America’s Historic Infrastructure Investment May Not Deliver Historic Results.

Historic capital mobilisation is colliding with bottlenecks in labour, power, materials, and permitting, reshaping timelines and strategies across the infrastructure sector.

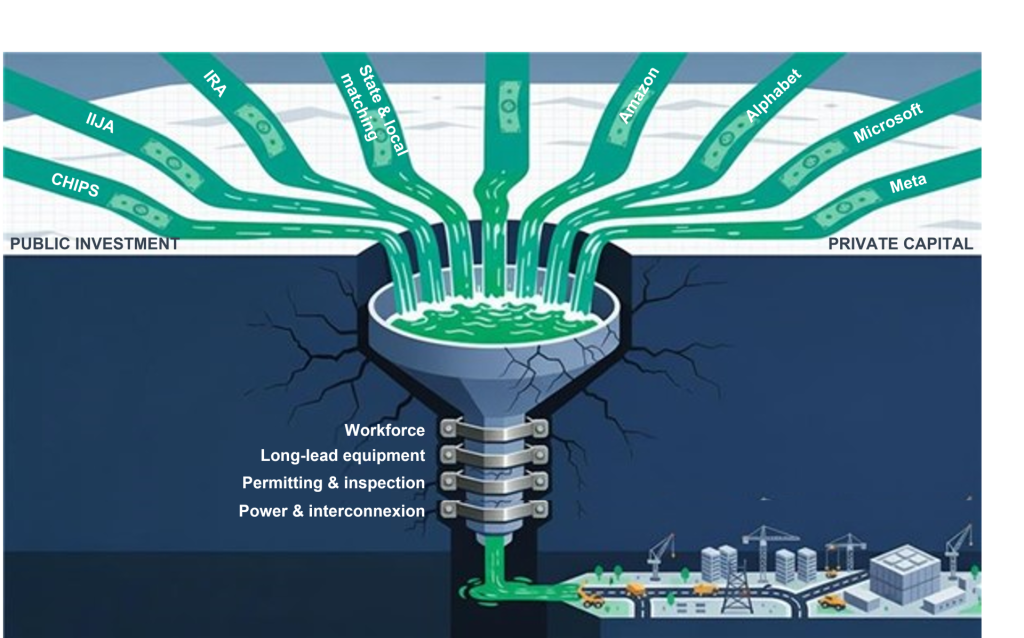

A NEW INDUSTRIAL AMBITION MEETS OLD CAPACITY LIMITS

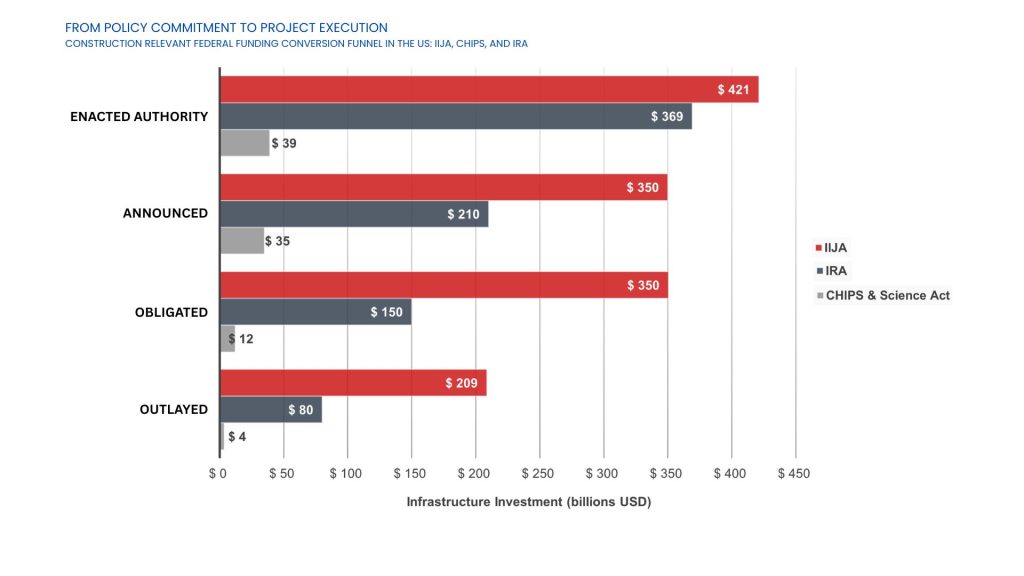

The United States is committing more capital to infrastructure and industrial build-out than at any time since the post-war era. Post-pandemic federal programmes span the $1.2 trillion Infrastructure Investment and Jobs Act (IIJA), clean-energy tax incentives under the Inflation Reduction Act (IRA) worth hundreds of billions, and $50 billion in CHIPS Act funding for semiconductor fabrication and R&D. Yet these historic public sector appropriations have been outshone by exceptional private- sector ambition, exemplified by hundreds of billions in capex for data centres and AI-adjacent infrastructure.

