More and more experts are discussing the risk of demographic decline and its socio- economic implications. They point to the ticking time bomb of an ageing Chinese population but also the precipitous fall in the birth rates of Western countries, where fertility rates are stalling.

This is a crucial issue because population dynamics frequently serve as the primary driver of market growth in volume.

It is clear that the more a population grows, the more mouths there are to feed, people to clothe and serve, goods to transport, services to provide…

Once again, though this topic may seem straightforward and well-documented, it is essential to examine the figures to capture the reality and assess the scale of this trend. And once the orders of magnitude are established, we must also question the impact of this trend on specific sectors of our economic activity.

PAST AND FUTURE POPULATION TRENDS

Between 1950 and 2024, the world population increased from 2.5 billion to 8.1 billion people.

This corresponds to average annual growth of 1.6%. Two phases can be identified:

- From 1950 to 1990, with average annual growth of 1.9%

- From 1990 to 2024, with average annual growth of 1.3%.

The first key observation is that, while there is a net deceleration in global population growth, the world’s population has still more than trebled over the period.

GROWTH BY CONTINENT

The second key observation is that the geographic split of the population has changed considerably.

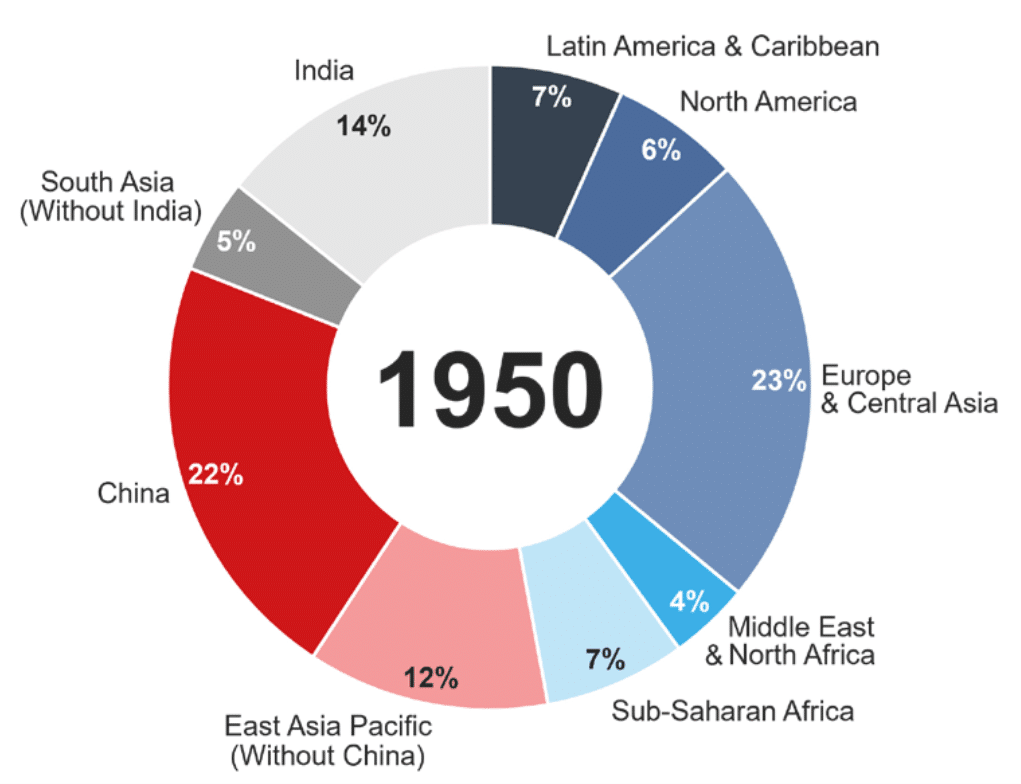

In 1950, Asia accounted for 53% of the global population; Europe and the Americas, 36%; and Africa and the Middle East, 11% (total population of 2.5 billion).

