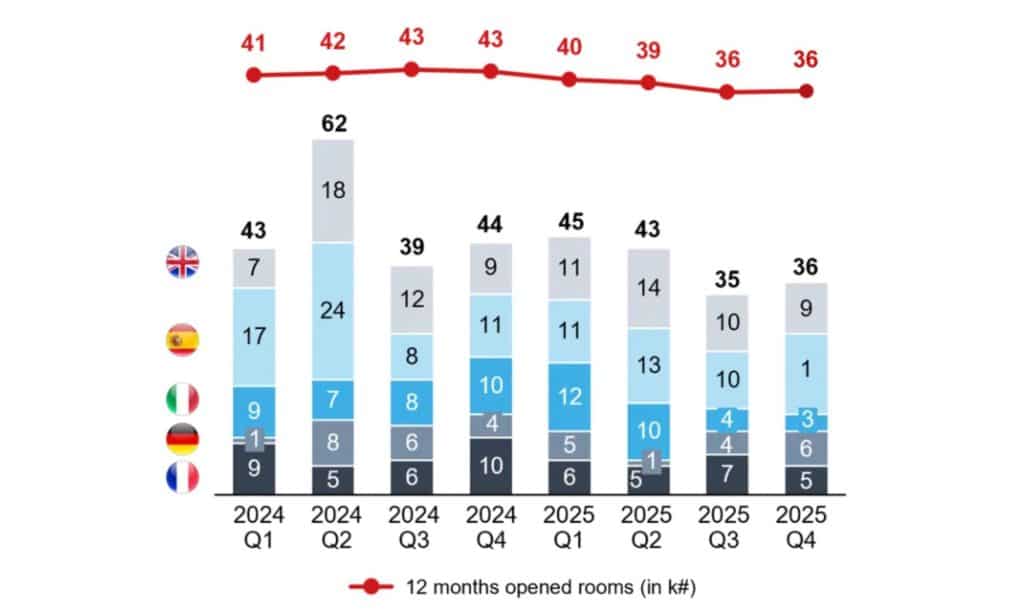

Number of hotel transactions vs. 12-month room openings

Sources: Mergermarket and CoStar

Quaterly deal flow remained stable with Q3 2025. Investment activity remains concentrated on trophy assets in core cities, while portfolio transactions remain subdued due to valuation gaps between buyers and sellers. Overall, the market remains polarised, with capital gravitating toward prime assets in key gateway cities.

The €900m of high-end transactions in London confirms continued global appetite for prime European hospitality despite elevated financing costs.

Main European hospitality transactions – Q4 2025

TOURISM PERFORMANCE

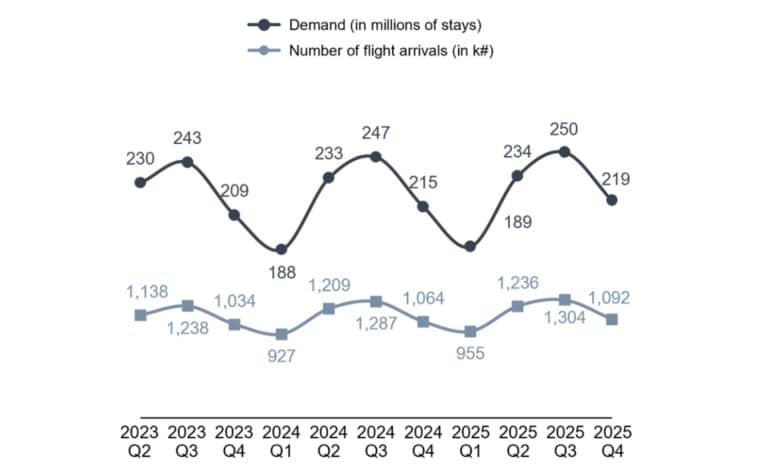

Air arrivals and hotel demand

Sources: Eurostat and Accuracy data analysis

Q4-2025 tourism showed reasonable growth, with air traffic up 2.6% compared with last year. The gradual return of long-haul travelers (US, China, Middle East) reinforces demand quality, supporting luxury and upper-upscale positioning in major capitals. However, constrained airline capacity limits the pace of full recovery

Arrival quality remained strong, supported by a rise in high-spending American and Middle Eastern tourists. In contrast, Japanese travelers, affected by a weaker yen, favored domestic travel. Oil prices, around $62 per barrel, contributed to lower airfare costs.

Key European festivals and attendance

ÉVALUATION

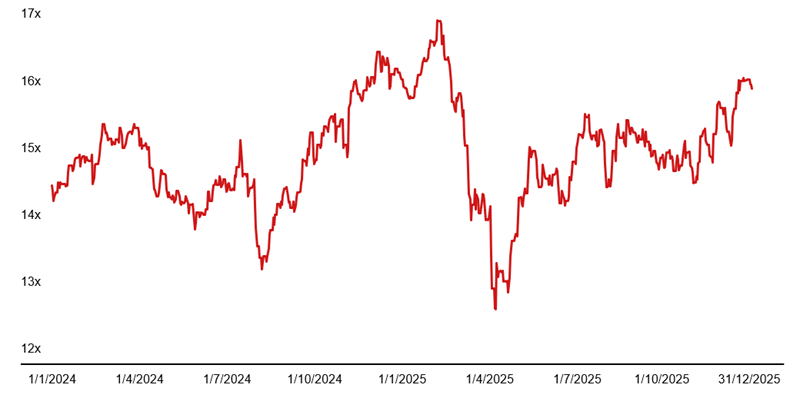

Hotel sector’s EV/EBITDA multiple1

Sources: S&P Capital IQ

The hotel sector’s EV/EBITDA multiple has surged over the last three months of 2025, hitting around 16x by the end of the year, reaching its almost high since January 2024. This is well above the two-year historical average of 14.9x. This increase is driven by RevPAR running above 2019 levels in key markets, positive 2026 EBITDA revisions, a ~40–60bps decline in US 10Y yields (back below ~4.3%), and recent M&A transactions clearing at 15x+ multiples.

OUTLOOK

Room demand in 2026 is expected to follow the momentum of 2025, with inbound travel driving a significant contribution (+6%). Chinese tourists are particularly anticipated to return.

After a strong 2025 performance in Germany, 2026 is projected to be another robust year, driven more by new rooms than RevPAR growth, expected to range between 1% to 3% at European level (Source: CBRE 2026 Report).

Lower inflation should ease pressure on Economy & Midscale hotels; however, 2026 may remain a challenging year for these segment, notably at margin levels. The luxury & upper upscale segment is expected to outperform, supported by strong pricing power and new hotels (Louis Vuitton hotel in Paris, Airelles Venezia, Six Senses London, Six Senses Bendor…).

A modest decline in interest rates is expected, which implies that the cost of capital will remain high. We expect investors to continue prioritizing quality assets with a highly selective approach.

Jérémie Israël – Partner, Accuracy

Simon Perez – Partner, Accuracy

Nicolas Paillot de Montabert – Partner, Accuracy

Hospitality in Europe at a glance – Q4 2025