To construct or to build? The two verbs seem interchangeable, yet their etymology reveals a subtle distinction. The former comes from the Latin construere, meaning ‘to pile up in layers’ – a notion that suggests order. The latter has its roots in Proto-Germanic languages: bastijan meant ‘to mend’ and, by extension, ‘to patch up or assemble’. Its contemporary German descendant is bauen, and historically Bauer did mean both builder and farmer. Perhaps, then, there is more ambition in constructing than in simply building.

Most economists would agree with this hierarchy. In France, INSEE (the national statistics service) splits the construction sector into four branches: specialised construction trades (69% of added value in 2023; responsible for making structures functional), civil engineering (17%), building construction (8%) and property development (6%).

With this in mind, perhaps in the famous French saying ‘quand le bâtiment va bien, tout va bien’ (when building thrives, everything thrives), the word ‘bâtiment’ should be changed to ‘construction’? Probably. But before considering whether this adage still holds true, it is worth looking at its origins, if only to note yet another layer of confusion. The quote is attributed to Martin Nadaud, a 19th-century stonemason who became a member of parliament and prefect, largely thanks to many years of diligent work during evening classes. According to Jean-Marc Daniel, emeritus professor at ESCP Business School, Nadaud’s actual words were, ‘Quand le bateau va bien, quand le bateau va loin, tout va bien’ (when the boat goes well, when the boat goes far, everything goes well). It was Baron Haussmann who took up the idea and gave it the wording that has become popular today. Of course, in French, a bâtiment (building) can refer to a bateau (boat), just like it can be a house, a block of flats or a warehouse. Nevertheless, a shipyard wouldn’t be included in the construction sector, even though we do talk of shipbuilding (and also naval architecture)!

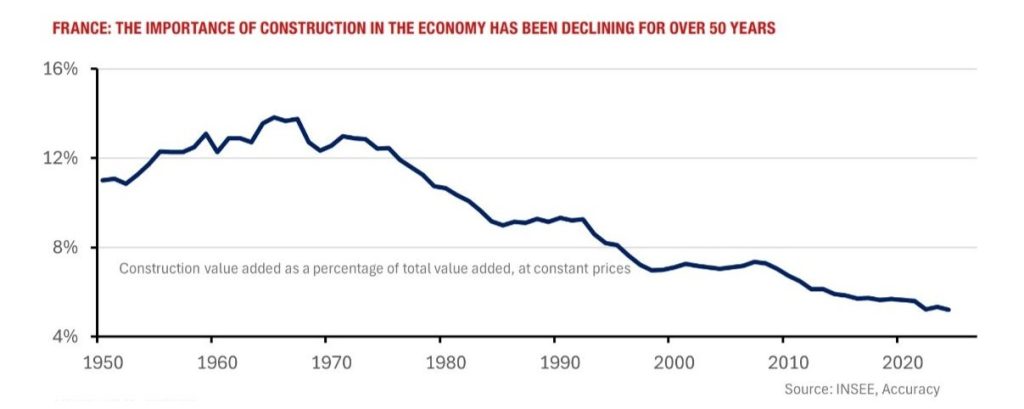

One observation is clear: the relevance of the proverb appears to have diminished over time. This is simply because construction’s share of total value added has declined steadily over the last few decades.

France provides a telling example. The sector accounted for 11% of total value added in 1950 and 13% in 1971 (its peak), before beginning a sharp decline to just over 5% today. In the same way as we speak of the deindustrialisation of France, perhaps we should also speak of its deconstruction. Undoubtedly – but there is a caveat. If we look not at value added but at production – that is to say, if we include the intermediate consumption necessary to generate output (as a reminder, value added = production – intermediate consumption) – the decline from the early 1970s until now is slightly less marked: the relative weight of construction falls from 14% to 7%.

This increase in intermediate consumption means that, over time, construction professionals have become more like assemblers of components produced by industry, representing a transfer of activity, albeit partial, from construction to manufacturing. Even so, it must be acknowledged that construction has grown more slowly than the economy as a whole. And because of that relative sluggishness, overall economic momentum has been weaker, all else being equal. Is this enough to invalidate the proverb? Not entirely, for two reasons.

Firstly, the economy is not just about trends; it is also about momentum. This can strengthen or weaken, rise or fall. Such shifts, consisting of inflection points and reversals, shape the economic cycle. Almost all components of the economy play a part. Let’s take prices, for instance: their rise can initially stimulate growth (buy today what will cost more tomorrow), then depress it (inflation first nibbles away at purchasing power before devouring it if it accelerates uncontrollably). Households and businesses also adjust their demand behaviour. Greater confidence encourages forward-looking decisions, leading to investment in equipment, intangible assets and, yes, construction, while declining confidence produces the opposite effect.