As headline grabbing as these announcements are, funding does not equal field execution.

Long before construction, projects must navigate obligations, design, procurement, permitting and interconnection. Once in the field, execution capacity becomes the binding constraint.

What distinguishes the current cycle is not only the scale of investment but the fact that public and private programmes are unfolding simultaneously and drawing on the same constrained pools of skilled labour, long-lead grid and industrial equipment, permitting and inspection resources, and, above all, power and interconnection.

THE DUAL BOOM IN THE NUMBERS: PUBLIC PROGRAMMES AND PRIVATE MEGAPROJECTS

The scale of what is underway is now clear. In recent earnings calls, the four largest hyperscalers – Amazon, Alphabet, Microsoft, and Meta – announced combined capex guidance of roughly $625 – 665bn for 2026, up approximately 60% year-over-year. Roughly three quarters of that (around $450 – 500bn) is directed specifically to AI infrastructure: GPUs, servers, networking equipment, and the data centres to house them. This single year spend rivals the GDP of medium-sized economies and exceeds any prior private-sector infrastructure buildout in modern history. Not all of that spend hits US construction. Hyperscaler capex breaks roughly into equipment (servers, GPUs, networking gear), land, site preparation and building construction (shell, power, cooling). Industry cost breakdowns, suggest that $120 – 150bn of 2026 capex will translate into physical data centre construction globally, with the US accounting for roughly

$80 – 100bn.

This aligns with project level intelligence. ConstructConnect reports that US data centre construction starts reached $77bn in 2025, up from roughly $15bn in 2023, with forecasts for 2026 in the $80 – 100bn range, consistent with hyperscaler guidance and the multiyear buildout timelines for megacampuses announced in Texas, Virginia, Ohio, Louisiana, and Illinois.

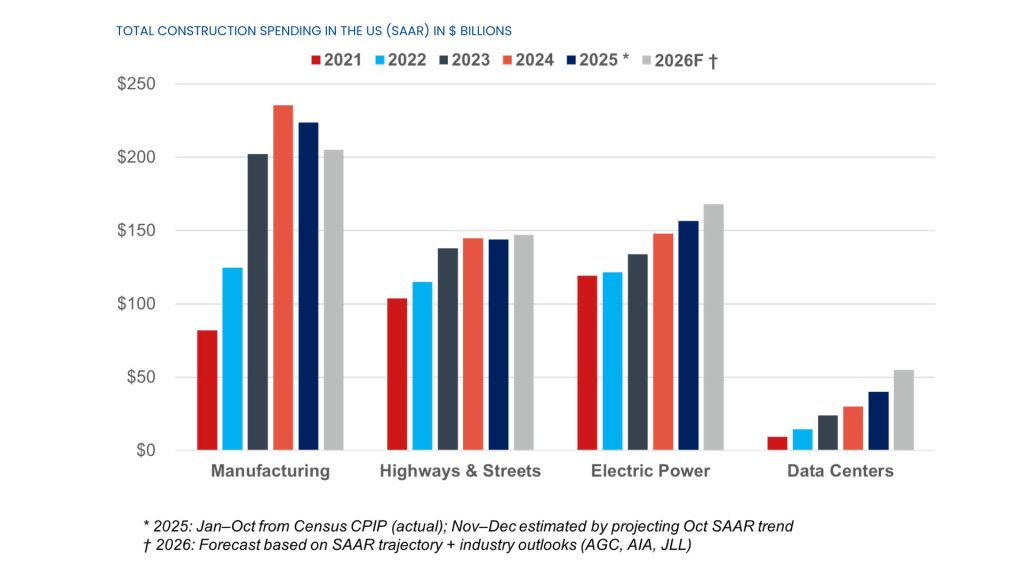

IIJA, IRA and CHIPS have driven highway, transit, grid, and manufacturing spending well above pre-pandemic levels. US Census data show manufacturing construction rising from roughly $76bn (seasonally adjusted annual rate) in 2020 to over $200bn annually for the last four years. Highway and street construction has also increased materially under IIJA, and ENR reports that major US owners’ construction in progress climbed 9.3% from 2023 to 2024, to nearly $596bn.

