It is no easy task for Europe to confront the image reflected back at it in the mirror held up by the United States. Does it not show an economy falling behind, struggling to hold its rank among the world’s major powers, and hinting at civilisational decline?

From an economic perspective, a long‑term comparison of GDP per capita, expressed simply in the dollar and at current prices, leads to a stark conclusion: the European Union accounted for 65% of US GDP per capita in 1990, and barely more than 50% in 2024. The conclusion seems unambiguous. But appearances can mislead. When GDP is adjusted for inflation and cost‑de‑living differences, the divergence nearly disappears: from 65% to 63%. A gap remains, but one that has not widened significantly. Europeans’ societal choice to work fewer hours, combined with lower productivity, largely explains it. This reassuring sense of “nothing new under the sun” may nevertheless be deceptive. First, the apparent stability masks two opposing trends: a relative slowdown in core EU countries, and their partial catch‑up by newer member states. But is this catch‑up process not bound to run out of steam? Second, Europe’s economic momentum has been weaker for some time, across productivity, investment, R&D and the adoption of new technologies. Less fluid social organisation also acts as a brake, as does the collective preference for shorter working hours.

In international relations, the EU (both its institutions and its member states) struggles to exert influence. It is as if its considerable economic weight were no longer enough. Yet that weight is comparable to China’s and far exceeds that of India (by a factor of almost five), Russia (seven) or Brazil (nine). In an increasingly Westphalian world – a reference to the Peace of Westphalia in 1648, which brought the Thirty Years’ War to an end, signifying also the end of religious unity in Europe (cujus regio, ejus religio) and which, one might argue, affirmed the power of nation states – Europe’s political power remains insufficient, particularly in foreign and defence policy, with the latter now conditioning the former. EU defence spending reached $342bn in 2024 (European Commission data), comparable to China’s ($314bn, SIPRI), well above Russia’s (around $149bn), but far below US spending ($997bn). Numbers alone, however, do not tell the full story. The lack of coherence between national defence policies, despite most countries being NATO members, likely reduces the operational return on this spending and perpetuates dependence on the US military. This has clear repercussions for foreign policy. The Trump administration has imposed decidedly unequal trade agreements on Europe, and Washington’s neo‑isolationist drift has encouraged Russia to pursue invasions of its neighbours, without excessive fear of Western retaliation. This insufficient mastery of the attributes of power ultimately disqualifies Europe in the eyes of a US government that prefers bilateral relations with member states over engagement with EU institutions. Europe cannot credibly claim a seat at the table in the new Concert of Nations; instead, it risks being relegated to the US sphere of influence.

On the civilisational front, the White House’s critique of Europe is severe. Environmental priorities are said to weaken the economy; immigration allegedly strains social cohesion; post‑modernism, seen as a precursor to wokism, is accused of undermining Western political culture by elevating minority viewpoints over consensus and threatening free expression. Civilisational decline is deemed inevitable unless Europe follows the path charted by the Trump administration.

There is broad agreement that Europe must regain its footing, but almost certainly not by following the American prescription, even if they may not like it.

Everything starts with the economy. Quite simply because economic success is a necessary condition for geopolitical influence and for the internal reforms the EU must undertake. As the rules of the global economic game change, Europe has a duty to adapt. It has done so before, most notably during the decades when neoliberal regulation translated into freer trade, more open markets, stronger multilateral rules and a transfer of power from nation states to so‑called independent agencies (competition authorities, central banks). Today, by contrast, in an international environment that has become more fragile and uncertain, the state is making a comeback. This is evident both in industrial policy, aimed at steering economic activity, and in the coercive defence of national interests wherever necessary across the globe.

Since the Draghi and Letta reports, both published in 2024, a broad consensus has emerged on what needs to be done. Three levers stand out: the single market, technology and joint borrowing. Nearly forty years after the Single European Act, the single market is still incomplete. An ECB study published in 2025 estimated that remaining frictions were equivalent to tariffs of up to 67% for goods and 95% for services. If internal barriers were reduced to US levels, IMF estimates suggest that labour productivity could rise by almost 7% over seven years. Europe must also re‑engage decisively in the race for critical technologies. Failure to do so would result in excessive dependence on China and the United States. The sums involved, whether for investment or R&D, are vast and cannot be mobilised by individual member states acting alone. European‑level pooling is unavoidable. There is therefore little alternative: major joint investment projects must be financed collectively. Common debt thus becomes an ardent obligation.

