Chinese players’ expansion into the European automotive industry reflects a strategy of gradual integration into existing ecosystems. Targeted acquisitions, structuring partnerships, and industrial investments enable a durable anchoring within value chains, providing direct access to capabilities, industrial networks, and end markets. This dynamic follows a long-term logic, where each initiative contributes to a coherent accumulation of capabilities.

The structuring of the industry is increasingly driven by technical standards and technological architectures. Choices related to batteries, charging protocols, connectivity, and embedded systems determine vehicle design and shape the entire value chain. These standards define how the various vehicle systems interact, guide technical decisions, and ultimately determine which players are able to integrate into the ecosystem.

Sino-European partnerships play a central role in this dynamic. They enable the circulation of capabilities originating from mature industrial ecosystems, particularly in areas such as complex systems integration, validation processes, and quality standards. These capabilities are progressively absorbed and embedded into systems whose organization is controlled by Chinese players. Over time, the accumulation of knowledge derived from these partnerships allows for the reconstruction of fully integrated industrial capabilities, without direct transfers of sensitive technologies.

Industrial investments in Europe extend this trajectory by anchoring Chinese players within local territories, facilitating access to public support mechanisms, and strengthening their integration into regional ecosystems. The diversity of national strategies across the European Union enables differentiated modes of entry, whose cumulative effects gradually reshape the structure of value chains.

These developments are shifting the core of industrial value toward the ability to orchestrate system-level operations and steer innovation trajectories. In this context, industrial partnerships go far beyond operational cooperation.

They contribute to redistributing learning capabilities, reconfiguring value chains, and shaping the conditions under which industrial power is exercised. As such, the way these partnerships are designed and governed becomes a critical issue for preserving long-term control over industrial architectures and the ability to capture associated value.

From market rivalry to a reconfiguration of power

The arrival of Chinese carmakers in the European market can no longer be read simply as a matter of price competition or the opportunistic use of excess industrial capacity. These factors are visible, certainly, but they only hint at a deeper shift. The real story is the progressive transformation of competition into a structural power relationship, where the objective, in addition to gaining market share, is to reshape Europe’s technological and industrial sovereignty.

This shift is already visible in several recent moves: Geely’s takeover of Volvo, strategic partnerships between Chinese groups and European manufacturers, and the establishment of electric-vehicle plants in Central Europe.

China’s strategy rests on a quiet manoeuvre of encirclement. It blends targeted industrial investments, capital-based alliances, methodical normative influence and progressive integration into European ecosystems. Each initiative, taken individually, can appear rational and mutually beneficial. Yet collectively they create a cumulative integration mechanism, one capable of shifting technological and decision-making centres of gravity without ever resorting to open confrontation. It is a gradual progression that turns industrial cooperation into an instrument of power far beyond the confines of commercial logic.

Time itself has become a decisive strategic lever. While Europe often continues to think in terms of product cycles and short financial horizons, Chinese actors frame their decisions within long-term trajectories, backed by tight coordination between the state, industry and regulatory bodies¹.

Every investment, partnership or minority stake forms part of a global timeline, in which the step-by-step consolidation of technologies, standards and platforms shapes the future orientation of entire ecosystems. Long-term strategy thus becomes an asset in its own right, capable of turning marginal footholds into durable sources of power.

For Europe, the stakes go far beyond industrial competitiveness. They concern the preservation and projection of sovereignty: the ability to define its own technological architectures, steer innovation pathways, set standards and structure industrial ecosystems according to its strategic priorities². The traditional focus on prices and volumes obscures this systemic dimension. It no longer suffices to understand the risks, nor to anticipate the power dynamics shaping the twenty-first-century automotive industry.

What follows therefore seeks to decipher the mechanisms of integration, learning and normative influence that are reshaping Europe’s technological and industrial balance of power.

A strategy of integration rather than confrontation

1. The logic of progressive anchoring

Chinese carmakers drew a clear lesson from their early attempts at direct exports: lasting access to the European market could not be achieved through low prices alone, nor through a frontal assault on segments shaped by decades of accumulated industrial, technological and symbolic capital. Their strategy has therefore shifted towards gradual insertion at the very heart of existing ecosystems, replacing open confrontation with a logic of progressive integration.