What sets this dual boom apart is the simultaneity and the nature of the demand. Traditional public infrastructure — highways, bridges, transit — now competes for labour, permitting bandwidth, and structural steel with private megaprojects that also requires transformers, switchgear, high voltage electricians, and, above all, electrons. Just as the electrician wiring a data centre cannot, at the same time, pull cable on a light rail extension, a 345kV transformer allocated to a semiconductor fab is not available for a utility’s grid modernisation scheme. A similar gating effect exists in the bureaucracies approving the energization of these projects.

FROM AUTHORISATION TO DIRT MOVING: THE SLOW CONVERSION FUNNEL

Even with unprecedented federal appropriations, the path from funding to execution remains long. IIJA and CHIPS programmes move through sequenced authorisation, obligation and award processes, while IRA support is primarily incentive-driven and realized ex post. Across all three, progress toward construction requires navigating finite labour bandwidth, procurement queues, environmental reviews, and grid interconnection procedures. As of April 2025, the Department of Transportation had obligated roughly 59% of IIJA funding and outlaid just over half, illustrating persistent lags even in well-established programmes.

These delays are not merely administrative: they reflect binding constraints in engineering resources, equipment availability, right-of-way and permitting throughput, and utility relocation. The funnel is further compressed by the scale of concurrent private investment. Hyperscalers now rival federal programmes in demand for hardware, materials, and specialised trades, intensifying competition for the same scarce inputs. As upstream bottlenecks bind, even fully funded portfolios experience schedule deterioration, underscoring that the dominant risk in this cycle lies not in access to capital but in system throughput.

Four Crucial Bottlenecks

Labour

Shortages are most acute in skilled electricians, commissioning technicians and specialised mechanical trades. Bureau of Labor Statistic data shows 292,000 construction job openings in November 2025, while the Associated General Contractors of America (AGC) reports 92% of contractors struggling to fill craft roles and 45% experiencing project delays tied to staffing gaps. Portfolio planning must assume overlapping megaprojects drawing from the same labour market cannot be staffed concurrently.

Long lead equipment

Large power transformers now carry average lead times of about 120 weeks, ranging up to 210 weeks for the biggest units. Distribution transformers have peaked at up to two years, and gas turbines show similar horizons. These constraints increasingly dictate project sequencing. In practice, procurement becomes the schedule driver, sometimes requiring equipment orders to precede detailed design.

Permitting, approvals, and inspection

The Council on Environmental Quality (CEQ) reports a median federal EIS timeline of about 2.2 years in 2024. Local approvals, inspections and interconnection reviews, however, continue to delay shovel ready projects. Throughput and staffing levels, more than statutory deadlines, determine progress. Recent federal workforce reductions have further limited review functions. Significant staffing cuts at EPA, DOT, and the Army Corps of Engineers in early 2025 reduced administrative bandwidth just as IIJA and IRA portfolios required peak processing. The resulting backlog affects compliance, permitting, approvals and inspections, already strained by rising private-sector demand.

