In recent years, and particularly in the wake of the Covid-19 health crisis, the issue of reindustrialisation has taken centre stage. While industrial policy has historically been seen as an aberration because it runs counter to free competition, increasing public intervention in the industrial sector is a tangible reality.

There are many reasons for this: creating skilled, well- paid jobs, improving the balance of trade, investing in the technologies of the future and ensuring “France’s independence and sovereignty”, according to the French president in his speech on 11 May 2023 dedicated to reindustrialisation.

FROM DEINDUSTRIALISATION TO THE REHABILITATION OF INDUSTRIAL POLICY

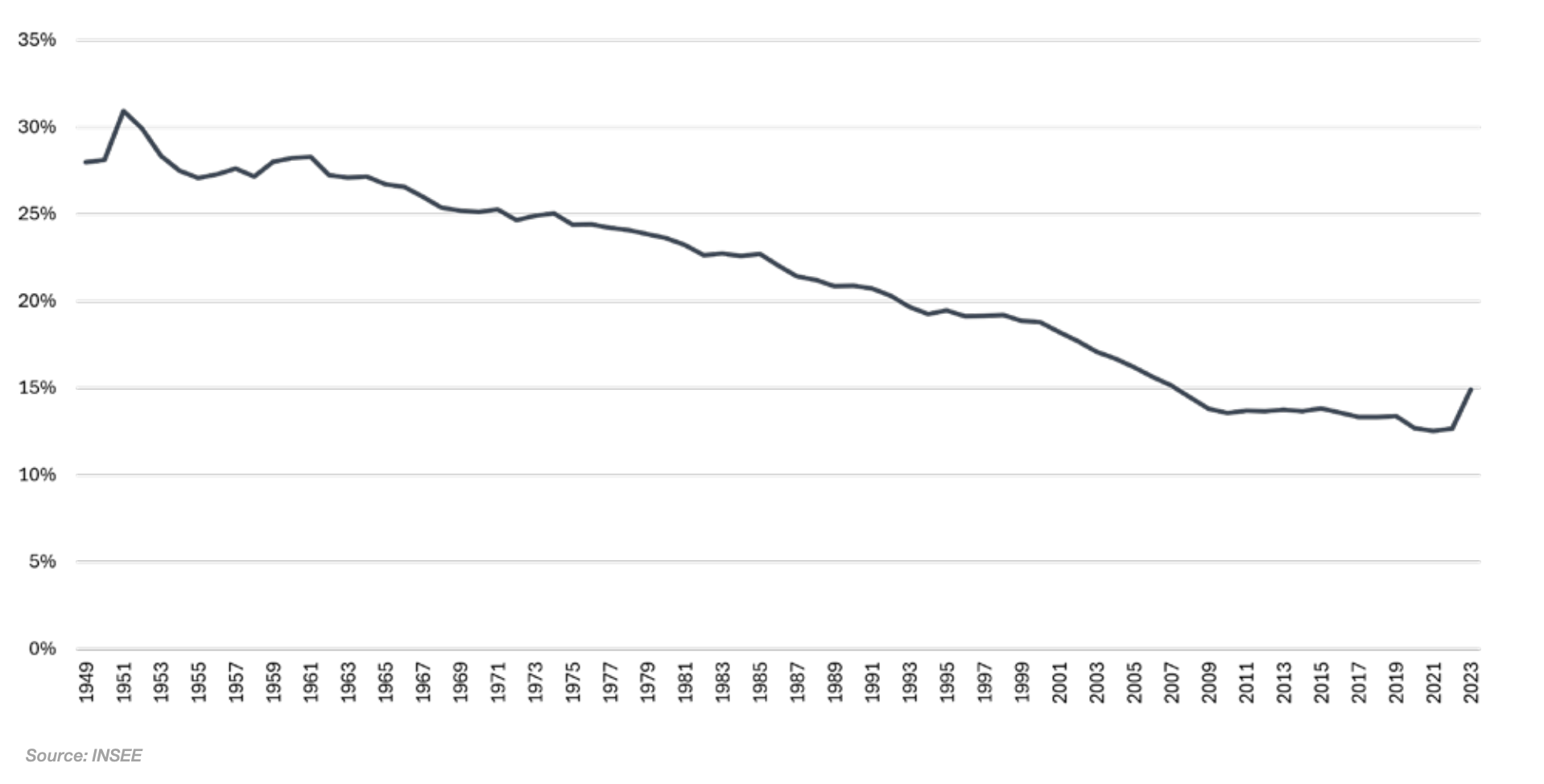

In fact, France has largely deindustrialised its economy, with services becoming the most important economic sector (almost 70% of GDP for market and non-market services in 2023). The adjacent graph shows the evolution of value- added in industry as a proportion of total GDP.