The acquisition of Volvo by Geely, the rising stake in Lotus, and the deepening partnerships with Renault or Stellantis are good examples³ ⁴. They act as carefully selected footholds designed to confer immediate technological legitimacy, enhance brand credibility and secure privileged access to Europe’s industrial networks. This approach neutralises a significant share of political and social resistance: the investment presents itself as a strategic partnership, or even an industrial rescue, rather than a competitive incursion.

These moves provide direct access to scarce expertise, capabilities that are difficult to build internally: vehicle development know-how, management of complex industrial platforms, system validation processes, quality culture and multi-layer integration skills. The alliance is never viewed as an end in itself but serves as a mechanism for accelerated learning and strategic repositioning, enabling Chinese actors to close capability gaps step by step while maintaining the formal appearance of balanced ownership structures.

Geely’s 2010 acquisition of Volvo is a case in point, granting immediate access to world-class engineering capacity and global brand credibility. Similarly, the creation of Horse Powertrain with Renault, or Stellantis’s stake in Leapmotor, opens reciprocal channels to technologies and markets. Taken together, these ventures illustrate a coherent strategy of industrial anchoring rather than opportunistic deal-making.

This anchoring creates a subtle but decisive shift. It transforms a reversible commercial relationship into a durable industrial one embedded in organisations, territories and production routines. Integration becomes a long-term stabilising force, far more effective than a market-share grab exposed to commercial cycles and shifting political winds.

2. Long-term strategy as a comparative advantage

This strategy rests on a conception of time fundamentally different from the one that still dominates European industrial governance. Where Western groups operate according to product cycles, constrained financial horizons and quarterly trade offs, Chinese actors embed their decisions within long term industrial trajectories, supported by unusually stable public policies and strong coordination between state, industry and standards bodies⁵.

Every plant, partnership or minority stake is conceived as part of a holistic system. The strategic effects become fully visible only in the medium term, once the critical building blocks of technologies, standards, architectures, networks and data have been sufficiently consolidated to make the opposing ecosystem’s dependence costly, if not structural. Strategic patience becomes an asset in its own right, turning initially marginal positions into long-lasting levers of influence.

In this perspective, competition takes the form of shaping future industrial pathways rather than gaining immediate market share. Long-term strategy allows China to replace a logic of conquest with one of progressive absorption, where learning, integration and standard-setting precede and ultimately enable commercial dominance.

This temporal asymmetry is one of China’s most powerful comparative advantages in today’s reconfiguration of global value chains. It provides Chinese manufacturers with the rare ability to invest in segments that may be unprofitable in the short run but are decisive for structuring tomorrow’s industrial balance of power⁶. For Europe, the challenge is to preserve current positions and avoid losing control of its future trajectories in this battle over the long term.

The invisible battle of standards and architectures

1. From markets to standards: shifting the battlefield

The most consequential strategic rupture no longer lies in production capacity, nor even in short-term technological advantage, but in control over standards. True to the industrial adage that “first-tier firms set standards”, China has launched a methodical offensive on norms, centred on its China Standards 2035 strategy and a systematic presence in international standard-setting bodies⁷ ⁸ ⁹. The objective goes beyond supporting an industrial move upmarket; it seeks to convert temporary technological advantages into structural positions of control.

In the automotive sector, three domains now concentrate most of this contest: vehicle to environment connectivity, battery and charging standards, and regulatory frameworks for autonomous vehicle certification. Each is a critical node in the future value chain. By gradually imposing its technical choices as international references, China is able to export its technologies, while also rewriting the conditions of market access, transforming its patents into regulatory tollgates and compelling competitors to integrate components it already dominates.

The mechanism is strategically effective precisely because it avoids explicit protectionism or open trade conflict. Influence emerges through quiet, progressive harmonisation. Once adopted internationally, a standard often becomes, almost automatically, a regulatory requirement within Europe, even when Europe did not shape its design nor control the negotiations that produced it¹⁰. The case of 5G offers a telling precedent: normative influence precedes and ultimately defines industrial dominance. The same logic now plays out in batteries. Choices around formats such as cell-to-pack, chemistries like LFP versus NMC, or charging protocols directly shape vehicle and infrastructure architecture. Once widely disseminated, these standards guide the entire ecosystem, from component suppliers to charging-network operators. Their gradual adoption generates lock-in effects that far exceed the significance of any initial technical advantage.