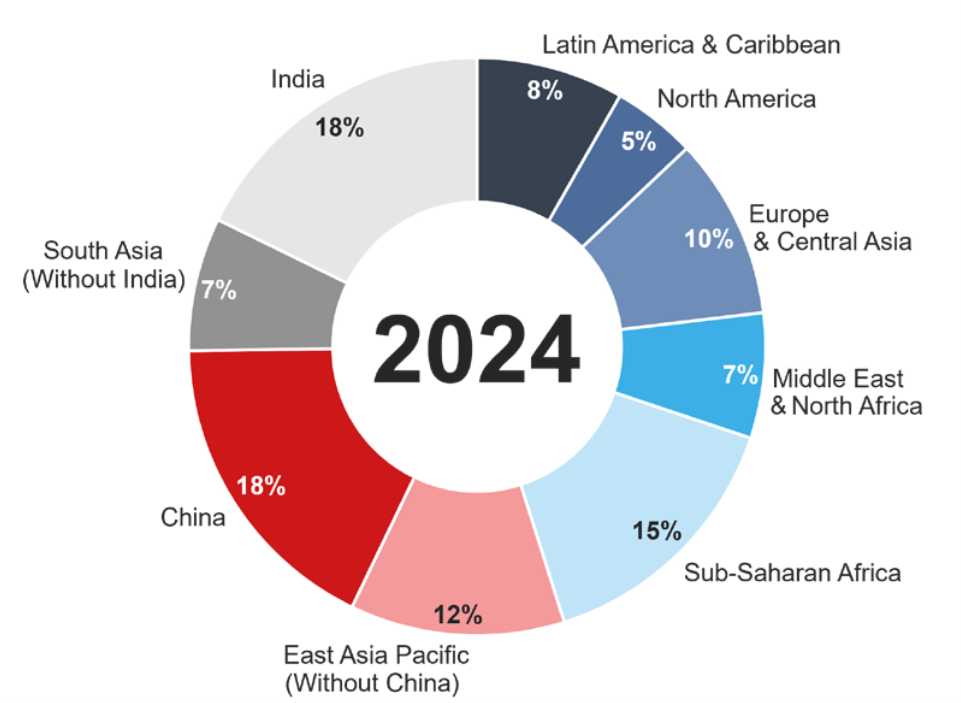

In 2024, Asia made up 55% of the population; Europe and the Americas, 23%; and Africa and the Middle East, 22% (total population of 8.1 billion).

It is worth noting that, in absolute terms, the European and American populations have still doubled, but the African and Middle Eastern populations have increased more than sixfold.

Breakdown of the world population by geographical segment – 1950

Breakdown of the world population by geographical segment – 2024

TWO MAIN DRIVERS OF GROWTH

Following this first set of observations, our primary remark is the explosion in the world population between 1950 and today.

This historical growth has been driven by two complementary factors:

- A high birth rate, exceeding the generational replacement threshold: in 1950, the average fertility rate was 4.9 children per woman, but this has steadily decreased to reach 2.3 children per woman in 2024.

- An increase in average life expectancy, enabled by significant progress in the pharmaceutical industry and in access to healthcare. According to UN statistics, this rose from an average of 46.5 years in 1950 to 73.3 years in 2024.

PROJECTED FUTURE DEVELOPMENT

Our analysis of future global population trends is based on the UN’s central scenario and takes into account the evolution of the two main drivers mentioned above.

Fertility rate

UN demographers predict that the birth rates in 2100 on all continents will be lower than the generational replacement threshold.

The average global fertility rate is estimated to then be 1.8 children per woman.

The last regions to fall under this threshold would be South Asia (2040), Central Asia and North Africa / Middle East (2070) and sub-Saharan African (2100).

Life expectancy

The UN forecasts an average life expectancy in 2050 of 77 years, an increase of 3.7 years compared with the current level.

The projections for 2100 are not explicitly stated, but we understand that the model incorporates slower growth in life expectancy between 2050 and 2100.

On the basis of these assumptions, the world’s population should culminate at around 10.4 billion people between 2080 and 2090, before starting to fall from 2100.

The growth rate by decade would be as follows:

On a global scale, and given humanity’s current impact on the planet, the synthesis of these forecasts seems rather reassuring:

- Global population growth is expected to slow to 0% in 2090.

- The world’s population is expected to peak temporarily at around 10.4 billion and to decline slowly thereafter.

However, there are two major counterpoints to this vision:

- This projection includes a significant ageing of the population: by the second half of the 2070s, the number of people aged 65 and over is projected to reach 2.2 billion, exceeding the number of people under 18 years old.

