What is demography?

One answer, both rigorous and simple, could be as follows: the quantitative study of human populations and their dynamics, based on the components of fertility, lifestyles, migration, ageing and mortality. A vox pop experiment in France today would probably result in a different view, with a declining birth rate, an ageing population and concerns about large inflows of migrants. With this in mind, it is hard not to be tempted to draw two “common sense” conclusions: the economic dynamic can only weaken, and the country risks “losing its soul”.

So, where do the major demographic trends stand, and what are their links with the economy? Let’s take a look at high-income countries (according to the World Bank, these have a gross national income per capita of over USD 13,845 – figures for 2022; at the bottom of the ranking, Chile is at just over 15,000, and at the top, Switzerland is at over 95,000; for information, the United States is at 77,000 and France at 45,000).

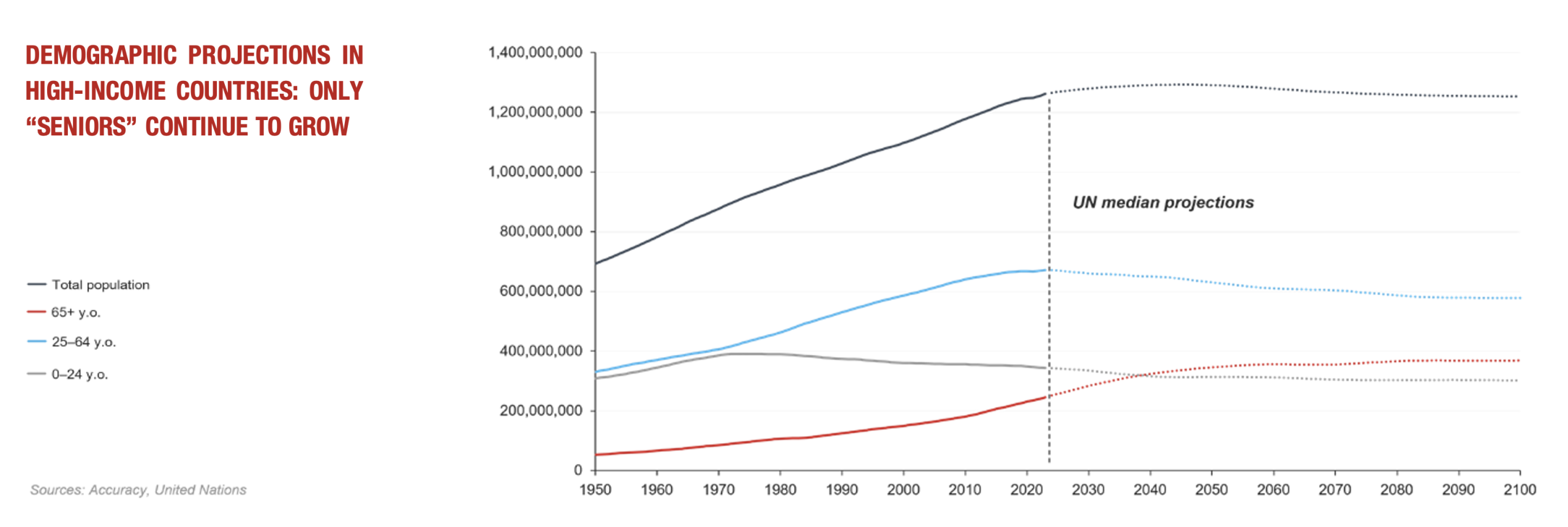

The total population of the group was 1.26 billion in 2023, compared with 693 million in 1950 (by comparison, the respective levels for the world are 8.16 billion and 2.49 billion). According to the United Nations median scenario, a peak of 1.29 billion people would be reached in 2038, and in 2100, there would be 1.25 billion people (for the world as a whole, the peak would be reached in 2081 at 10.29 billion, before dropping to 10.18 billion in 2100).

For these high-income countries, the number of inhabitants hardly increases from now on. A major shift is even taking place before our very eyes: the 25–64 age group peaks in 2023 at 671 million. Its size is now shrinking and is expected to be just 578 million by 2100. In fact, the only group that is now expanding is the 65+ age group; the under-25s have been declining since 1973.

Fewer adults and fewer young people – that is not a good message when it comes to the outlook for the working-age population! Nevertheless, we should bear in mind that worldwide trends are more favourable.

The 25–64 age group should continue to grow until 2070 (5 billion compared with 4 billion today), largely offsetting the slow decline in the under-25 age group (3.15 billion in 2070 compared with 3.28 billion in 2023). That said, the 65+ age group is also growing in size.

Let’s focus a little more on the high-income countries and try to gauge the extent of this dual movement: a small increase in the total population (+2.3% between now and 2038, or +0.15% per year) and a slight fall in the working-age population (-2.9% over 15 years, or-0.2% as an annual average). What will the impact on global growth be? Economic analysis is based on the idea that, over the long term, the pace of growth depends on the importance of the factors of production used (traditionally, capital and labour) and their efficiency (the productivity of each of them).

The macroeconomic breakdown most often takes the form of the following equation: change (%) in GDP = change in hours worked (%) + change in hourly labour productivity (%).