In this context, the battle over standards becomes an instrument of power in its own right. It shifts competition away from costs and volumes towards the far more strategic terrain of defining the rules of the game. Of course, whoever writes the standards wins markets, but more importantly, they shape industrial hierarchies for the long term.

2. Locking in critical architectures

Beyond formal standards, the battleground is moving to an even deeper layer: technological architectures. The electric, connected vehicle depends on software platforms, embedded operating systems, communication protocols and data-processing chains that structure the entire value system¹¹ ¹². These architectures function as the invisible infrastructure of the twenty-first-century automotive industry. By controlling these foundational layers, Chinese actors are able to organise the ecosystem around their own technical choices, set the direction of innovation and create systemic dependencies that extend far beyond the vehicle itself.

For Europe, the risk is one of progressive lock-in: once dominant platforms are established, innovation becomes constrained within frameworks it no longer defines.

This dependency is all the more insidious because it produces no immediate shock. There are no factory closures, no sudden job losses. Instead, the shift unfolds slowly within intermediate layers – software, data, interfaces – where value creation, bargaining power and ecosystem governance increasingly reside.

Over time, the issue surpasses industrial competitiveness.

It touches Europe’s ability to remain a normative power, capable of defining its own technological architectures rather than operating within systems designed elsewhere.

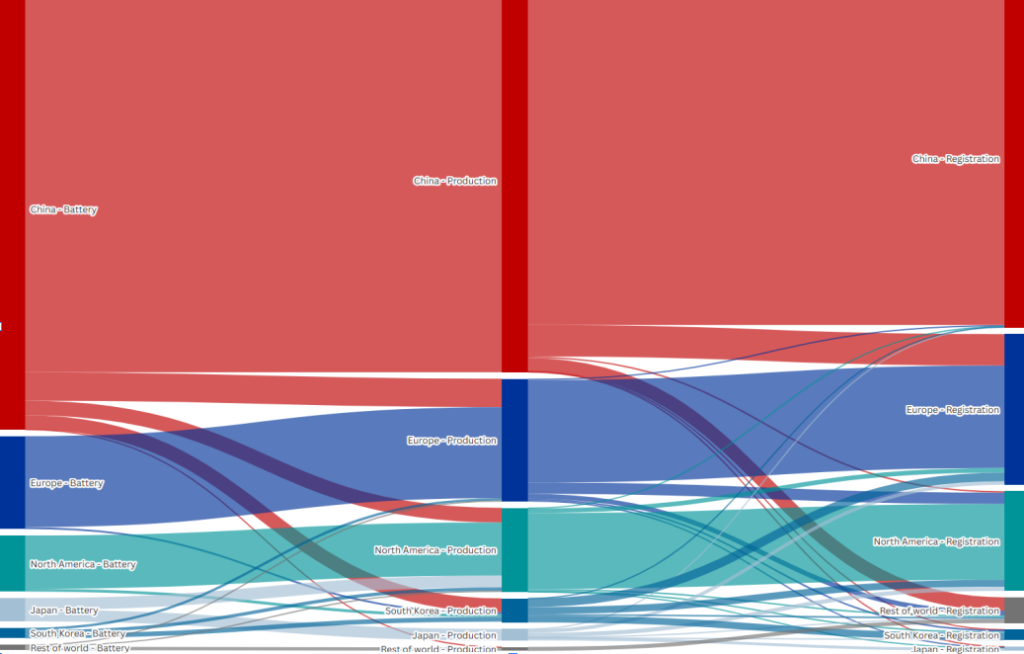

Figure 1: Cross-dependence: Global trade flows of lithium-ion batteries and electric vehicles (in GWh), 2023¹³

Source: IEA analysis based on Benchmark Mineral Intelligence and EV Volumes data

Note: The flows represent batteries produced and sold as part of electric vehicles. The battery itself is crucial: its characteristics (format/cell-to-pack design, chemistry, voltage, thermal management) shape the vehicle’s architecture and influence key industrialisation choices.

Industrial alliances and asymmetric learning

1. Partnerships as instruments of restructuring

Sino-European alliances are often presented as pragmatic responses to short-term constraints: sharing investment burdens, gaining reciprocal access to markets, or mitigating technological risk. But this transactional reading vastly understates their systemic implications. Indeed, these partnerships have become central instruments for reshaping technological power relations¹⁴.