- Geographically, the dynamics would be much more varied:

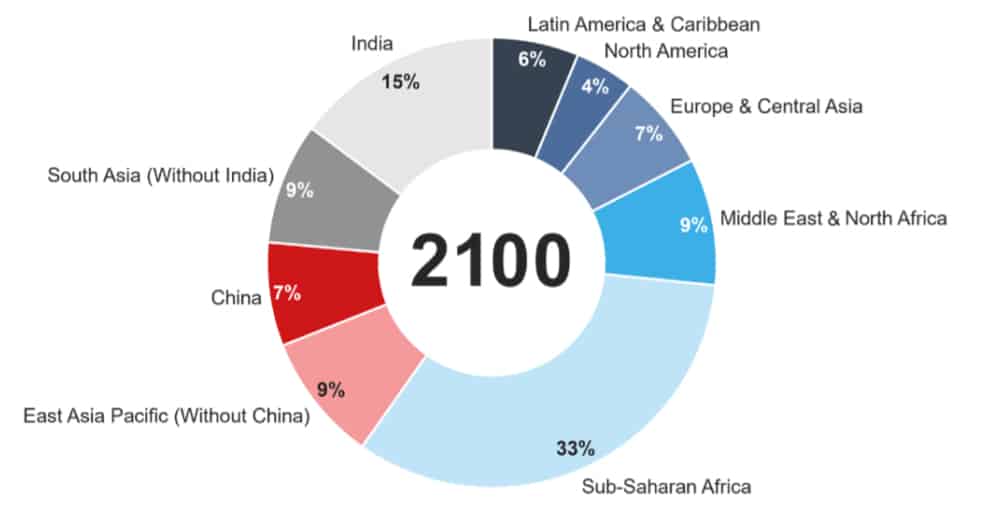

In 2100, Asia would only account for 40% of the population; Europe and the Americas, 17%; and Africa and the Middle East, 43% (total population of 10.4 billion).

In other words (and figures!):

- China’s population will be 45% smaller in 2100 than in 2024.

- Europe’s population will shrink by 13%.

- The population of the Americas will rise by 5%.

- Asia (excluding China) will experience a 13% increase.

- The populations of Africa and the Middle East will grow by +146%.

Breakdown of the world population by geographical segment – 2100

IN SUMMARY

Going beyond preconceived ideas, a detailed review of the UN’s projections sheds light on the issues at hand:

- The demographic challenge for China is critical: the population is set to halve, combined with very marked ageing. A critical issue will be China’s capacity to open up to its neighbouring countries and its policy towards Africa (current policies are geared more towards developing the extraction of raw materials and transport infrastructure than towards urban development and infrastructure dedicated to the population).

- Europe’s population is set to decline and age significantly, but migratory flows from Africa will be able to compensate for the population decline, subject to the capacity of these areas to positively manage African demographic pressure on the African continent and in Europe.

- The Americas will offer by far the greatest demographic resilience over the coming century.

WHAT ARE THE BUSINESS IMPLICATIONS?

These fundamental trends are bound to have major implications for whole swathes of our economies.

We outline below the major challenges for three of them: infrastructure, healthcare and consumer goods (fashion/FMCG).

INFRASTRUCTURE

Future population growth projections highlight the immense need for infrastructure investment in Africa/Middle East and, to a lesser extent, Asia excluding China.

Given that Africa’s infrastructure is lagging behind the rest of the world and that its population is set to increase by a factor of 2.5 by 2100, these infrastructure needs will become imperative if certain societies are not to collapse. Many questions remain unanswered about the financing of this infrastructure and the ability of countries to achieve greater political and economic stability in the decades to come.

Let’s hope that past experience does not foretell the future and that certain innovations will enable countries to truly and definitively emerge. The combination of photovoltaic energy with (i) desalination technologies, (ii) agricultural fertilisation or (iii) the production of green hydrogen seems promising but still far from large-scale implementation. The oil monarchies seem to have grasped the scale of the challenge, but will their investments spread in a healthy and sustainable way across Africa?

And if so, how quickly? On the other side of the spectrum, there are likely to be growing concerns about the conditions and cost of maintaining European and Chinese infrastructure in the face of ageing and declining populations.

The challenge of ageing and shrinking populations in China and Europe is also likely to have a major impact on certain sectors:

- Positive for the pharmaceutical industry

- Mixed for the personal services sector

- Negative for the luxury goods and FMCG industries.

The following analysis provides useful insights into differences in consumption by age group in an economically developed population.

