Several years ago, Mervyn King, a former Governor of the Bank of England, introduced the term ‘radical uncertainty’. Shouldn’t we acknowledge that in this rapidly changing world there is an abundance of things we do not know? For example, what new products and services will appear tomorrow, with what technologies and in what political and environmental context? According to Mr King, ‘Radical uncertainty means that many of the markets in which price might move to produce an equilibrium simply cannot and do not exist. The market economy cannot, therefore, coordinate spending plans’. As a consequence, it becomes impossible to assign probabilities to future events. This brings us to a distinction made by Frank H. Knight, an American economist active in the first half of the 20th century. He considers that risks can be quantified by attributing probabilities taken from previous experience or from statistical analysis, whilst uncertainty is unmeasurable and is synonymous with ‘unknowable unknowns’. So, what can be done when modern macroeconomics finds itself at a loss?

Three conclusions can initially be drawn. First, risk aversion, since it cannot be measured, penalises initiative-taking – growth can’t help but be negatively affected. Second, economic agents will seek to favour robust strategies, even if they are not particularly sophisticated, with the aim of protecting against unforeseen events or sudden changes. Of course, it is not the underlying data that determine asset prices, but rather the beliefs of the market regarding those data. These beliefs can in turn be challenged, if not more often then more radically than the data themselves. This leads to attitudes favouring caution, inaction, even pessimism, as the expected timeframe for generating returns on investment cannot be predicted more accurately than through rough estimates. Alongside any implications that this has for the pace of growth, we must remain attentive to the possibility of volatility and even significant corrections in asset markets. Finally, the perception that the very foundations of economic stability are being challenged leads us to adopt precautionary behaviours. Priority will be given to savings, bearing in mind that assets considered most likely to conserve their value will be favoured. But which ones? Those that appear least likely to lose their value, of course, but what trade-off will there be between government securities and liquidity?

This view of the economic environment, or to put it more accurately, the need to change the way we view it as a result of the changes underway, is bound to challenge insurance professionals. Isn’t the sector at somewhat of a crossroads?

- Traditional methods of risk assessment are having to evolve due to changes in the frequency of claims (for example, an increase in the number of climate-related disasters). Is it still possible to simply extrapolate from experience or from historical data?

- The costs of certain repairs are rising; will insurers be able to shoulder the burden?

- At a certain point in time, will we have to resign ourselves to the fact that an increasing number of risks cannot be effectively managed?

- With regard to assets held on company balance sheets, will allocation and asset management principles need to be revised?

We can see it: the raison d’être of the insurer is perhaps being called into question. Traditionally, insurance was a force for maintaining (or returning to) the original state of something; tomorrow, it could be a force for accompanying a changing environment. To prevent ‘uninsurability’ becoming the ultimate and default solution in some cases, familiar pathways should be further developed, while other, newer ones should be explored. These include systematic prevention, broader insurance pooling, promotion of anti-fragility (encouraging the innovation needed for inevitable adaptation) and further diversification of investments.

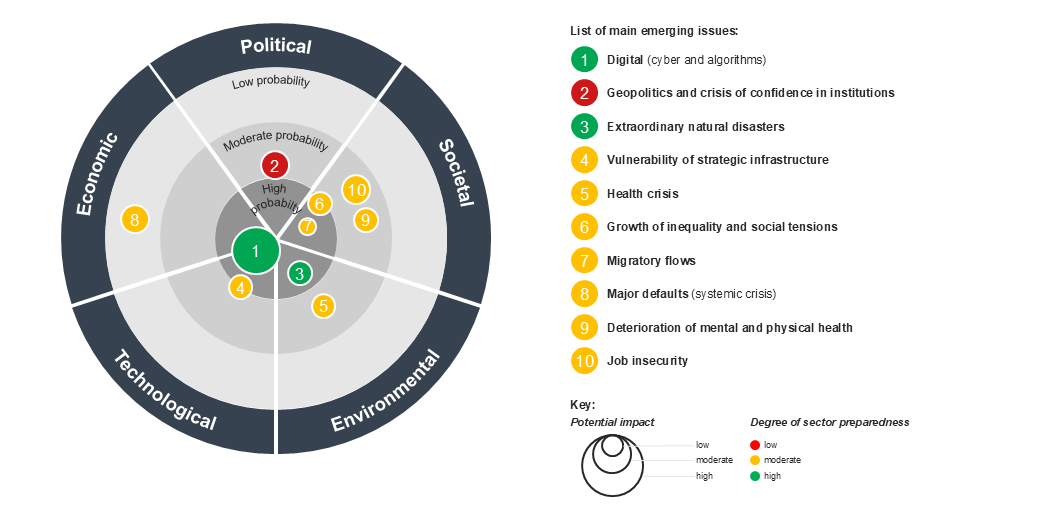

Where should insurers focus their attention? A study by CNP, published at the start of the year, identifies key risk areas based on three criteria: (i) the probability of certain events occurring within the next five to ten years; (ii) the potential impact of such events; and (iii) the extent to which the relevant sector is prepared. The framework used encompasses five sectors (economic, political, societal, environmental and technological) and three probability levels (low, moderate and high). However, the approach does not distinguish between risks and uncertainties.

The insurance sector: an overwiew of emerging issues

Source: CNP Assurances

The main issues are those for which the impact is high and preparedness low. According to CNP, none of them appears to fit this description. For example, the impact of a digital crisis is high; fortunately, so is the sector’s level of preparedness. At the next level down (moderate impact), the sector appears less prepared for a political crisis. Generally speaking, though the study concludes that we are relatively well protected against economic and environmental shocks, increased attention should be given to societal issues, where a number of themes that require close scrutiny are emerging.

The balance between risks and uncertainties is changing. We must learn to adapt, but how? First, by better managing identified risks, and second, by confronting uncertainty with greater confidence – in organisations, in decision-making processes and more generally in our human relationships. Nearly 30 years ago, Alain Peyrefitte, a former minister under General de Gaulle, published a book called The Confident Society. In it, he advanced the theory that confidence is the best ingredient for launching and fostering a thriving economy. Let insurers contribute to strengthening confidence by offering solutions to reduce uncertainty!

Hervé Goulletquer – Senior economic adviser

Accuracy Talks Straight #11 – Economic point of view