In technology-focused collaborations between European and Chinese manufacturers, asymmetry rarely lies in governance structures or ownership balances; it lies in the nature and direction of knowledge and innovation flows. European partners typically bring capabilities deeply rooted in mature innovation ecosystems – mastery of complex systems integration, rigorous validation and testing processes, high-end quality standards – all of which are difficult to replicate outside these environments. Chinese actors, by contrast, tend to retain control over their software architectures and technological platforms, while absorbing, adapting and reconfiguring these European capabilities to accelerate their own innovation trajectory and narrow existing capability gaps¹⁵ ¹⁶.

In the short term, this equilibrium can appear functional, even mutually beneficial. But over time it generates a form of strategic gravitation. Chinese firms progressively internalise the organisational, methodological and industrial building blocks that underpin long-term performance, while Europe’s comparative advantage erodes, without any visible loss of legal or capital control. Instead of emerging through hostile takeovers or sudden strategic shocks, dependence results from a gradual shift in technological and decision-making gravity.

In this structure, the alliance serves as a mechanism for accelerated learning, deliberately designed to reduce structural capability gaps while maintaining the formal appearance of contractual balance. What is at stake is less the ownership of assets and more the mastery of dynamic capabilities, those that allow an actor to steer industrial trajectories over time.

2. The risk embedded in intermediate layers

While the danger of explicit transfer of breakthrough technologies is now reasonably well monitored through investment-screening mechanisms, the main danger now lies in the circulation of intermediate layers, validation procedures, integration methods, simulation tools, test architectures and datasets, whose aggregation enables, over time, the reconstruction of complete industrial capabilities.

This dynamic falls largely outside the traditional categories of strategic protection. It does not concern industrial secrets in the strict sense, nor dual-use technologies. Rather, it touches on transversal competencies that are often underestimated when viewed individually, yet prove decisive when combined. It is precisely within these intermediate layers that the ability to design, industrialise and validate complex systems now resides.

The recent history of semiconductors offers a revealing parallel¹⁷. China’s rise in this domain emerged from the gradual absorption of mature building blocks, reorganised into coherent industrial trajectories; it did not emerge from direct access to cutting-edge technologies. As a result, far from immediate and dramatic, losses manifest as a silent erosion of Europe’s ability to integrate systems, steer technological development and govern platforms.

What was previously considered a threat to final technologies alone now concerns Europe’s ability to orchestrate entire industrial ecosystems, a capability that could migrate beyond its reach.

Industrial implantation and territorial restructuring

1. Producing in Europe to secure market access

The rise of tariff barriers, carbon-adjustment mechanisms and local-content requirements has triggered a decisive strategic shift: the move from an export-driven model to a strategy of territorial implantation¹⁸. Industrial projects in Central Europe, Turkey and several EU member states are good indicators of this structural change: they show how Europe is being transformed into an integrated production base, organically woven into Chinese value chains.

Here, foreign investment morphs from a simple tool for industrial optimisation into an instrument of strategic stabilisation. By localising an increasing share of their production within Europe, Chinese manufacturers gradually neutralise traditional trade-defence tools, tap into public subsidies linked to the energy transition and embed themselves within local ecosystems of suppliers, engineering skills and industrial know-how. This shift profoundly changes the nature of the relationship: the boundary between “European industry” and “non-European industry” becomes increasingly porous, if not conceptually ambiguous.