HEALTH SERVICES AND PHARMACEUTICALS

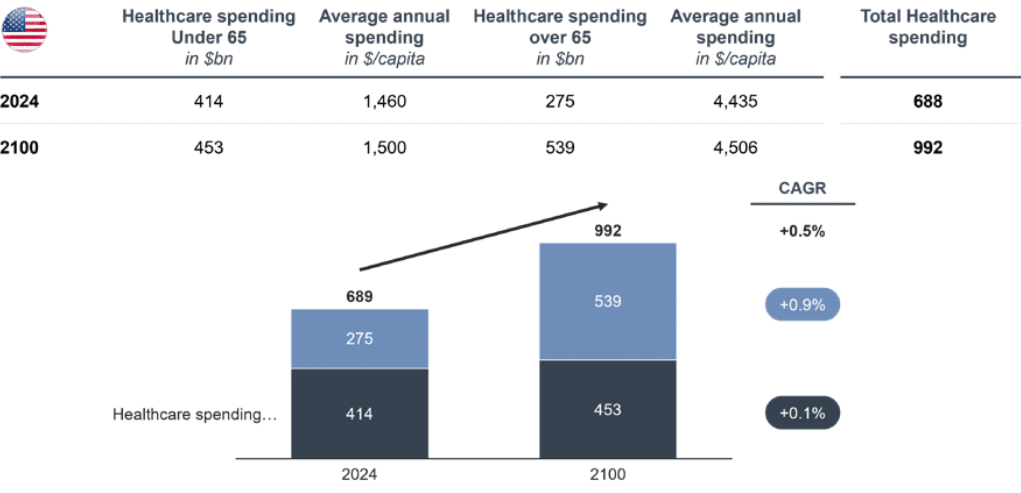

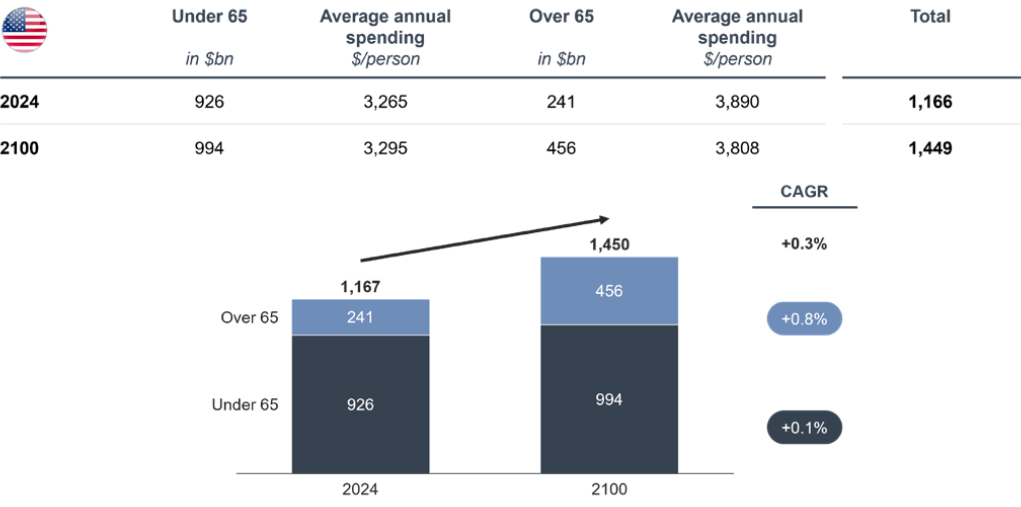

Clearly, healthcare expenditure increases significantly with the age of patients. Ageing populations will therefore have a multiplier effect on the sector, driven by both the number of patients and the average budget per patient. It is also reasonable to assume that constant scientific progress in healthcare will result in a further increase in the resources allocated per patient.

To illustrate this point:

A 70-year-old American patient contributes $4,300 a year to the healthcare sector, compared with $650 a year for a 20-year- old (a factor of 6.6x).