Change in the share of industrial value-added in GDP between 1949 and 2023

While deindustrialisation has been continuous since the end of the Second World War, it accelerated in the early 2000s, with industry now accounting for just over 10% of GDP, compared with almost 30% until the 1960s. Moreover, although this downward trend is consistent with that observed in many European countries, it was twice as strong as elsewhere. The reason put forward is poor positioning in terms of cost competitiveness, linked to the higher labour costs and corporate taxes in France compared with her neighbours.1

Today, France is just a few percentage points behind Germany and Italy, and close to, if slightly higher than, the United Kingdom and the United States.

An economic theory can be used to describe the downward trend in the share of industry: the smile curve.

Popularised by the founder of Acer, Stan Shih, it postulates that most of the added value created by an industrial firm is located upstream (research and development – R&D) and downstream (marketing, sales, associated services) of the production process, so that physical production is only a very marginal part of the value of a good.

In this context, the smile curve underpins a certain geography of productive choices: productive efficiency means taking advantage of the opportunities offered by globalisation and choosing to produce in countries where labour costs are as low as possible. This often means keeping services close to the end customer, but also sometimes manufacturing geographically far from the point of sale, within global value chains.

Covid-19 has partially challenged this paradigm, considering that, even if the added value of production is not high, geographical proximity has a strategic value. For example, the shortage of surgical masks during the pandemic revealed the risks of the location choices associated with the smile curve. The dilemma is thus clear: choose to reindustrialise to secure supply but accept to pay more for the end product.

DEFENCE AS AN EXAMPLE OF SUCCESSFUL PUBLIC POLICY

For reasons linked to minimising external dependency, in the defence sector, France prefers to supervise the value chain to ensure that its defence industry is capable of producing the major equipment required by France’s armed forces.

Defence procurement choices can therefore serve as a point of reflection for the reindustrialisation drive.

Historically, arms production in France has been linked to state arsenals. These were responsible for the development, production and maintenance of the equipment, with a view to controlling the entire value chain. France’s Gaullist ambition is one of strategic autonomy: not to be dependent, including on allies, when it comes to the central elements of defence policy.

This is particularly the case for nuclear deterrence, where 99% of the industrial prime contractor’s purchases are made in France.2

Since the end of the Cold War, France’s industrial base has been transformed to become more efficient, while maintaining an objective of independence in critical areas (R&D, final production). The business model is largely based on substantial public investment to finance the development and production of weapons systems.

This investment, although cyclical, was not called into question at the end of the Cold War, unlike in other European countries. As a result, French industry is now one of the most efficient in the world.

In addition to public orders, exports are the other component of the defence industry’s business model, accounting for around 25% of total sales.

Moreover, minimising dependency leads to a reduced volume of imports, resulting in a coverage ratio exceeding 4 over the past ten years.

Today, with over 200,000 jobs, the French defence industry represents a major sector (almost 6% of total industry). Further, 25% of the country’s R&D potential is concentrated in the aerospace and defence sector3, which has a positive macroeconomic impact.4

THE CHALLENGES OF DEFENCE REINDUSTRIALISATION

However, despite strong regulation, continued political will and substantial investment, the French defence industry faces major challenges.

The first is to guarantee technological continuity by investing in future programmes that will be in service in the decades to come. This is a major ambition of the recent loi de programmation militaire (LPM – Military Planning Act), covering the period 2024–2030, which safeguards R&D spending on the successors to the nuclear deterrent delivery systems.

The second challenge is to increase production rates because, with the increase in international tensions and conflicts since 2022, demand for French defence products is growing strongly, especially in the artillery, munitions and missile sectors. There are a number of bottlenecks (difficulty in recruiting and uncertain responsiveness of the subcontracting chain), which means that, despite a full order book, production volumes are only increasing slightly.5

One case of reindustrialisation in the defence sector is emblematic: the relocation of gunpowder production to Bergerac with the Eurenco company. This company, heir to the arsenals and the result of consolidation with European players, benefits from very strong demand for chemical products, including gunpowder for large-calibre ammunition. In less than a year, the investments made by Eurenco enabled it to relocate a large part of its production, automate its production processes and thus increase the output of the final product.

This example confirms that the ambition to reindustrialise requires a combination of political will, which is not necessarily financial, a vision of the business model over the medium and long term, and an analysis of the strategic nature of production.

1 France Stratégie (2020), Les politiques industrielles en France, Évolutions et comparaisons internationales, Report for the National Assembly

2 H. Masson (2017), Impact économique de la filière industrielle, composante océanique de la dissuasion, Recherches & documents de la FRS, n°01/2017

3 S. Moura and J.-M. Oudot (2017), Performances of the defence industrial base: the role of small and medium enterprises, Defence and Peace Economics, 28(6), 652-668

4 E. Moretti, C. Steinwender and J. Van Reenen (2025), The intellectual spoils of war? Defense R&D, productivity and international spillovers, Review of Economics and Statistics, 107(1), 14-27

5 J. Droff and J. Malizard (2024), Pourquoi nous ne sommes pas (encore) en économie de guerre ?, The conversation

Julien Malizard – Chair in Defence Economics – IHEDN

Accuracy Talks Straight #12 – The academic insight