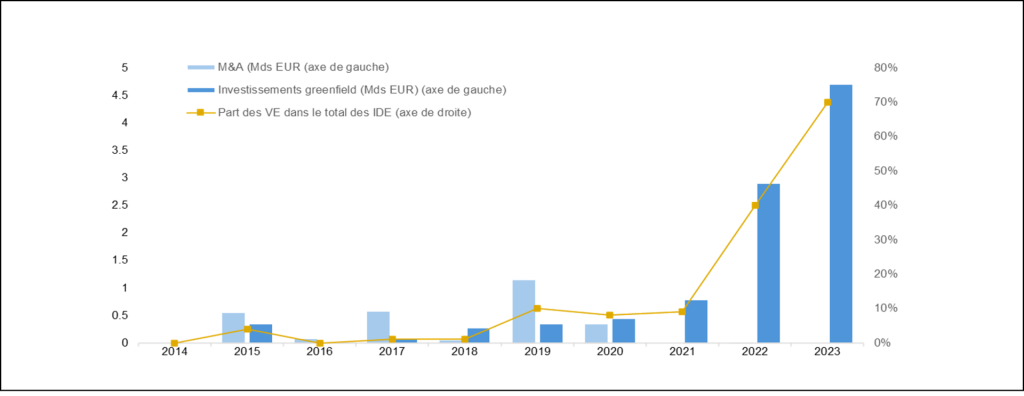

Figure 2: Chinese investment linked to electric vehicles in Europe is dominated by greenfield construction¹⁹

Source: Groupe Rhodium, 2024

This blurring carries significant political weight. Once factories are built, jobs created and regions financially committed, any strategic reversal involves high economic, social and political costs. Industrial implantation thus generates a territorial lock-in effect: it turns a reversible commercial relationship into a long-term industrial one, firmly anchored in national and regional economies. In time, trade flows are reshaped, but importantly, so is Europe’s own industrial geography, increasingly structured by actors who, though operating locally, remain embedded in external technological and strategic frameworks.

2. Exploiting European fragmentation

This territorial strategy thrives on Europe’s fragmentation. The absence of a unified industrial doctrine, the diversity of investment-screening regimes and the competition between member states create a political as well as economic optimisation space. Certain regions position themselves as privileged entry points, offering regulatory, tax or financial incentives to attract major projects, often without a consolidated assessment of their long-term strategic implications²⁰.

In addition to the usual competition for investment, this creates a lasting differentiation of industrial positions within the Union, producing asymmetric dependencies between territories, sectors and value chains. Leveraging these disparities, Chinese firms effectively fragment the European industrial space, reducing the EU’s ability to articulate common positions on negotiation, protection or reciprocity²¹.

The comparison with European carmakers entering China in the 1990s is often invoked, but it is deeply misleading.

At that time, Western groups entered an administered market from a position of technological, normative and organisational superiority. Today, Europe welcomes foreign players who already dominate several critical segments, bringing with them stabilised standards, platforms and industrial trajectories. The asymmetry is now technological, normative and systemic, as opposed to commercial or legal.

In this context, European fragmentation becomes a major strategic vulnerability. Individual projects may appear marginal, but taken together, they redraw the landscape: a growing share of Europe’s industrial base operates under architectures, standards and decision-making logics shaped, at least partially, from outside the Union. What matters is less the immediate scale of these investments than their cumulative impact: the progressive creation of a territorial web capable of influencing Europe’s industrial, social and political orientations for decades to come.

Towards an offensive industrial sovereignty

1. Ring-fencing strategic assets

The first condition for an offensive industrial sovereignty is the ring-fencing of strategic assets. Critical skills, technological architectures, industrial platforms, engineering capabilities and intangible capital have become instruments of power in their own right, just as essential as physical infrastructure or logistics chains.

Their protection requires a systemic approach to sovereignty, bringing together industrial policy, competition policy and innovation strategy. This need for coordinated European action was highlighted in the Draghi report on Europe’s industrial sovereignty, which emphasises the consolidation of strategic nodes and the alignment of investment priorities to safeguard the Union’s industrial autonomy²².

In a context of rapidly shifting value chains, mastering these structuring segments becomes decisive. The task is not simply to preserve existing positions, but to identify and

strengthen the strategic nodes that will shape tomorrow’s industrial ecosystems. Achieving this requires Europe to orient investment flows, coordinate technological priorities and foster European platforms capable of setting their own architectures.

Recent initiatives around batteries, shared industrial platforms or data infrastructures are important. While they may represent, in part, catch-up efforts, they also represent an attempt to rebuild a European capacity to organise industrial ecosystems.

2. Governing industrial partnerships

Another decisive dimension of sovereignty lies in the architecture of industrial partnerships. Alliances with Chinese players can no longer be approached merely as tools for market access or cost-sharing. They are embedded in long-term trajectories where technological, industrial and normative power dynamics take shape, often irreversibly. Their strategic reach extends far beyond equity stakes: it encompasses the control of technological architectures, critical interfaces and innovation pathways that structure the entire value chain.

