Upon the release of Q1 2026 earnings results, major U.S. banks such as JPMorgan, Goldman Sachs, and Bank of America have once again demonstrated strong performances, driven by buoyant market activities.

While attention is focused on New York, another story is unfolding, more quietly, yet just as instructive, north of the border.

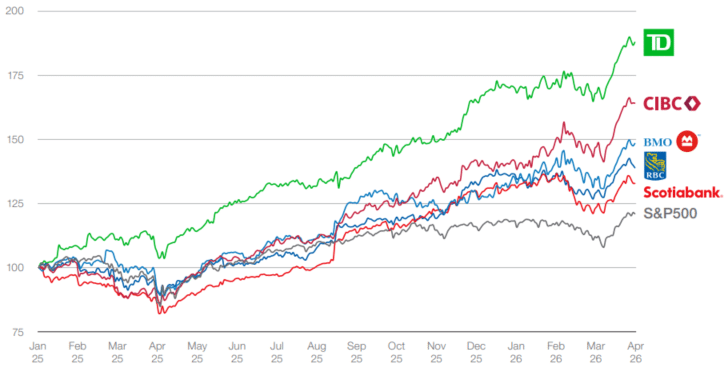

Since early 2025, the “Big Five” Canadian banks (RBC, TD, BMO, Scotiabank, and CIBC) have all outperformed the S&P 500. This performance is even more remarkable given the challenging underlying economic environment which includes tariffs and tensions with the U.S. (Canada’s main trading partner), rising unemployment, pressure on the real estate market, and an increasingly polarized economy.

Share price performance of the Big Five since January 1, 2025 (indexed to 100)

How, then, have Canadian banks managed to deliver such strong stock market performance in the face of this uncertainty?

1. A shift toward “non-NII” revenues: capital markets and wealth management

In the context of a banking environment with slowing lending activity, Canadian banks have benefited from a pivot toward capital markets and wealth management businesses. They have capitalized on a favorable environment: rising equity markets (mechanically scaling up assets under management), increased volatility (supporting trading volumes and hedging activities), and a recovery in origination activities (generating fees in capital markets).

This shift in the revenue mix is more than just a marginal change. It reduces dependence on net interest income (NII) in the context of rate normalization, while favoring less capital-intensive revenue streams. This results in an accretive effect on profitability, with ROE supported by higher fee-based activities and stronger operating leverage.

2. Balance sheet quality: a successful combination of NII and cost of risk

Another key driver has been the structural strength of Canadian banks’ balance sheets, reflected through two complementary dynamics.

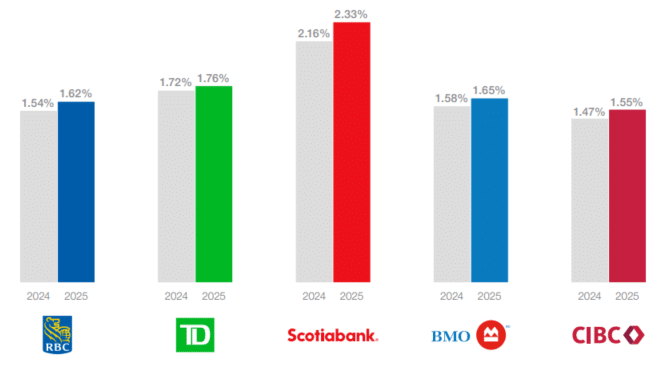

The first is net interest margin. Between June 2024 and March 2025, the Bank of Canada cut its key rates seven times, a shift that, in theory, should have mechanically compressed margins. In practice, the impact remained limited and even slightly positive for the Big Five as a whole.

Evolution of net interest margins relative to outstanding balances of major Canadian banks (2024–2025, %)

Banks benefited from a repricing asymmetry between assets and liabilities. Funding costs adjusted downward more quickly than asset yields, mechanically supporting margins.

On the liability side, deposit remuneration rapidly declined in line with policy rates. This effect is particularly pronounced in Canada, where the oligopolistic market structure limits competition for retail deposits. It was accompanied by a second favorable shift: a move from term deposits to demand deposits (a 3-point increase in demand deposits was recorded among the Big Five between the end of 2024 and 2025, with the largest gains observed at Scotiabank and BMO, rising by 3.7 and 4.1 points, respectively). In a lower-rate environment, clients favored liquidity over yield, further reducing the banks’ average cost of funding.

On the asset side, the adjustment has been more gradual. Part of the loan book, particularly semi-variable rate loans, reprice slowly, while margins in the corporate segment remain robust.