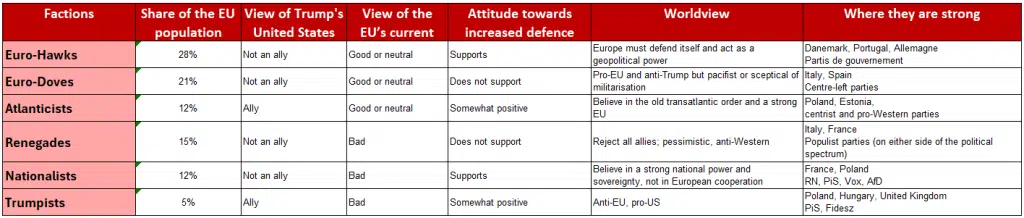

It then falls to European politics to make these necessary initiatives possible. Drawing on a recent ECFR study (European Council on Foreign Relations, The European Archipelago: Building Bridges In A Post-Western Europe¹, February 2026), public opinion can be segmented into the following broad categories: “Euro-hawks” (28% of Europeans): pro‑EU, critical of the United States, supportive of increased defence spending; “Euro-doves” (21%): pro‑EU but reluctant to raise military budgets; “Renegades” (15%): hostile to both the US and the EU, opposed to higher defence spending; “Atlanticists” (12%): broadly pro‑EU but primarily aligned with the US, in favour of higher defence spending; “Nationalists” (12%): critical of both the US and the EU, but supportive of military spending; “Trumpists” (5%): eurosceptic, pro‑US, advocating higher defence budgets.

[1] The sample of countries taken into account includes the United Kingdom and Switzerland.

The views of the various schools of thought within the European Union

Source: ECFR, Policy Brief, February 2026

How can a majority coalition be built? It is a matter of arithmetic, convictions… and movement. Assuming that Renegades, Nationalists and Trumpists will not play a constructive role, the core bloc consists of Euro‑hawks (28%), Euro‑doves (21%) and Atlanticists (12%). The first must become less hostile to the US; the second must accept defence‑related budget trade‑offs; and the third must recognise that European success requires greater strategic distance from Washington. Compromises will be unavoidable. Progress may not be easy. If consensus among all 27 proves impossible, an avant‑garde group, provided it is sufficiently large, may need to lead the way, paving a path others will eventually follow.

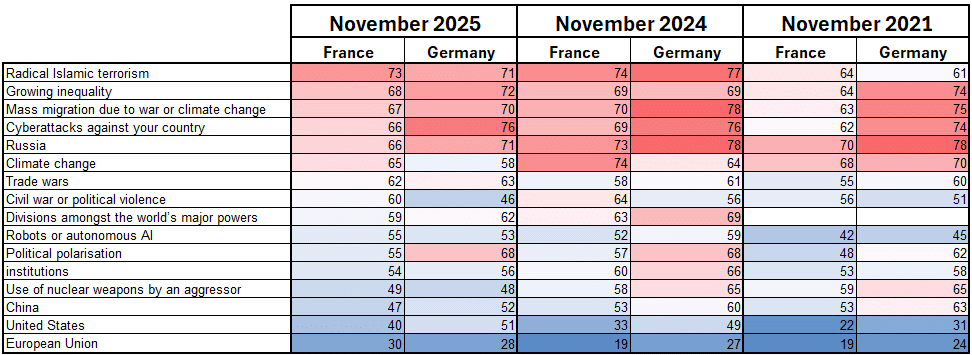

This brings us to the crucial question: can a Franco‑German initiative carry the majority of member states in this deep reform agenda? Two underlying realities stand out: first, public opinion in France and Germany shares a common view of current threats and broadly compatible visions for Europe’s future; second, their economic performances diverge significantly.