The central question revolves around the trajectory of power implicit in each partnership: Who controls the critical interfaces? Who defines standards and platforms? Who steers investment priorities and innovation roadmaps? It is at this level – often silently – that strategic dependence is forged. Governance must therefore be grounded in a dynamic reading of future asymmetries, based on the anticipation of technological and industrial imbalances, not on formal legal balances. This requires political oversight of strategically significant partnerships, involving governments, industry and regulators, to preserve Europe’s decision-making autonomy over time.

European initiatives such as the European Battery Alliance or the European Chips Act follow a complementary, but distinct logic. Their purpose is to structure industrial capacity at the continental scale. The former aims to establish a competitive and integrated sector, one that is resilient to external dependencies; the latter seeks to strengthen the EU’s technological sovereignty in a key sector for digital industries and critical systems²³. By contrast, partnership governance operates at the level of private actors, within the concrete configuration of collaborations, where the balance of technological power and learning trajectories are shaped. The challenge is to align the macro and the micro so that local industrial dynamics do not undermine Europe’s broader strategic objectives²⁴.

These examples show that the governance of industrial alliances demands a strategic vision, coordination instruments and precise oversight mechanisms, ensuring that Europe’s integration into global value chains reinforces its capacity to influence and decide on key technologies and standards.

3. Reclaiming normative influence

The final strategic frontier is perhaps the most decisive: normative influence. As earlier sections have shown, the battle over standards is now a central arena of industrial competition, and for Europe, it has become an explicit strategic issue. In the automotive sector, as in network-based industries, standards now determine competitiveness.

Europe cannot afford to remain a passive adaptor. It must re-establish itself as a prescriber capable of embedding its technological choices within international frameworks, turning them into reference points for global markets. This requires a strategic mobilisation of public and private actors, sustained investment in standardisation work and close coordination between economic diplomacy and industrial policy. Initiatives such as the Digital Markets Act or the EU’s work on battery and electric-vehicle standardisation illustrate how regulatory frameworks can act as levers of influence and sovereignty.

Standards become tools of projection, shaping market structures as effectively as technology or capital. In this sense, more than just defensive instruments, offensive industrial sovereignty aims to rebuild Europe’s ability to organise ecosystems, mastering structuring assets, governing strategic alliances and reclaiming normative power. Only through such a systemic approach can Europe remain an industrial power able to define, rather than endure, the rules governing the automotive world of the twenty-first century.

From reaction to doctrine

The quiet reshaping of Europe’s automotive industry by Chinese players is neither a spectacular offensive nor a straightforward price war. It stems from a systemic strategy built on the progressive integration of ecosystems, the absorption of European know-how, and the control of standards and underlying technological architectures. What is at stake is not an obvious loss of market positions, but a shift in the centres of decision-making. As architectures, standards and integration chains slip beyond Europe’s control, the industry may appear outwardly intact while gradually losing the ability to shape its own future.

For Europe, the danger is a slow and silent marginalisation: the erosion of integration capabilities, growing dependence on external architectures and standards, and a weakening of normative influence. Traditional defensive tools – one-off subsidies, investment-screening procedures, trade barriers – must be embedded within a long-term vision that links industrial policy, alliance governance and the recovery of normative power.

Industrial sovereignty should defend existing assets, but it must also organise ecosystems, secure strategic nodes and shape future technological pathways. This demands coordinated European leadership, able to anticipate asymmetries, steer investment and deploy governance mechanisms that are both flexible and robust. Only a systemic approach can turn constraint into leverage, replacing defensive reflexes with a proactive strategy of industrial power.

Otherwise, Europe may retain its factories and its brands, yet lose something essential: the ability to define its own technological rules, influence standard-setting and steer its industrial ecosystems according to its strategic priorities. The battle for sovereignty is a long-term contest, fought in the gaps between standards, platforms and alliances, and it requires a clear, coherent doctrine commensurate with the challenges of the twenty-first century. Instead of merely taking part in industrial competition, the challenge is to define its rules. A power that manufactures without shaping the underlying architectures ultimately becomes dependent on those it did not design. Europe now stands at this point of inflection: either it regains the capacity to set the terms of the game, or it settles into a lasting posture of adaptation. In the world of systems, dependence is never declared: it is built. Quietly.

Frédéric Recordon – Partner, Accuracy

The silent encirclement – How China is redrawing Europe’s automotive sovereignty