The second dynamic relates to the normalization of the cost of risk. After a peak in provisioning in early 2025, particularly due to tensions with the U.S. and an uncertain macroeconomic environment, an improvement has since been observed. This easing reflects overall resilient asset quality, historically disciplined underwriting, and relatively limited exposure to the riskiest segments. This is even more noteworthy as risks related to private credit in the United States appear to be intensifying, raising investor concerns.

3. Profitability over “growth at all costs”: a winning strategy

A third, more qualitative yet consequential factor is execution discipline.

Unlike some international banks, large Canadian banks have historically avoided risky international expansion, maintained rigorous capital allocation, and prioritized profitability over “growth at all costs”.

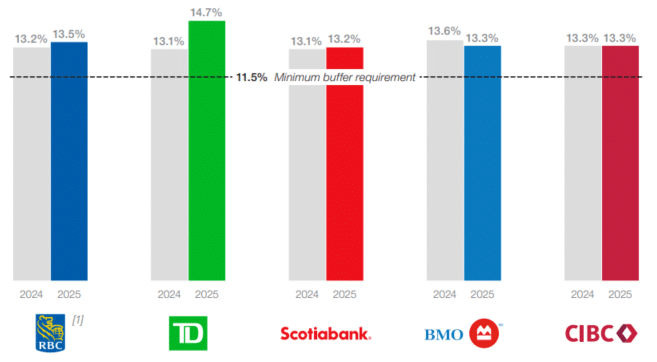

This positioning is now reflected in high capital levels (CET1), providing significant flexibility both for investment and shareholder returns, as well as competitive cost-to-income ratios relative to peer groups, reflecting past efficiency efforts.

Evolution of CET1 ratios of major Canadian banks (2024-2025, %)

This strategic conservatism becomes a meaningful advantage in more uncertain cycles.

4. A supportive market environment for Canadian banks

Finally, the stock market performance of the Big Five has also benefited from an external factor. With uncertainty persisting, investors have shifted toward assets offering visibility, yield, and risk control.

Canadian banks have naturally stood out in this context. Their hybrid profile, midway between cyclical stocks and income- generating equities (through high dividends), makes them particularly attractive for investors seeking stability.

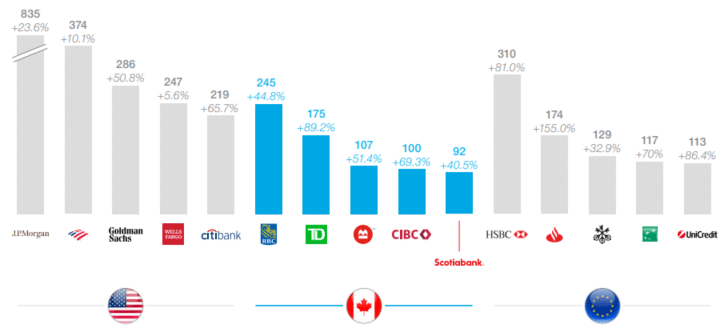

This dynamic is directly reflected in valuations. The market capitalizations of major Canadian banks (even when expressed in U.S. dollars and thus penalized by unfavorable FX effects) have shown remarkably strong and homogeneous increases, consistently exceeding +40% since early 2025. By comparison, in the United States, only Goldman Sachs and Citi show similar trajectories.

Europe offers an interesting contrast. Several major players, particularly those strongly focused on profitability such as Santander or UniCredit, have also delivered strong performances. However, it should be noted that despite a much smaller domestic market, RBC and TD would rank second and third, respectively, in terms of market capitalization in the European landscape.

Market capitalizations of major banks in the U.S., Canada, and Europe as of April 23, 2026, and evolution since January 1, 2025 (USD bn and %)

The outperformance of Canadian banks since 2025 can thus be explained by a rare alignment: a defensive model with more diversified revenues and lower reliance on NII, consistent execution discipline, and a market environment that has, paradoxically, rewarded prudence.

But this phase may be reaching its limits. The Big Five currently hold significant excess capital. With it comes inevitable strategic choices, such as prioritizing shareholder distributions at the risk of capping growth, accelerating initiatives related to transformative acquisitions (as illustrated by ongoing consolidation around National Bank) at the cost of increased risk, or investing heavily in technology (particularly AI) to sustainably transform their operating model.

These options are not mutually exclusive, but they are constrained, both in terms of capital and execution.

Nicolas Darbo – Partner, Accuracy

Michael Craniotakis – Senior Manager, Accuracy

How Canada’s Big Five Banks outperformed the S&P 500 in a challenging environment