On perception, convergence is clear. The Germans and the French largely agree on both allies and adversaries. It follows that their European projects should align closely. They do, but not completely. In both countries, a coalition of Euro‑hawks, Euro‑doves and Atlanticists forms the majority. Yet in Germany, this majority is comfortable (58%: 33%, 17% and 8% respectively); in France, it is marginal (51%: 26%, 18% and 7%). In fact, eurosceptic groups, whether Renegades, Nationalists or Trumpists, and the politically unaligned, carry more weight in France than in Germany (respectively 39% and 10% versus 35% and 7%). Around 53% of Germans who support the ruling coalition identify as Euro-hawks. In France, that figure is almost 10 percentage points lower.

What are the issues of greatest concern to the French and Germans?

Source : Munich Security Conference, Munich Security Report 2022, 2025 and 2026

Note : each figure represents the percentage of people who believe that a particular issue poses an imminent risk to their country

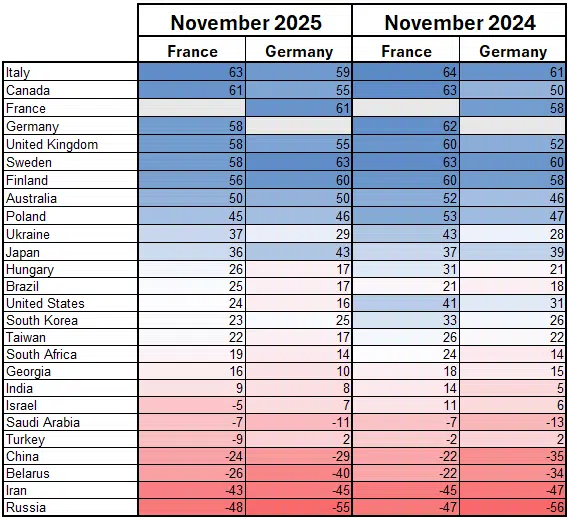

Who do the citizens of France and Germany consider to be their allies or adversaries?

Source : Munich Security Conference, Munich Security Report 2025 and 2026

Note : each figure represents the difference between the number of people who consider the country in question to be an ally and those who consider it to be an adversary

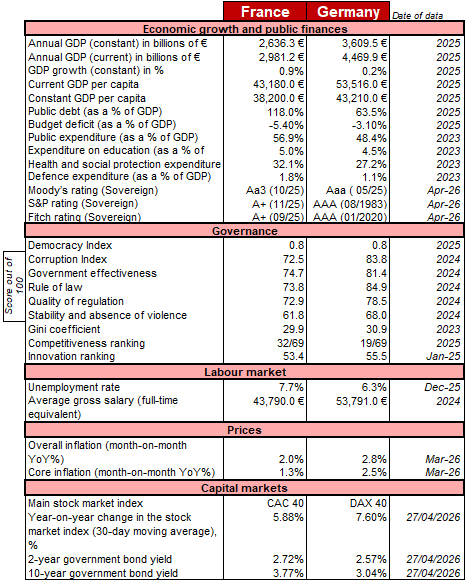

Economic fundamentals diverge more clearly – and to Germany’s advantage, with France often lagging behind, though this assessment should be tempered by Germany’s recent growth struggles. Between 2022 and 2025, German GDP contracted by an average of 0.4% per year, while French GDP grew by 1.2%. A less open global economy, particularly in China and the US, and the loss of access to cheap Russian energy have forced Germany to rethink its economic model. This transition is costly and time‑consuming. Even so, Berlin’s economic and financial position remains stronger than Paris’s. Germany has the means to finance the building blocks of a European renaissance largely from its own resources. France, by contrast, cannot avoid relying on European‑level funding, a mechanism Germany has traditionally been reluctant to embrace.

A more favourable picture of the economy on the German side

Source : Accuracy, Macrobond, Eurostat, IMD

How, then, can France and Germany move forward together? Convergence is needed in crucial areas such as defence (Germany’s emphasis on “responsibility” versus France’s on “autonomy”, with potentially a much higher increase in military spending east of the Rhine than west) and European governance (fiscal discipline and revised objectives for Berlin, versus an expanded, more autonomous EU budget for Paris). Reciprocal commitments will be essential. France must restore order to its public finances quickly, durably and credibly. Germany must agree to develop its attributes of power within a European framework. Is this feasible? More precisely, will political balances on both sides of the Rhine allow it?

Hervé Goulletquer, conseiller économique principal, Accuracy