Power and grid interconnection

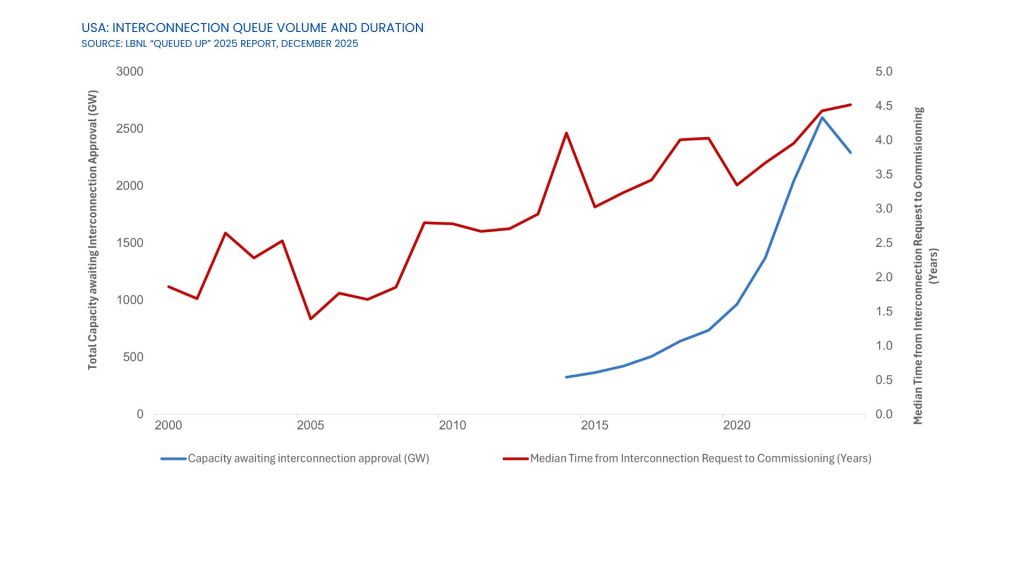

Interconnection queues held roughly 2,300 GW of capacity at the end of 2024, with median timelines from queue entry to operation reaching five years. Data centres, which consumed about 4% of US electricity in 2023 and may reach 9% by 2030, are intensifying demand for grid upgrades. FERC Order 2023 introduces important procedural reforms, but near-term delivery remains constrained by equipment availability and review capacity.

EXECUTIVE PLAYBOOK: HOW TO WIN WHEN CAPACITY BECOMES THE SCARCE RESOURCE

Plan for scarcity overturning past assumptions

Executives should reassess portfolios based on realistic expectations for labour availability, equipment lead times, and interconnection timelines, and model downside scenarios accordingly. Tail risks – multiple concurrent bottlenecks compounding into cascading delays – must be weighted appropriately. Past performance is no longer predictive in a capacity-constrained cycle. Interconnection queue positions and utility postings should be treated as firm constraints, not aspirational milestones.

Lock the critical path early

Securing the critical path therefore means locking in power commitments, transformer and switchgear orders, and key electrical and commissioning teams as early as possible.

When long-lead items dominate timelines, they effectively set the pace for the entire project.

Contract for volatility

Contracts should allocate material and equipment escalation risk appropriately. Clauses tied to interconnection timelines and equipment delivery dates support more predictable execution. AGC survey data indicate that delays from equipment and approvals are already pervasive.

Build repeatable delivery

Standardized substation designs, modularized MEP components, and consistent commissioning processes reduce reliance on scarce specialist trades. FERC’s 2023 readiness requirements favour well prepared, repetitive design packages.

WHAT POLICYMAKERS CAN DO TO INCREASE SYSTEM THROUGHPUT

Match administrative capacity to capital deployment

Federal EIS timelines have improved to a median of 2.2 years, but local permitting, inspection, and interconnection reviews remain bottlenecks. FERC Order 2023 reformed interconnection queue procedures to reduce speculative projects and accelerate study timelines, yet implementation requires corresponding investments in reviewer headcount, digital workflows, and enforceable service-level agreements. Procedural reforms fail without the resources to execute them.

Align workforce and procurement policy to supply realities

Apprenticeships and credential portability in high-voltage electrical and commissioning trades address long-term skill gaps but do not solve near-term shortages. Similarly, Buy America Build America (BABA) domestic-content requirements support long-term manufacturing resilience but collide with current equipment supply constraints. When equipment lead times exceed two years and domestic production cannot meet demand, rigid enforcement delays projects that are otherwise ready to build. Pragmatic phasing of domestic-content rules and clearer guidance on IRA incentives can reduce risk premiums and accelerate the conversion of obligations into actual outlays.

INTERNATIONAL PARTICIPATION: WHERE GLOBAL FIRMS CAN REALISTICALLY WIN

Success in the US requires local execution capacity and domestic content compliance. Grid equipment manufacturing, specialised trades, modular fabrication, and structured financing partnerships remain viable pathways. BABA rules and CHIPS Act guardrails shape procurement and supply-chain strategies, favouring firms that combine capital with local delivery capacity through joint ventures or acquisitions. Global conditions reinforce these openings. Similar constraints are emerging across Europe, the Gulf, and APAC, creating a broadly shared environment of scarcity. For international firms, this convergence means that entering the US market is less about escaping bottlenecks at home and more about bringing scalable delivery models that can operate under them.

CONCLUSION: CAPACITY IS THE NEW SCARCITY

The scale of America’s dual infrastructure boom is unprecedented. Yet the binding constraint has shifted from capital availability to system throughput. Federal obligations now outpace outlays not because appropriations have stalled, but because engineering bandwidth, long-lead procurement, and skilled labour pools cannot absorb the surge. In this environment, early certainty around power supply, equipment and expertise shapes project outcomes more than financing terms or legislative authorization. Organizations that recognize execution capacity as the scarce input – and adjust procurement, staffing, and schedule assumptions accordingly – will outperform those still relying on historical precedent. Past eras of capital scarcity rewarded financial discipline. This era of capacity shortages rewards operational foresight.