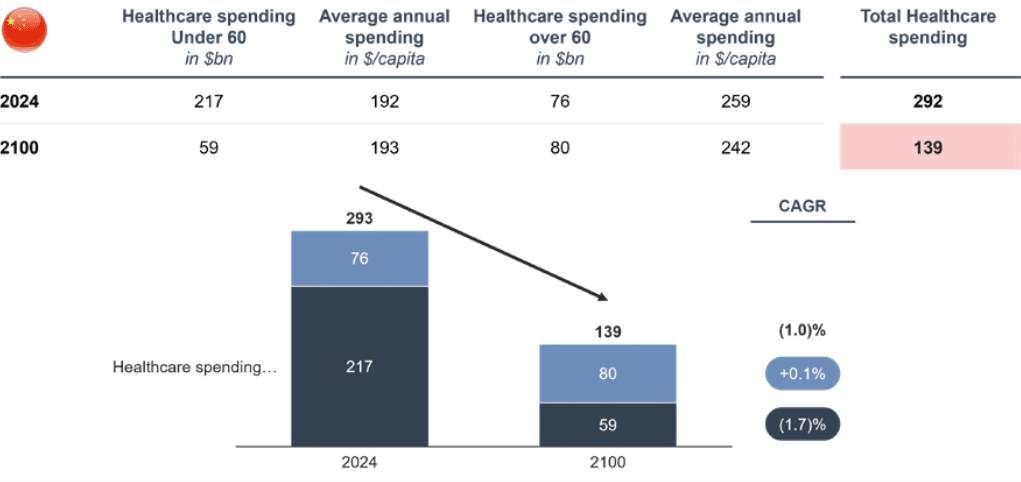

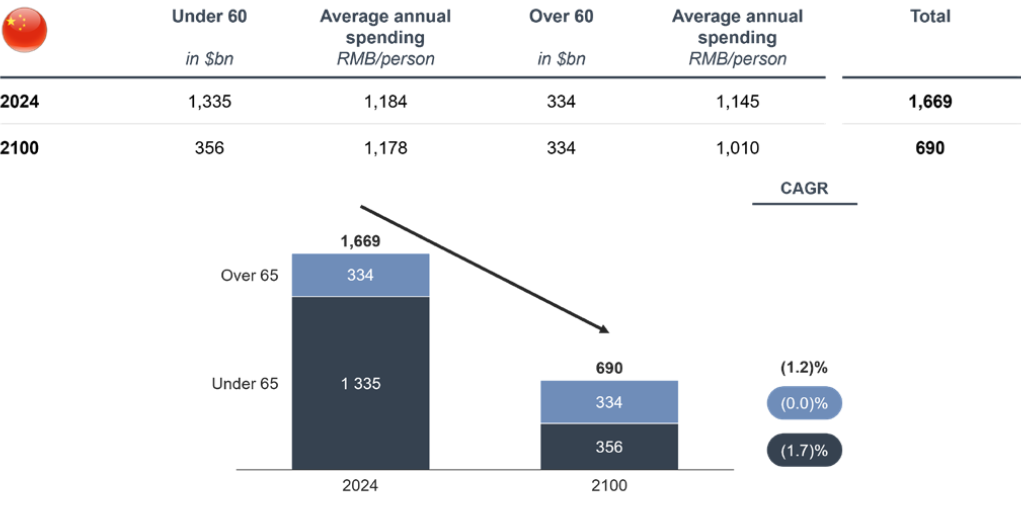

In China, the differences are smaller but still significant. Will they increase as Chinese medicine shifts towards more Western equivalents?

A 70-year-old Chinese patient brings in RMB 2,000 a year for the health sector, compared with RMB 1,100 a year for a 20-year- old (a factor of 1.8x). Over and above the per capita healthcare budget, the sector will face a massive shortage of healthcare staff to assist the elderly, in terms of both medical monitoring and day-to-day assistance. Elon Musk predicts a population of 10 billion humanoid robots by the end of the century. Visionary genius or madness?

Healthcare spending – US

Healthcare spending – China

FASHION AND FMCG

At the opposite end of the spectrum are consumer budgets for fashion items. It is well known that the peak consumption period for this type of item is between the ages of 25 and 50, when people become more conscious of their appearance and begin to have growing and significant purchasing power. Older people, despite having more financial means, are less concerned with their wardrobe and live off their existing stock of clothes.

- American consumers aged between 45 and 54 spend an average of $837 a year on fashion items, compared with $611 for those aged between 65 and 74, and $481 for those over 75.

- Chinese consumers aged 30 spend an average of RMB 1,200 a year on fashion items, compared with RMB 500 for those aged 75 and over.

The ageing of the population will therefore act as a double burden for this economic sector, with fewer young, high-spending consumers and more older consumers who are less responsive to this category.

Clothing spending – US

Clothing spending – US

We have just briefly analysed the potential impacts for three sectors of activity, and it is clear that they will be significant.

In reality, every sector of activity will be massively affected.

In the best-case scenario, this will mean significantly adapting the business model, with a major distortion of the geographical mix, a shift in value from one age group to another, and a rethink of targeting levers and business models.

In more complex cases (e.g. infrastructure in Africa, healthcare in ageing countries, asset management and pension systems), it will mean starting from scratch.

Demographic statistics are known for their resilience. Decision-makers and investors will not be able to say they didn’t know…

Jean-François Partiot – Partner, Accuracy / Léa Bocquillon – Consultant, Accuracy

Accuracy Talks Straight #12 – Industry insight