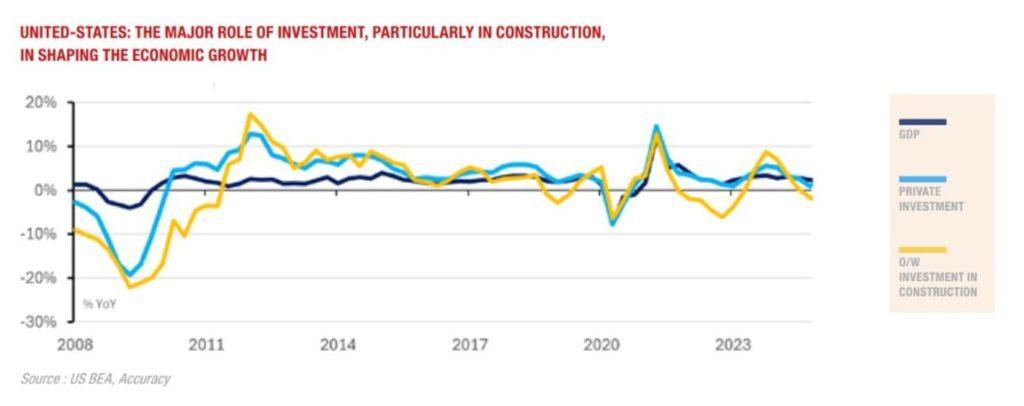

Finally, there is economic policy: monetary policy in particular, including interest rate management, which influences supply and capital-market conditions, which in turn shape investment choices. Ultimately, the relationship between investment, particularly its construction component, and overall economic activity is both proven and persistent. The United States and France illustrate this quite convincingly.

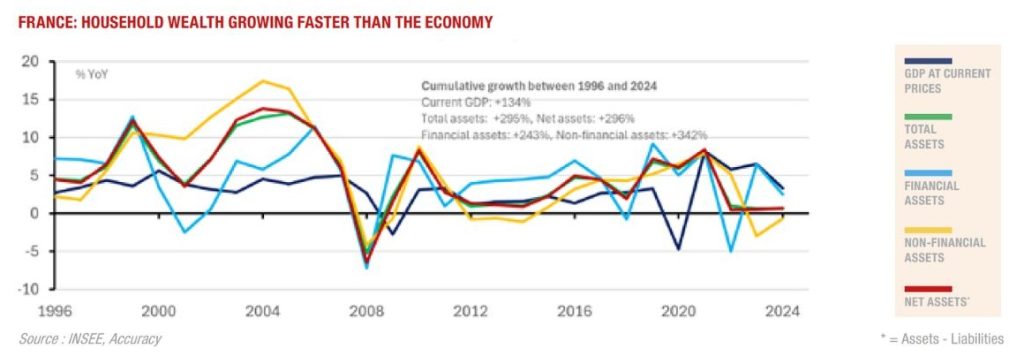

Secondly, the economy is not driven solely by flows. Stocks play an important role too, via the process of appreciation and depreciation. Economists refer to this as the wealth effect: households tend to spend more as their assets increase in value (and vice versa). In France, household wealth has risen faster than GDP. Over the past 30 years or so (1996 – 2024), while nominal GDP grew by 134%, French households’ assets increased at more than twice that pace.

Their total value reached nearly €17 trillion in 2024, compared with a GDP of around €3 trillion. More specifically, three developments stand out:

- A 342% increase in non-financial assets (mainly construction – in fact, housing – and land), reaching €9.9 trillion in 2024

- A 243% increase in financial assets (to €7.0 trillion)

- After accounting for debt, net household wealth stood at €14.8 trillion in 2024, representing growth of 296% since 1996.

This increase is primarily the result of two effects: one related to flows (saving efforts) and one related to prices. Between 1995 and 2023, the net financial wealth of French households more than tripled (x3.4), with flows contributing over 50% and price effects nearly 40%. For non-financial assets, this division of roles is more difficult to determine, but considering real estate alone, price effects appear predominant.

Construction is therefore a major component of household – and national – wealth. Over the long term, its value tends to rise, enriching owners. While the link with changes in demand is neither direct nor linear, this wealth accumulation phenomenon acts as a sort of reserve that can be drawn upon in hard times.

From both a cyclical and structural perspective, we can reasonably defend the idea that ‘when building thrives, things may not be so bad after all’!

Hervé Goulletquer - Conseiller économique principal, Accuracy

Accuracy Talks Straight #15 – Economic point of view