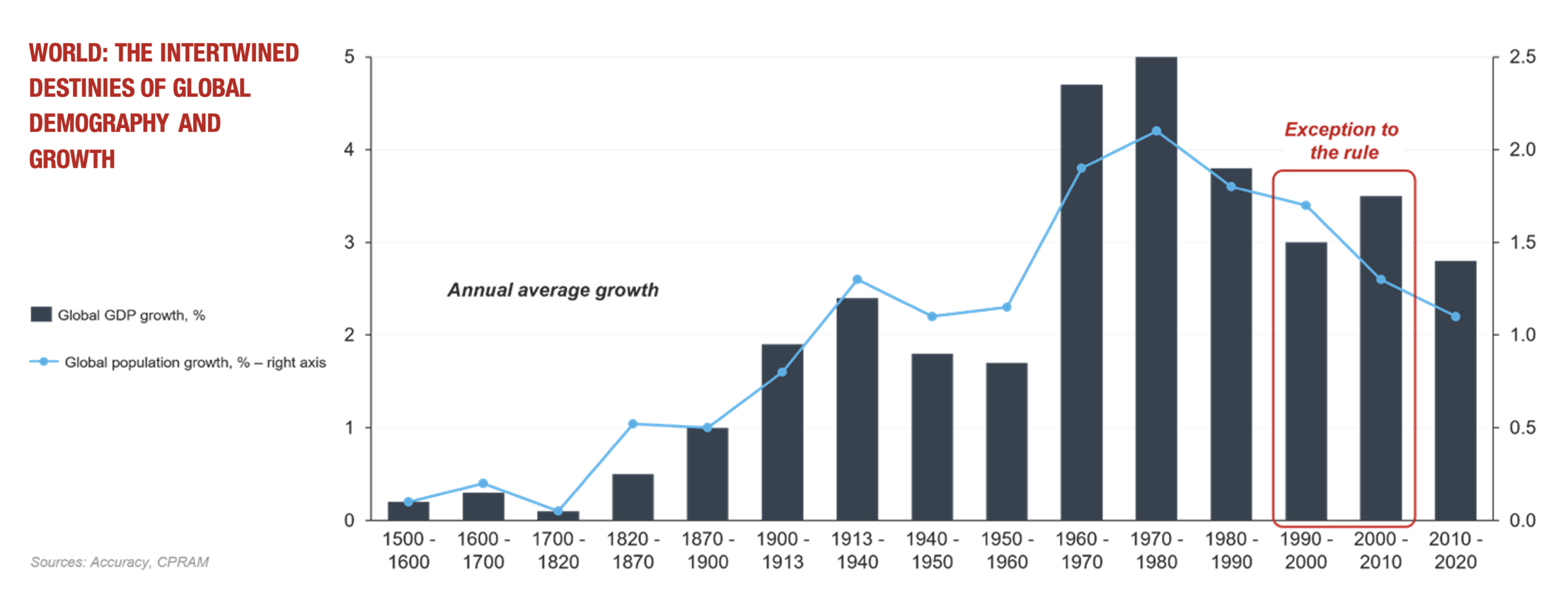

We should bear in mind that the number of hours worked depends on both the workforce employed and the average working time. Although not direct, there is a relationship between economic growth and population growth. Over a very long period and at the global level, the ratio is more or less the same, at 2 (the economy) to 1 (the population). Thanks to the miracle of productivity, 1 percentage point of population growth contributes 2 percentage points of economic growth.

A more dynamic demography would then encourage higher productivity gains and therefore even more growth. The explanation lies in producers’ expectations. Perceived structurally higher final household demand prompts investment projects to be scaled up. As is often the case, capacity and productivity are linked. But beware of the reversible nature of the relationship: lower anticipated demand, for demographic reasons, reduces investment decisions. Productivity performs less well and the slowdown in economic growth may be more marked than that of the population.

There are exceptions to this “iron law”. On a global scale, between the decades starting in 1990 and 2000, the population growth rate slowed (from +1.7% per year to +1.3%), yet economic growth accelerated (from +3.0% to +3.5%). The opening up of China’s economy to the rest of the world and the internet revolution boosted business expectations, investment and, ultimately, productivity.

Today, the dual prospect of a slowing population and weaker economic growth has the makings of an unacceptable scenario. How can we simultaneously accelerate the energy transition, effectively combat climate change, ensure the necessary defence efforts in a more dangerous world, manage demographic ageing, and cope with the financial burden of rising debt, all with even less economic growth?

What can be done? Certainly, we must look to replicate the first decade of this century! On the demand side, finding an economy of China’s scale that is opening up to the world again is no easy task. But how can ignore what the UN is telling us? By 2050, while the population of North America and Europe combined will stagnate, that of Africa is projected to increase by two-thirds (to almost 2.5 billion). Its development is key; for Africa… and for the entire world!

On the supply side, there are three levers to pull. First, there is productivity. The challenge is to ensure that it does not slow down or, better yet, that it increases. Will the emergence and spread of new technologies make this possible? Then there is the activity rate of the existing population. This means increasing the number of working-age people engaged in professional activity, shifting the balance between work and personal life more in favour of the former, and fostering greater talent development (better lifelong learning and opportunities that are more widely open to all groups in society). There is no denying that implementing such reforms will be complicated in many countries. Finally, there remains the even greater challenge of attracting more workers from more demographically dynamic regions of the world (primarily Africa, but also Asia – mainly South Asia, Southeast Asia and the Middle East). Labour shortages and the lack of interest in certain professions push in this direction, but political debates remain a strong barrier. This can only be overcome if the process is well managed, with the conviction that integration will succeed. How can we reassure increasingly sceptical populations? Or, to put it another way, how can we ensure that economics and politics work together in harmony?

Hervé Goulletquer – Senior Economic Adviser, Accuracy

Accuracy Talks Straight #12 – Economic point of view